Evolution of Customer Experience Personalization

Segmentation of customers & tailoring customer engagement based on segment traits has been in practice for quite some time. However, with advances in technology, today it is possible to capture salient features of every interaction with the client, either in person or through automated channels. Predictive AI tools leverage this data to advise the ‘next best action’ and make the engagement with the customer a highly personalized interaction, rather than a persona-based interaction. With advanced capabilities of transaction platforms, personalization of client experience is also moving on to the next level in terms of customizing products to suit personal preferences, leveraging technology.

This is becoming a differentiator in the Wealth Management (WM) business too. WM has earlier seen high personalization for the Ultra High Networth Individuals (UHNI) & High Networth Individuals (HNI) segments, with a high level of Advisor touch. With the increasing focus on the lower end of the retail segment of the WM business, & individual touch not being an option because of the numbers involved, wealth managers face the challenge of offering a personalized experience to these customers. On the other hand, studies have indicated a high degree of willingness of wealth management customers to share personal data with their wealth managers – even slightly more than their willingness to share personal information with their physician or a health worker – for a more personalized service or user experience. Significantly, the willingness is high among all age segments too. This indicates a huge potential for a more fruitful customer engagement through deep personalization.

Personal / Direct Indexing

Evolution of technology has increased the ability to capture & mine data at the individual level. It has also increased computing power and predictive analytical capabilities to process this data real time. Enabled by all this, personalizing customer experience in terms of product offerings and servicing for all the WM customer segments is gaining traction. Personalization of WM products is taking the form of enabling a larger segment of investors to have customized portfolios, rather than invest in passive products like ETFs or model portfolios. Access to personalized products such as Single Managed Accounts (SMAs) have typically been restricted to UHNIs & HNIs in the Retail segment and Institutional investors. However, advances in terms of next generation product platforms have enabled offering Direct / Personalized Indexing variations of the SMAs, at scale. Unlike traditional SMAs which offer completely customizable portfolios, Direct / Personal Indexing accounts typically offer limited customization within an overarching standard model.

The US has been the main adopter of Direct / Personal Indexing as part of portfolio strategy, which has become very popular among affluent clients. Enablement of trading in fractional shares and increased availability of zero fee trading accounts in the US have been key reasons for the increasing popularity of the product among investors.

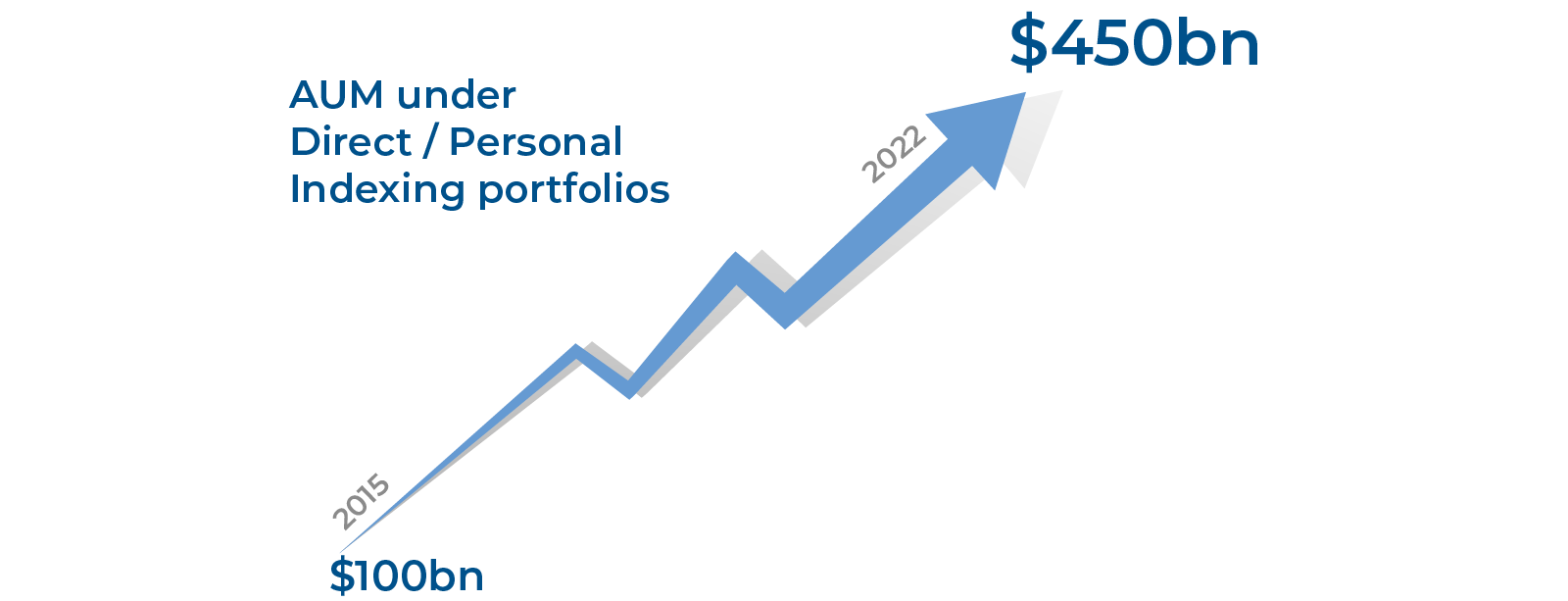

AUM under Direct / Personal Indexing portfolios is estimated to have grown more than four-fold from about US $ 100 billion in 2015 to about US $ 450 billion as at the end 2022 & is expected to be a key investment option for investors going ahead. The last few years have seen major players in the WM business like Morgan Stanley, Blackrock, J P Morgan Chase, Vanguard, Franklin Templeton, Charles Schwab, Fidelity etc. move into Direct / Personal Indexing space, reflecting the perception on future growth potential of this product.

AUM under Direct / Personal Indexing portfolios is estimated to have grown more than four-fold from about US $ 100 billion in 2015 to about US $ 450 billion as at the end 2022 & is expected to be a key investment option for investors going ahead. The last few years have seen major players in the WM business like Morgan Stanley, Blackrock, J P Morgan Chase, Vanguard, Franklin Templeton, Charles Schwab, Fidelity etc. move into Direct / Personal Indexing space, reflecting the perception on future growth potential of this product.

Why Personal / Direct Indexing?

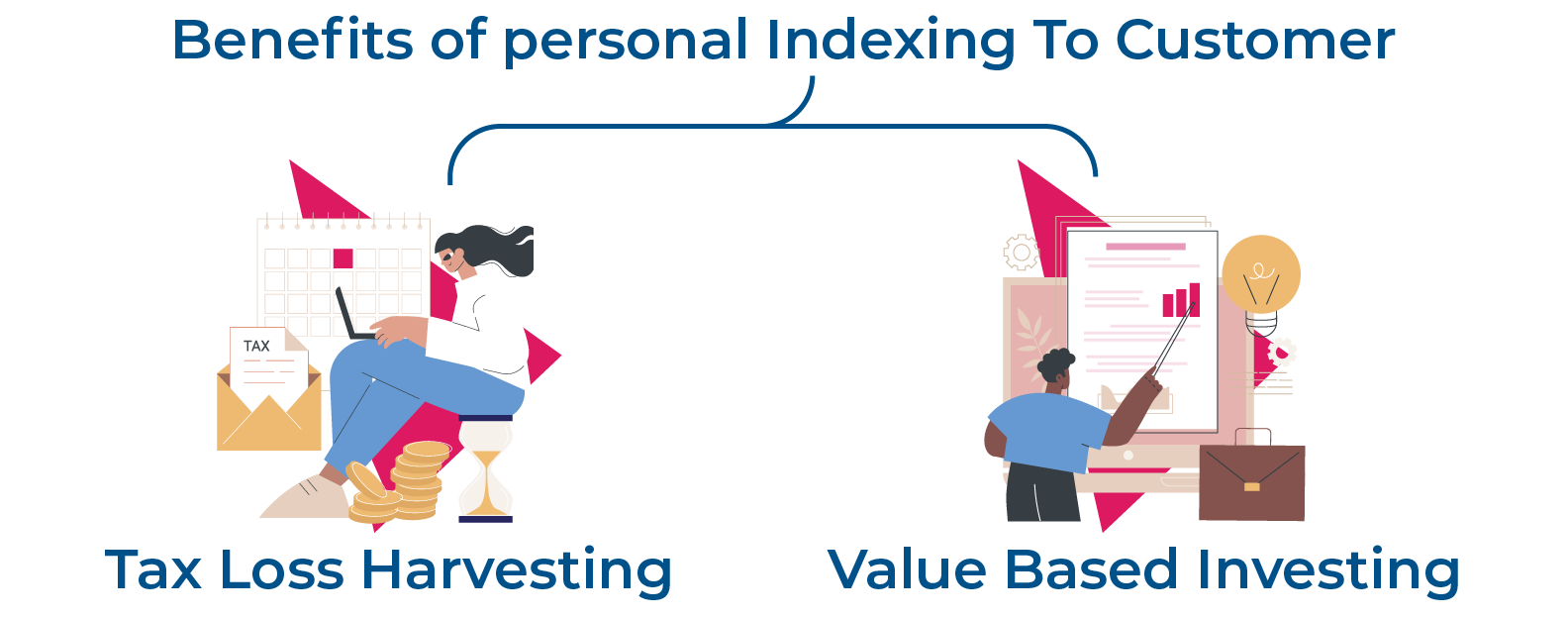

Benefits of a Personal Indexing portfolio to a customer are in terms of:

1)Tax Loss Harvesting

The investor is having a profit from other sources or investment with other advisors, and a book loss on one of the stocks in the portfolio. The investor can realize losses on the individual stock, replacing it with a similar stock not forming part of the index on which the portfolio is modelled. The loss can be offset against profit from other sources, reducing tax liability and improving net gains, without a large deviation from the portfolio strategy.

2) Value Based Investing

Investment in an alternate stock, similar in profile to the index stock, but preferred for other criteria like higher ESG compliance score, industry / country exposure, etc.

However, investors opting for Direct / Personal Indexing need to be actively involved in managing their investments, preferably with the help of a professional advisor. The strategy also makes sense only where there are other sources of income, the profits or losses accruing from which can be effectively managed. The WM firms benefit too, in terms of higher fees as compared to managing passive investments and also a stronger customer connect to grow their business.

Approach To Enabling Personal / Direct Indexing

A technology driven product, offering of Direct / Personal indexing product requires WM firms to acquire additional capabilities in terms of specialized technology platforms, besides trained manpower. This would include automated capabilities for advisory, trading, & portfolio management for this product, integration to client systems through digital channels for understanding client’s financial position & identifying tax loss harvesting opportunities, robo advisors capable of advising on tax loss harvesting opportunities & identifying alternate investments, Robotic Process Automation, etc.

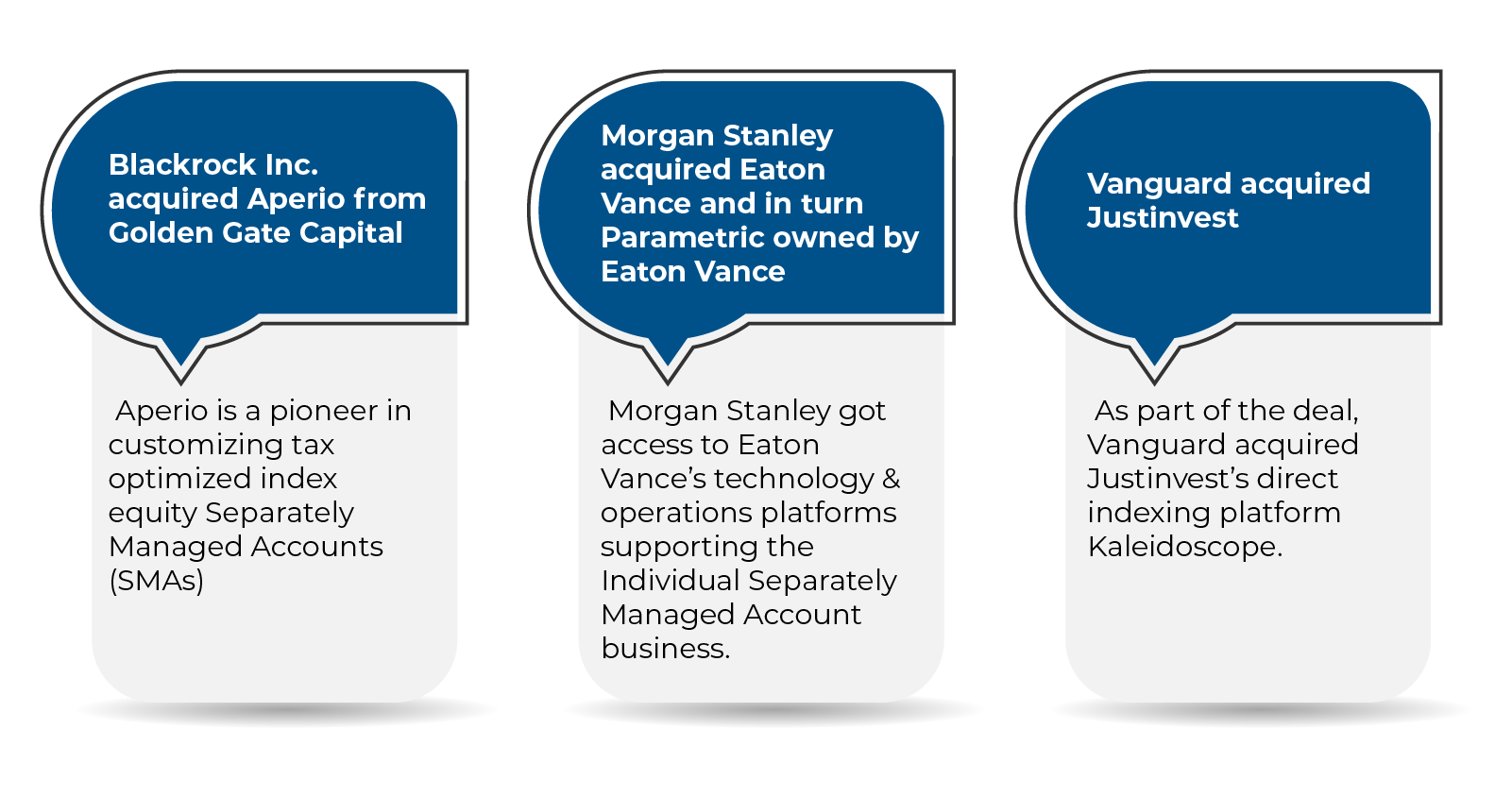

WM firms have the option of building these capabilities inhouse or acquiring them inorganically. The last few years have seen multiple M&A deals in the US geography with focus on adding Direct / Personal Indexing product capabilities to their existing portfolio of offerings.

Some examples of acquisition activity with focus on acquiring Personal / Direct Indexing capabilities are:

An example of in-house capability development for Personal / Direct Indexing has been Fidelity’s Solo FidFolio platform.

Continuing evolution of platforms with more & more computing capabilities and technologies like AI, is likely to see further innovations in product personalization in the WM business in future.

Co-authored by Eswaran Swaminathan, and Venkatesh Padmanabhachari

Maveric’s thought leadership series – E.D.G.E (Experiences Delivered by Global Experts) – handpicks the game-changing technology ideas and pressing functional questions financial institutions must solve today.

These features – reports, whitepapers, podcasts, flyers, blogs, and infographics – are for Banking leaders and Technology evangelists to apply profound trends, the latest opinions, and transformational analyses to boost the performance of their organizations.

About Maveric Systems

Established in 2000, Maveric Systems is a niche, domain-led, BankTech specialist, transforming retail, corporate, and wealth management digital ecosystems. Our 2600+ specialists use proven solutions and frameworks to address formidable CXO challenges across regulatory compliance, customer experience, wealth management and CloudDevSecOps.

Our services and competencies across data, digital, core banking and quality engineering helps global and regional banking leaders as well as Fintechs solve next-gen business challenges through emerging technology. Our global presence spans across 3 continents with regional delivery capabilities in Amsterdam, Bengaluru, Chennai, Dallas, Dubai, London, New Jersey, Pune, Riyadh, Singapore and Warsaw. Our inherent banking domain expertise, a customer-intimacy-led delivery model, and differentiated talent with layered competency – deep domain and tech leadership, supported by a culture of ownership, energy, and commitment to customer success, make us the technology partner of choice for our customers