How have payment methods evolved and how do transactions take place in our banking platform?

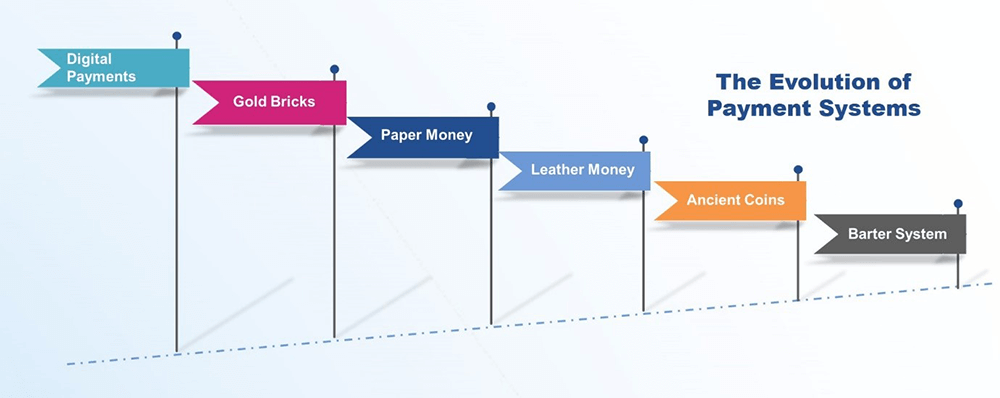

Buying things and paying for them is a regular part of our everyday life and we do it numerous times in a day. The biggest point to ponder here is how we have emerged in the world of payments. We are literally moving away from the days of pocket carrying leather wallets to digital wallets.

In the earlier days, trade use to happen in exchange of material goods, then slowly we emerged to payments in the form of ancient coins and it moved further in the form of leather money. Post which, paper based bank notes were issued by respective country authorities generally backed by Gold bricks. There are few other modes of payments made based on bill of exchange, debtor paying for creditor and cheque issuance. Eventually when the internet and technology evolved, all the current banking payments took the shape of digital payments.

The Growth Potentials

The technological advancements offer a vast potential for new payment services, from the acceptance of existing banking payment channel capabilities to the latest requirements of these new payment channels. Thus, we get introduced to new fundamentals and concepts for payment process right from payment initiation or receipt to execution. Majority of users in all countries have regular access to internet services and the expansion of digital network is even more advanced.

Payment services are strongly governed by banking regulations and country specific rules, which keeps progressing on a regular basis. Interestingly, nowadays payment services are not purely the interest domain of banks anymore, payment fintech innovators such as Paypal, Chase, Apple Pay etc offer multiple payment products and services. For seamless payment processing, every such payment innovator also has to connect to the existing banking infrastructure and payment systems.

Statista has estimated that the total transaction value in the digital payments segment is projected to reach $ 10,520,219 million by 2025, growing at an annual growth rate of 12%. As payments processing volumes are growing with increasing diversity of customer demands, the areas such as digital payments modes, real-time payments, fraud monitoring and many aspects of processing are put under severe pressure within a bank’s functional system.

The emphasis is now, more than ever, on cost efficiency, better risk management, and building a resource-light digital platform for servicing customers, this has, in turn, accelerated the need to scale up technology within the banks.

Adoption of Temenos Payments HUB (TPH) in today’s digital payment world:

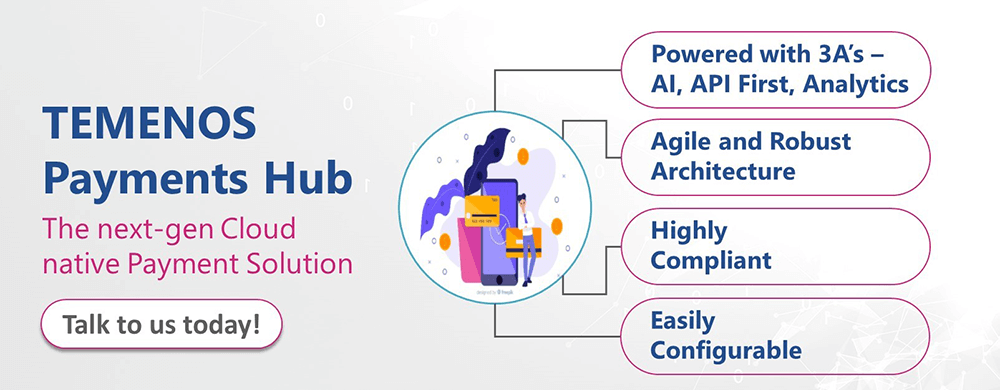

The true real time digital core banking system with a payments hub designed by Temenos offers an excellent breadth of new-age functionalities and ample levels of flexibilities. Through smart configurations, TPH can easily meet the ever rising payment demands. Banks can now offer their customers a seamless payment experience which offers straight through processing (STP) and provides a 360° view of all transactions in real-time and have a workflow for priority based payments processing. Thus, the Temenos payments hub more commonly known as TPH rules the digital payments world by facilitating easy arrangement at customer level for any payment volume or value.

Hassle-free instant payments

TPH is a one single real-time 24/7 platform which supports instant payment processing. The need for Instant/immediate payments has already taken its immense stride in the evolution of the payments market. It emphasizes the digitization of the supply chain in which real-time payments enable corporates to concentrate on their business priorities rather on the invoice payment and its subsequent processing. Additionally, the data of such transactions can be viewed in a real time with adequate financial insights on the fly. TPH has unrivalled STP (straight-through-processing) based on native functionalities with exception handling.

The robust architecture of TPH allows customers to seek intelligence of any payment transactions at given point of time. TPH can address global payments, instant payments and all the expectations of ISO20022 and real time settlement clearing.

Legacy Processes

More than digital, payments requirements is greatly differentiated by region and banks need to be more active in this space, and still there are use of cheques in certain regions and it is essential that banks move existing customer base from cheques to digital payments particularly if instant payments process has to succeed. Regardless, it is essential for bank’s payment system to be easily adaptable to the changing needs of their customers and country regulations. TPH has the capabilities on the broader payment ecosystems and has the additional solution of Financial crime mitigation and repair option enabled.

Built with Open API’s for Open Banking

Open banking has taken the banking industry by a storm with the introduction of Open API’s. Through Open API’s, banks have been provisioning and granting third-party services. TPH is an API enabled payment solution that offers a seamless integration service with the core banking platform to make sure STP is a success, a truly digital customer experience. It manages routing to all downstream payment processing systems based on rules. For example, all real-time payments can be routed to TPH for execution and route low value (e.g. ACH) payments through an existing legacy system, supporting progressive renovation.

Ensures Payment Compliance

TPH is built with a strong regulatory engine which has a close eye on country level compliance and governance requirements (e.g., PSD2). Supporting reporting requirements institutionalized by regulatory bodies or financial ministry is a matter of click for use cases such as submissions of financial documents and reports related to payment transactions, customer bank account details and other related payment information.

Conclusion

Payments are becoming increasingly important and seamless experience is essential for survival. The rise of digital payments enabled by latest technologies will lay a foundation for superior experience. Corporates will expect manual processes to be replaced with digital methods that are quicker, cheaper and incur less friction. TPH is an ideal solution, which has the capability of standalone deployment or can be embedded with Temenos Transact.

The banks should drive the back-office operations efficiently and the speed of fulfilment is also critical; the digital solution must therefore be front-to-back. Banks should perform friction-free back-office operations, and the back-office staff can work efficiently without any hassle. This ultimately comes down to using a single platform. Temenos payments can process to highly scaled up Tier-one payments volumes. A recent benchmark showed that it can process up to 10 billion payments per year and TPH supports this being highly parameterizable payment product. As one of the leading payment solutions, banks can lead the game of digital payments with TPH.