Enable Seamless Connectivity with Temenos’ APIs and Open Banking Capabilities

In today’s rapidly evolving digital landscape, connectivity, and integration are key drivers of success for financial institutions. Banks must embrace open banking and leverage robust API frameworks to adapt to changing customer expectations and regulatory requirements. This blog post explores how Temenos’ APIs and open banking capabilities enable seamless connectivity, empowering banks to offer innovative products, enhance customer experiences, and drive growth in the digital era. Partnering with domain experts in Temenos Core banking systems like Maveric Systems brings a stellar advantage for leading FIs to forge ahead in their digital transformation initiatives.

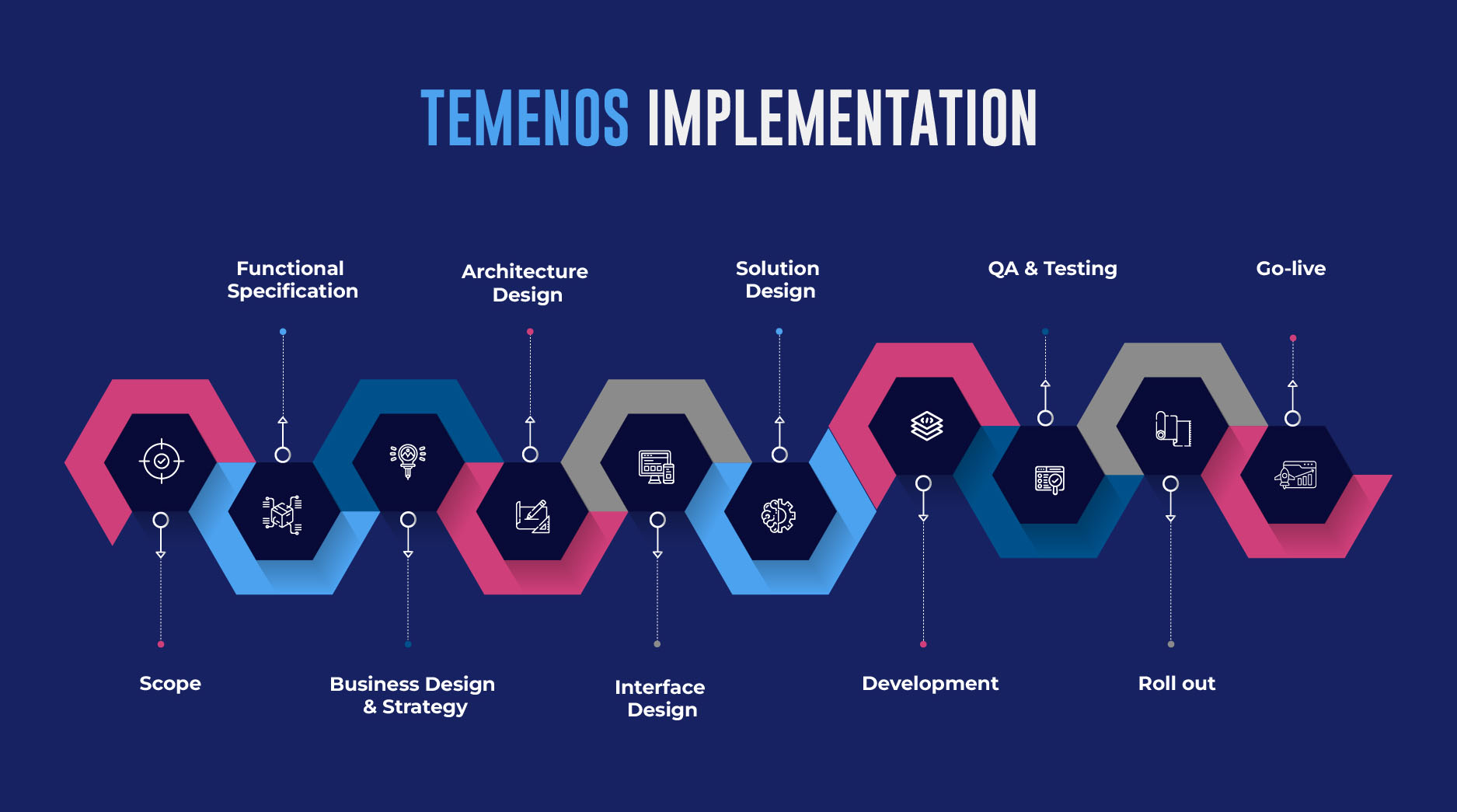

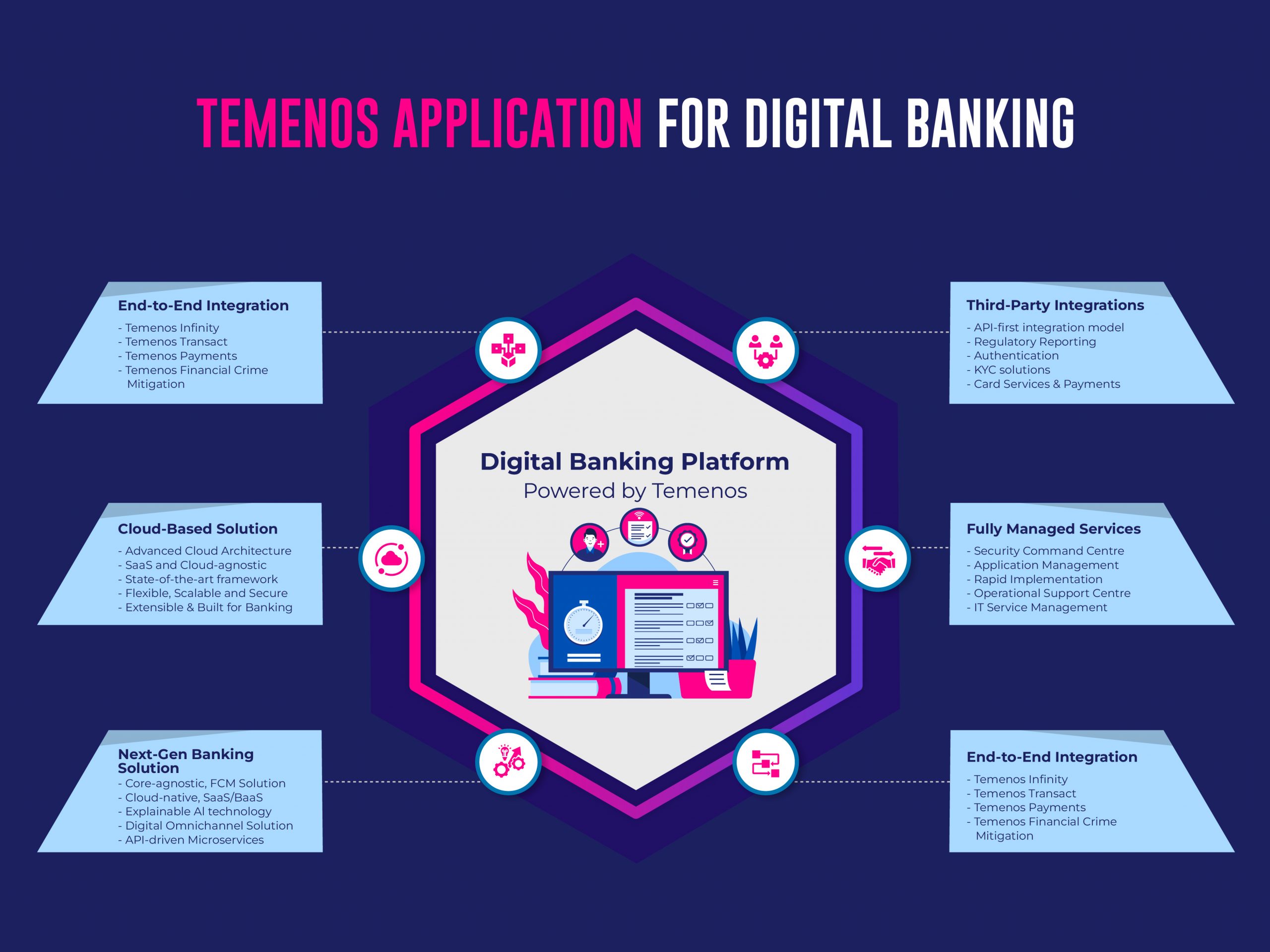

Understanding Temenos’ API Framework:

Temenos, a leading banking software provider, offers a comprehensive API framework that enables banks to expose and consume APIs securely and efficiently. With Temenos’ API-first approach, financial institutions can unlock their core banking capabilities and seamlessly integrate with third-party systems, fintech partners, and external data sources. The API framework comprises a set of well-documented and standardized APIs, facilitating rapid development, easy integration, and scalability.

Open Banking: Empowering Collaboration and Innovation:

Open banking is a regulatory-driven initiative that mandates banks to provide secure access to customer data through APIs to authorized third-party providers. By embracing open banking, financial institutions can foster collaboration with Fintechs, deliver innovative products and services, and enhance customer experiences. Temenos’ open banking capabilities enable banks to comply with open banking regulations while harnessing the opportunities it presents.

Benefits of Seamless Connectivity with Temenos’ APIs:

Enhanced Customer Experience:

Temenos’ API framework allows banks to create personalized and tailored customer experience. Banks can offer targeted recommendations, real-time financial information, and customized services by integrating external data sources and leveraging customer insights. Seamless connectivity enables customers to access their financial data, initiate transactions, and manage their accounts effortlessly, leading to higher customer satisfaction and engagement.

Accelerated Innovation:

Temenos’ API framework promotes collaboration with fintech partners, allowing banks to access various innovative solutions and services. By integrating with fintech ecosystems, banks can quickly bring new products to market, tap into emerging technologies, and meet evolving customer needs. The seamless connectivity provided by Temenos’ APIs accelerates the innovation cycle, enabling banks to stay competitive in a rapidly changing landscape.

Simplified Integration:

Integrating disparate systems and legacy infrastructure can be complex and time-consuming for banks. Temenos’ API framework simplifies integration efforts by providing standardized and well-documented APIs. This seamlessly connects banks to connect their core banking systems with various internal and external applications. The simplified integration process reduces costs, improves operational efficiency, and enables banks to leverage the full potential of their technology stack.

Increased Operational Efficiency:

Temenos’ APIs facilitate seamless connectivity between different systems within a bank’s ecosystem. Banks can streamline operations and reduce manual interventions by automating data flows, transaction processing, and information exchange. The increased operational efficiency translates into faster transaction processing, improved data accuracy, and reduced operational risks.

Regulatory Compliance:

With the rise of open banking initiatives worldwide, compliance with regulatory requirements is a critical concern for financial institutions. Temenos’ API framework includes built-in security and compliance features, ensuring data protection, secure access, and consent management. Banks can authenticate and authorize access to customer data, monitor data usage, and maintain control over the APIs, complying with regulations while safeguarding customer privacy.

Scalability and Future-Proofing:

As banks grow and evolve, scalability and future-proofing become vital considerations. Temenos’ API framework is designed to support the scalability requirements of financial institutions. Banks can scale their API infrastructure based on increasing demand, add new features and services, and seamlessly integrate with new technologies. This future-proofing capability enables banks to keep pace with fluctuating market dynamics and stay ahead of the curve.

Conclusion

In the digital banking landscape, enabling seamless connectivity through robust API frameworks and open banking capabilities is crucial for driving innovation, enhancing customer experiences, and ensuring regulatory compliance. Temenos’ API framework empowers financial institutions to unlock their core banking capabilities, integrate with third-party systems, and collaborate with fintech partners. By leveraging Temenos’ APIs, banks can offer personalized services, accelerate innovation, streamline operations, and comply with regulatory requirements. Embracing seamless connectivity through Temenos’ APIs and open banking capabilities positions banks to thrive in the digital era and deliver exceptional value to their customers.

About Maveric Systems

Starting in 2000, Maveric Systems is a niche, domain-led Banking Tech specialist partnering with global banks to solve business challenges through emerging technology. 3000+ tech experts use proven frameworks to empower our customers to navigate a rapidly changing environment, enabling sharper definitions of their goals and measures to achieve them.

Across retail, corporate & wealth management, Maveric accelerates digital transformation through native banking domain expertise, a customer-intimacy-led delivery model, and a vibrant leadership supported by a culture of ownership.

With centers of excellence for Data, Digital, Core Banking, and Quality Engineering, Maveric teams work in 15 countries with regional delivery capabilities in Bangalore, Chennai, Dubai, London, Poland, Riyadh, and Singapore.

View