The New Faces of Wealth: Startup Executives as High-Net-Worth Clients

Wealth doesn’t always arrive with predictability. Sometimes it enters overnight – unplanned, unstructured, and underserved.

That’s the reality of the startup economy. And it’s creating a new class of High-Net-Worth (HNW) individuals who challenge the traditional playbook of wealth management.

These are not your legacy HNW clients with generational capital and family offices. Startup executives (founders, early employees, and even product leaders) are amassing substantial wealth rapidly through liquidity events like IPOs, acquisitions, or secondary stock sales. But with that sudden wealth comes complexity, volatility, and a unique set of expectations.

For wealth management and financial services firms, this isn’t just a new segment, it’s a strategic opportunity. But only if you know how to serve them differently.

The Rise of the Startup HNW: Liquid, Young, and Under-Advised

Startup executives represent one of the fastest-growing and most under-leveraged HNW segments. According to Capgemini’s World Wealth Report 2024, nearly 25% of new HNW individuals under the age of 40 have earned their wealth through startup equity or tech entrepreneurship, more than double the figure from a decade ago.

The defining traits of this group?

- Sudden wealth creation: triggered by liquidity events, often compressing decades of financial accumulation into months

- Age and attitude: skewing younger (late 20s to early 40s) with strong digital affinity and DIY instincts

- Volatile wealth profile: concentrated in company equity, exposed to valuation swings, with limited early-stage liquidity

- Personal-professional entanglement: where startup performance and personal net worth are often the same thing

These traits create a persona that doesn’t fit neatly into traditional HNW advisory frameworks. And that’s precisely why wealth managers need to rewire how they acquire, engage, and serve them.

New Client, New Playbook: What Startup HNWs Really Want

This new generation of affluent clients doesn’t want brochures, relationship managers, or cookie-cutter portfolios. They want contextual insight, intelligent nudges, and hyper-personalized strategies that evolve as quickly as their liquidity does.

Here’s what sets their expectations apart:

- Speed and Clarity Post-Event IPOs or exits often flood startup executives with new cash and even more questions: Should I diversify? Where do I park unallocated capital? What about tax planning?

- Equity-centric Planning A large portion of their net worth is still tied to restricted stock, options, or phantom equity. They need advice that understands vesting schedules, 409A valuations, and cap table dilution.

- Flexible Goal Mapping Many startup HNWs don’t have fixed goals yet, but they want tools to explore scenarios: passive income by 40, early philanthropy, or even launching their next startup.

- Advisory That Feels Like Product Traditional relationship models fall short. They expect digital-first, mobile-native, and analytics-augmented experiences with real-time scenario modeling and proactive alerts.

Where AI Meets Affinity: The Strategic Advantage

To attract and retain this segment, firms must evolve from generalist advisory to persona-led precision. This is where AI-first frameworks come into play, not as a feature, but as a foundation.

According to a recent EY survey, wealth and asset management firms with over $2 billion in revenue identified generative AI as having the greatest potential impact in areas such as alpha generation, financial advice, client onboarding, marketing, and investment operations

At Maveric Systems, we help wealth platforms enable this shift through two core levers:

1) AI-Led Customer Acquisition and Conversion

Using AI to identify, qualify, and engage startup HNWs early, often before liquidity events, is a game changer.

- Pattern-based persona recognition: AI can detect trigger behaviors like stock plan inquiries, financial modeling app usage, or wealth-related keyword patterns in digital interactions.

- Predictive onboarding: Scoring startup execs based on likely liquidity timelines using company data, funding rounds, and option vesting analytics.

- Personalized landing experiences: Dynamic microsites and app modules tailored to founder journeys, equity event scenarios, or co-founder exit stages.

Result? Higher conversion rates, faster trust-building, and deeper engagement.

2) Advisor Enablement Through Persona-Based Workflows

Even the best advisors struggle with startup-specific complexity. AI can augment human expertise with guided, intelligent workflows tailored to this HNW persona.

- Real-time financial diagnostics: Automatically surfaces relevant insights, like cash burn rates, RSU expiration, or capital gains thresholds – linked to client equity events.

- Smart recommendations engine: Suggests tax strategies (QSBS, AMT), diversification paths, or philanthropic vehicles based on evolving liquidity and goals.

- Ongoing opportunity alerts: Detects when a client’s wealth footprint changes, e.g., upcoming lockup expiry, change in valuation and prompts the advisor with timely outreach playbooks.

JPMorgan Chase has integrated AI across its operations, leading to significant improvements in productivity. In asset and wealth management, tools like Smart Monitor and Connect Coach have increased advisory productivity by over threefold, enabling advisors to deliver more personalized and efficient services to clients.

This is not about replacing the advisor. It’s about amplifying their impact, especially in moments that matter.

And the industry is already moving in this direction:

“The UHNW client wants and deserves to get the best from multiple disciplines. The siloed business model is one of the past, and this positive change has been driven by client demand, client focus, and industry competition.” — Philipp Wehle, CEO, International Wealth Management, Credit Suisse

But for institutions to realize this impact at scale, internal transformation is critical. Traditional RM models, built around long cycles, manual prep, and static segmentation, must be recalibrated to prioritize proactive engagement, scenario planning, and AI-assisted decisioning. Business incentives need to shift from transactional KPIs to lifetime value creation. And compliance teams must be equipped to oversee AI-driven advice flows, ensuring explainability, suitability, and governance are embedded by design.

The Window of Trust Is Narrow and Now

There’s a short window when startup HNW clients go from pre-liquid to post-liquid, and it’s during this transition that trust is either built or lost.

Traditional models take too long to engage. By the time the first advisor meeting is set up, the client may have already moved capital elsewhere or made suboptimal decisions in haste.

To win this segment, firms need to anticipate moments, not just respond to them. That’s where AI-first design, backed by persona understanding and domain precision, becomes your moat.

This evolution also demands a rethinking of core technology infrastructure. Legacy CRMs and onboarding tools, often designed for static workflows, need modernization to support real-time context switching, persona-based journeys, and embedded intelligence. Whether it’s integrating AI signals into advisor desktops, or linking wealth trigger events to automated onboarding paths, speed and intelligence must flow across systems and not stay siloed in innovation labs.

Maveric’s Approach: Intelligence That Serves Insight

At Maveric, we’ve worked across banking and wealth ecosystems to modernize core platforms, digitize experiences, and embed AI across the customer journey. For institutions looking to target the startup executive segment, we offer:

- AI-led persona creation frameworks

- Equity event prediction models

- Advisor workflow orchestration layers

- Integration accelerators for CRM, RMs, and onboarding platforms

The outcome? A smarter, faster, and more empathetic wealth platform, tailored to startup-era wealth.

Closing Note: The Future of Wealth Is Being Written by Founders

They are young. They are liquid. And they are underserved.

The traditional HNW lens doesn’t capture the nuance of startup executives. Serving them well requires a reimagination of engagement – where insight is proactive, advisory is digital-first, and the human touch is augmented by AI.

Because in the age of startup liquidity, wealth management can’t just be reactive. It has to be real-time.

And startup executives are just the beginning. The same platform principles – real-time insight, persona-led design, and proactive AI – can scale to serve other fast-growing, underbanked HNW personas. Think: digital creators monetizing IP, gig entrepreneurs scaling personal brands, or athletes entering new wealth cycles. A well-designed wealth platform isn’t just a product. It’s an extensible ecosystem for the new faces of global affluence.

Let’s Talk

If you’re:

- A Private Banking or WealthTech Leader looking to build relevance with the next wave of HNW clients, we’d love to explore how AI-powered engagement can deliver trust at the speed of liquidity.

- A Head of Digital or Customer Strategy reimagining advisor journeys and onboarding models, we can show you how persona-driven orchestration unlocks speed, scale, and affinity.

- An Industry Analyst or Innovation Partner tracking AI’s real impact in wealth management, we’re happy to share deeper frameworks, models, and proof points.

About the Author

As Senior Vice President, Ashwani Narang will lead the growth charter for Maveric Systems in the North America region, focusing on deepening client relationships, driving strategic expansion, and unlocking new opportunities within key banking accounts. Based in Dallas, he will be responsible for advancing Maveric’s presence across top-tier financial institutions by fostering trust, enabling value-led outcomes, and steering client success

As Senior Vice President, Ashwani Narang will lead the growth charter for Maveric Systems in the North America region, focusing on deepening client relationships, driving strategic expansion, and unlocking new opportunities within key banking accounts. Based in Dallas, he will be responsible for advancing Maveric’s presence across top-tier financial institutions by fostering trust, enabling value-led outcomes, and steering client success

View

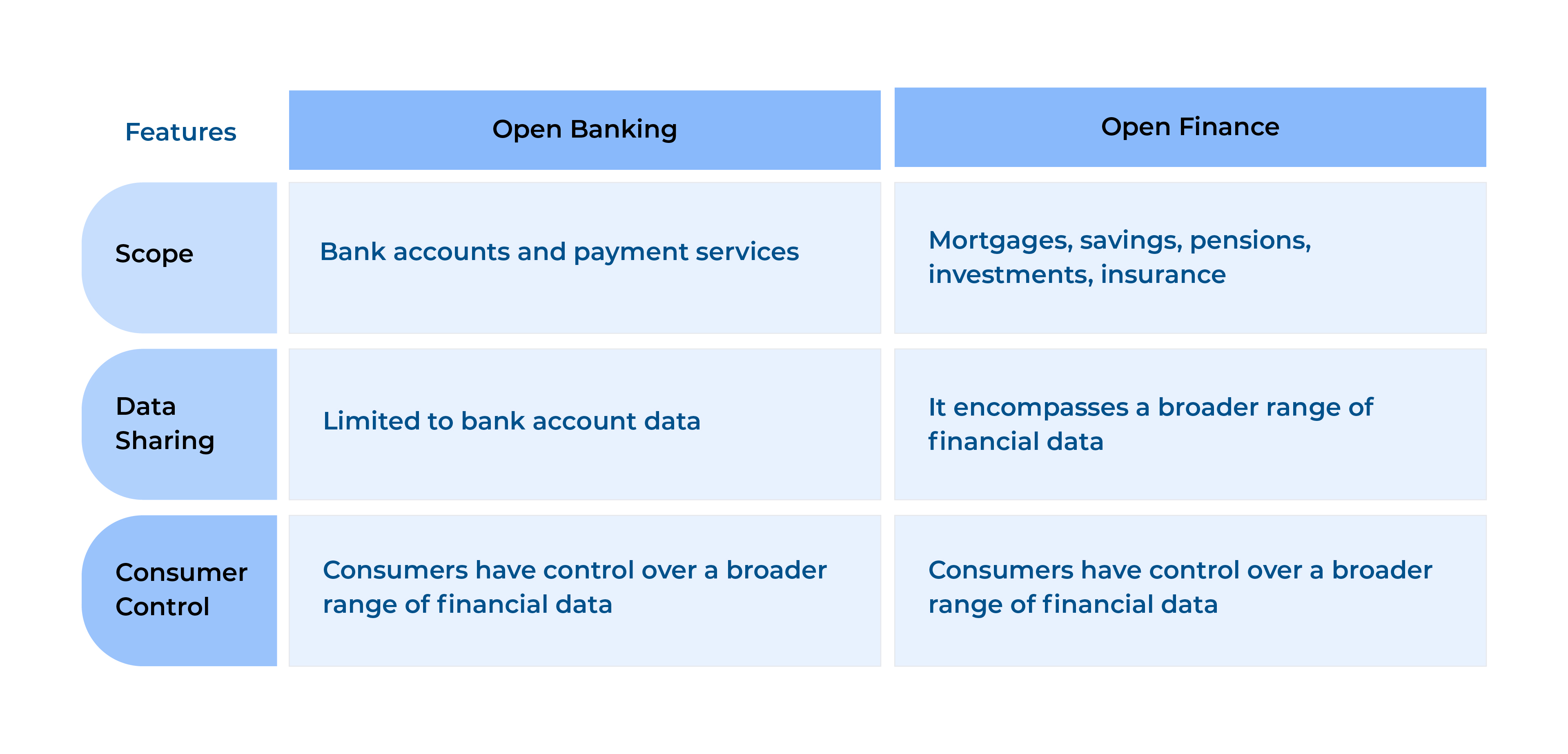

Open Finance represents a significant leap forward from Open Banking by addressing consumers’ expectations for greater control, convenience, and customization.

Open Finance represents a significant leap forward from Open Banking by addressing consumers’ expectations for greater control, convenience, and customization. Consumers want to make informed decisions based on a complete picture of their financial health, and Open Finance makes this possible. It is about putting consumers in the driver’s seat and empowering them to manage their financial lives more effectively.

Consumers want to make informed decisions based on a complete picture of their financial health, and Open Finance makes this possible. It is about putting consumers in the driver’s seat and empowering them to manage their financial lives more effectively. Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.

Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.

Financial institutions that embrace Open Finance initiatives and collaborate with experienced partners like

Financial institutions that embrace Open Finance initiatives and collaborate with experienced partners like  Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.

Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.