Why Onboarding Is Banking’s Most Expensive Unsolved Problem

Onboarding sits at the intersection of two competing demands that no digital solution has fully reconciled: regulators require absolute thoroughness; customers expect instant access. North American banks have spent a decade solving this as a UX problem – simplifying forms, reducing fields, refining mobile flows. The result has been marginal. Self-service reduced the headcount required to input data, but the underlying architecture – document review, address validation, KYC screening, AML checks – remained sequential, rule-dependent, and slow.

AI makes customer servicing an inference problem, not a journey-mapping problem. The question shifts from ‘Is the digital journey working?’ to ‘How can we dynamically orchestrate the right outcome without the customer having to do the work?’

This reframing changes everything downstream – from the data architecture required to the compliance model deployed to the servicing platforms built. AI in banking does not optimize the existing onboarding process; it replaces its core logic.

Three Structural Shifts AI Brings to Bank Onboarding

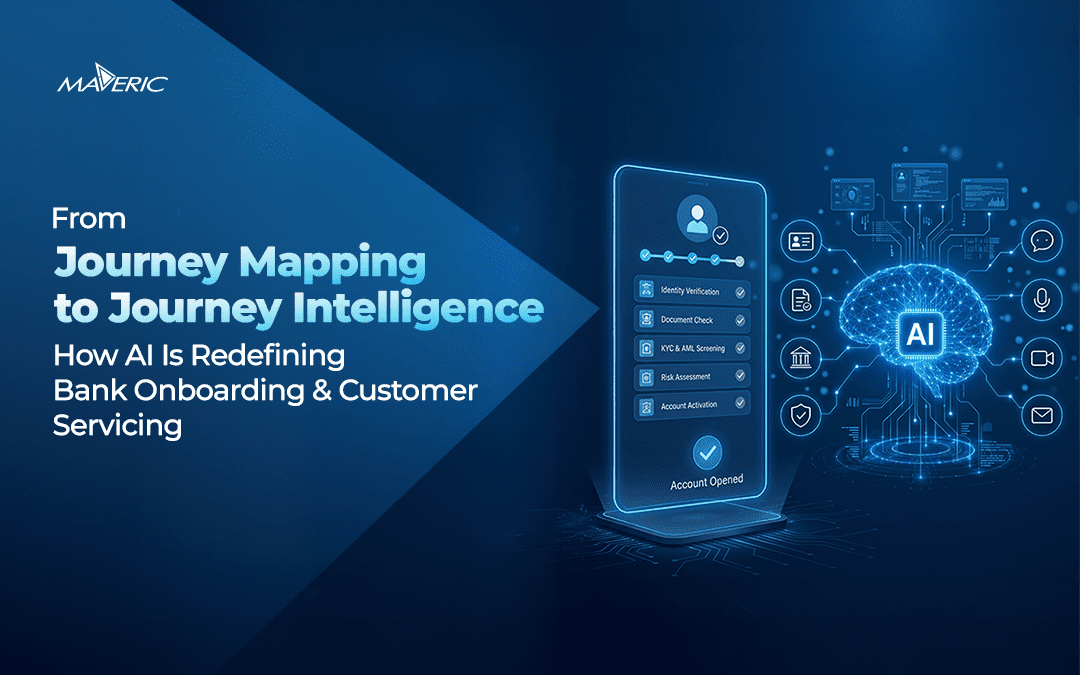

From Self-Service to Zero-Service

Digital banking introduced self-service – which simply meant the customer typed their own data instead of a teller doing it. Agentic AI advances this to zero-service. Through intelligent data orchestration, AI solutions proactively pull contextual information from CRM records, government registries, third-party data providers, and digital behavioral footprints – without requiring customer input at each verification step.

In Maveric’s implementations for regional banking leaders, this capability reduced customer onboarding times from hours to completion in as few as 8 to 10 clicks through AI-powered verification and account opening. For institutions competing against digital-native challengers in the North American market, near-instant account activation has moved from differentiator to baseline expectation.

Contextual Risk Stratification

The traditional delay in onboarding is the human effort required to review documents, validate addresses, and resolve exceptions against rigid, static checklists. Agentic workflows now handle this validation continuously and contextually. Rather than applying a uniform review process to every applicant, AI evaluates each customer’s specific risk profile in real time.

Low-risk applicants receive straight-through processing. High-risk anomalies are intelligently routed to compliance officers with an AI-generated brief – a summarized context of why the escalation occurred, the specific signals that triggered it, and recommended resolution steps. This is not a cosmetic efficiency gain; it is the mechanism by which AI compliance in banking moves from reactive to anticipatory.

Unified KYC, AML, and FCM Infrastructure

Know Your Customer, Anti-Money Laundering, and Financial Crime Management have historically operated as separate compliance disciplines with siloed tooling. This separation generates data redundancies and inflates false-positive rates that consume compliance officer capacity without improving fraud detection accuracy.

AI enables the convergence of these disciplines into a unified risk infrastructure. By processing plural sets of unstructured and structured data concurrently, AI builds a continuously updated risk picture of each customer across all three compliance domains simultaneously. Banks that architect this KYC-AML-FCM convergence from the outset realize substantially higher fraud-loss reductions and avoid the integration debt that accrues when these systems are connected retroactively.

Beyond Chatbots: The Case for Multimodal Customer Servicing

The limitations of first-generation chatbots are well understood. Rigid decision trees fail the moment a customer’s issue falls outside the programmed taxonomy – producing frustration, escalation, and compounding handle time. These systems were digital, not intelligent; they automated scripts rather than understanding intent.

AI resolves this by introducing genuine multimodal capability across the servicing layer. Digital banking gave customers multiple separate channels. AI gives banks a single intelligence layer capable of seamlessly processing and pivoting between text, voice, image, and video within one interaction, interpreting customer intent regardless of the mode it arrives in.

When a customer struggles to understand textual instructions, the AI does not repeat the text – it interprets the confusion and dynamically generates a personalized visual walkthrough. When escalation is necessary, it transfers complete context including sentiment analysis and recommended resolution steps, so the receiving agent does not start from zero.

90% First Call Resolution rate achieved by a global bank through Maveric’s AI-driven Agent Assist and Intelligent Knowledge Management platform

That outcome – an industry-leading First Call Resolution rate – was made possible not by adding agents but by deploying more intelligent routing, real-time context transfer, and continuous knowledge management. It is a precise illustration of what trusted AI in banking looks like in production.

Architecture Implications for Banking CIOs

Design for multimodal from day one: Retrofitting multimodal capability onto a channel-based architecture is expensive and produces fragmented experiences. CIOs must specify multimodal requirements at the platform design stage, not as an enhancement cycle planned for a future release.

Unify compliance infrastructure early: The cost of building KYC, AML, and FCM as separate systems and connecting them later substantially exceeds the cost of building convergence into the initial architecture. The fraud-loss reductions and false-positive reductions that follow justify the upfront design investment.

Measure outcomes, not activity: Handle time and call volume are activity metrics. First Call Resolution, customer effort score, onboarding completion rate, and fraud detection accuracy are outcome metrics. AI-first banks track the latter – and they report them to the board, not just to operations.

AI in banking is not an enhancement to the customer journey – it is a replacement of its underlying logic. Institutions that recognize this early and architect accordingly will set the servicing benchmarks that define the next decade of North American banking. Read more on the complete strategic and architectural framework in the whitepaper – From Digital-First to AI-First: The Mandate Reshaping the Banking CIO Agenda

Frequently Asked Questions

How does AI reduce bank customer onboarding time?

AI reduces onboarding time by replacing sequential, human-dependent document review with intelligent data orchestration. Agentic systems proactively pull verification data from government registries, CRM records, and third-party providers, enabling low-risk applicants to complete account opening in minutes rather than hours. High-risk cases are routed automatically to compliance officers with context already assembled, eliminating the rework of manual review.

What is the difference between a rule-based chatbot and an AI-powered servicing agent?

A rule-based chatbot navigates customers through a pre-programmed decision tree. If the issue falls outside defined rules, the bot fails. An AI-powered servicing agent understands context, interprets intent across text, voice, image, and video, dynamically generates responses, switches modes based on customer need, and escalates with full context intact – including sentiment analysis and recommended resolution steps.

What is unified KYC-AML infrastructure and why does it matter for AI compliance in banking?

Unified KYC-AML infrastructure consolidates Know Your Customer, Anti-Money Laundering, and Financial Crime Management into a single AI-driven risk layer rather than managing them as siloed programs. The result is fewer data redundancies, significantly lower false-positive rates, and substantially higher fraud-loss reductions. Banks that build this convergence from the outset avoid the integration debt of connecting systems retroactively and establish a foundation for responsible, explainable AI compliance from day one.

How do North American banks measure ROI from AI in customer servicing?

ROI should be measured across three dimensions: operational KPIs such as onboarding turnaround time and cost per interaction; business KPIs including fraud loss reduction and customer retention rates; and trust KPIs covering model explainability and regulatory auditability. First Call Resolution rate is a particularly high-signal metric for contact center AI effectiveness.