Tokenization: The Game-Changing Shift in the Investment Landscape

In an era of rapid technological advancement, tokenization has emerged as a transformative force, fundamentally reshaping our perception and management of assets. This innovative process is not merely an incremental improvement; it represents a seismic shift in the investment world, unlocking unprecedented opportunities for seasoned investors and newcomers alike. Let’s delve deep into the revolutionary impact of tokenization on the investment landscape.

Demystifying Tokenization: The Digital Alchemy of Modern Finance

At its core, tokenization converts rights to an asset into a digital token on a blockchain or similar distributed ledger technology. These digital tokens are a proxy for real-world assets, ranging from tangible properties like real estate and fine art to intangible assets such as stocks, bonds, and intellectual property. By harnessing blockchain technology’s robust security and unparalleled transparency, tokenization ensures that each transaction is encrypted, immutable, and traceable, establishing a new gold standard for security and trust in the financial world.

According to a report by the World Economic Forum, tokenized markets could reach $24 trillion by 2027, representing a staggering 10% of global GDP. This projection underscores the transformative potential of tokenization across various asset classes and industries.

The Multifaceted Benefits of Tokenization: A New Frontier in Investment

- Unprecedented Liquidity Injection

One of the most revolutionary aspects of tokenization is its ability to infuse liquidity into traditionally illiquid assets. Assets like real estate or fine art, typically requiring significant time and resources to sell, can now be easily tokenized and traded on digital platforms. A study by BNY Mellon revealed that tokenization could increase liquidity in private markets by 50-80%, dramatically reshaping investment dynamics.

- Democratization through Fractional Ownership

Tokenization shatters the barriers to entry for many high-value investments by enabling fractional ownership. This democratization allows smaller investors to participate in markets previously dominated by large institutional players. For instance, a $50 million commercial property can be divided into 50 million tokens, each worth $1, making it accessible to a broader range of investors. A report by Deloitte suggests that this democratization could lead to a 20-30% increase in retail investors participating in alternative investments by 2025.

- Unparalleled Transparency and Security

The underlying blockchain technology ensures that all transactions are transparent, traceable, and secure. Each transaction is recorded on an immutable ledger, significantly reducing the risk of fraud and enhancing trust among investors. A study by PwC found that blockchain-based systems could reduce financial fraud by up to 50%, potentially saving the industry billions annually.

- Cost Reduction and Efficiency Maximization

Traditional asset transactions often involve a complex web of intermediaries, extensive paperwork, and time-consuming compliance checks. Tokenization streamlines these processes, enabling faster transactions with fewer intermediaries. Research by McKinsey & Company indicates that tokenization could reduce transaction costs in private markets by 30-50%, translating to billions in savings across the global financial system.

The Horizon of Tokenization: Navigating the Future

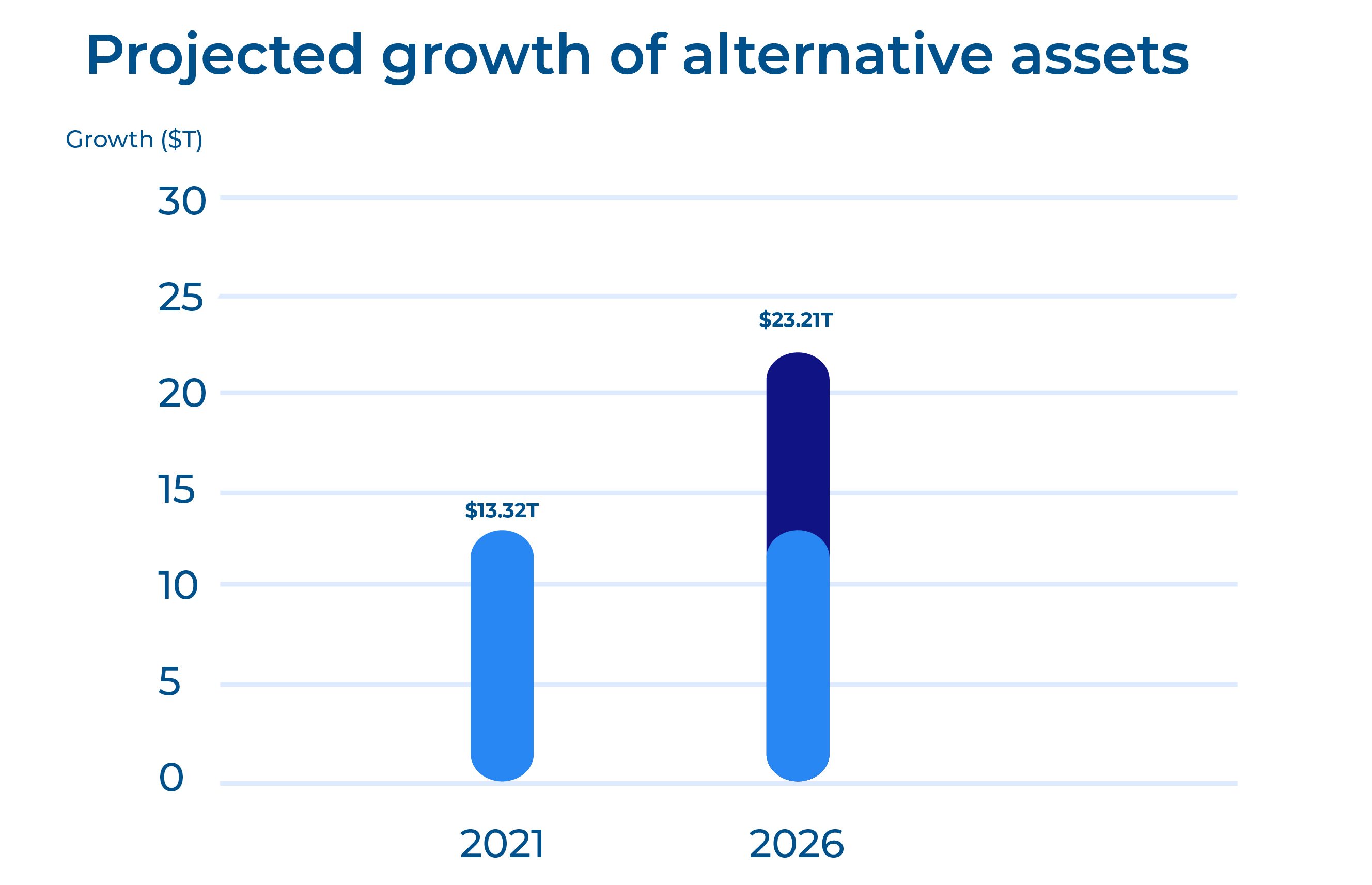

As tokenization technology matures, its adoption is poised for exponential growth. More asset classes are expected to be tokenized and traded on sophisticated digital platforms, reshaping the investment landscape. A report by Finoa predicts that the total market cap of tokenized assets could reach $4 trillion by 2025, growing at a CAGR of 50%.

Conclusion: Embracing the Tokenization Revolution

Tokenization stands at the forefront of a financial revolution, poised to redefine the very fabric of investments. By enhancing liquidity, enabling fractional ownership, and dramatically increasing transparency and efficiency, tokenization democratizes access to various assets and creates a more dynamic, inclusive investment ecosystem.

As we stand on the brink of this new era, the question for investors, asset owners, and financial institutions is not whether to embrace tokenization but how quickly they can adapt to this paradigm shift. Those who recognize and harness the transformative power of tokenization will be well-positioned to thrive in the rapidly evolving landscape of 21st-century finance.

The tokenization revolution is here. Are you ready to participate in this historic transformation in investments?

Citations and Further Reading

Co-authored by Venkatesh Padmanabhachari, Avinash Dave, and Sagar Rathore

Maveric’s thought leadership series – E.D.G.E (Experiences Delivered by Global Experts) – handpicks the game-changing technology ideas and pressing functional questions Banks and financial institutions must solve today.

These features – reports, whitepapers, podcasts, flyers, blogs, and infographics – are for Banking leaders and Technology evangelists to apply profound trends, the latest opinions, and transformational analyses to boost the performance of their organizations.

About Maveric Systems

Established in 2000, Maveric Systems is a niche, domain-led, BankTech specialist, transforming digital ecosystems across retail, corporate, wealth management, cards & payments and lending domains. Our 2600+ specialists use proven solutions and frameworks to address formidable CXO challenges across Customer Experience, Assurance, Regulatory Compliance, Process Excellence and New age AMS.

Our competencies across Data, Digital, Cloud, DevOps, AI and automation helps global and regional banking leaders as well as Fintechs solve next-gen business challenges through emerging technology. Our global presence spans across 3 continents with regional delivery capabilities in Amsterdam, Bengaluru, Chennai, Dallas, Dubai, Kingdom of Saudi Arabia, London, New Jersey, Pune, Riyadh, Singapore, Sweden, Dubai and Warsaw.

Our inherent banking domain expertise, a customer-intimacy-led delivery model, and differentiated talent with layered competency – deep domain and tech leadership, supported by a culture of ownership, energy, and commitment to customer success, make us the technology partner of choice for our customers.

View