Flipping the odds for digital transformation success in the Banking and Fintech industry depends on customer experience. An influential study that dissects digital transformation success pegs banking as having the second highest rate after Telecom, Media, and Tech sectors.

Reviewing the key imperatives that bring digital transformation success – such as integrated strategy, leadership commitment, agility in governance, or Tech platforms that combine data and digital – ultimately pivot around one common element: Customer Experience.

This blog deepens into the Banking CX aspects and elaborates on best practices.

The Banking or Fintech Customer Journey.

Starting with an impulse, or a need for information, a typical banking customer journey comprises many interactions that culminate in the customer’s decision to purchase.

While each action may appear hidden, it touches a specific part of the banking organization – whether the operations model, processes, or the core technology platform.

Before addressing the best practices that govern customer experience journeys in banking, let’s round up the top three errors that are often costly.

- Significant investments in digital banking solutions may be focused on CX but do not integrate well with the organization’s back-end machinery (processes, regulatory, and risk protocols)

- Business and Technology tracks may be misaligned in their CX priorities and responsibilities.

- Siloed organizational behavior may be content with incremental improvements and miss out on the quantum opportunity to overhaul the organization’s CX capabilities.

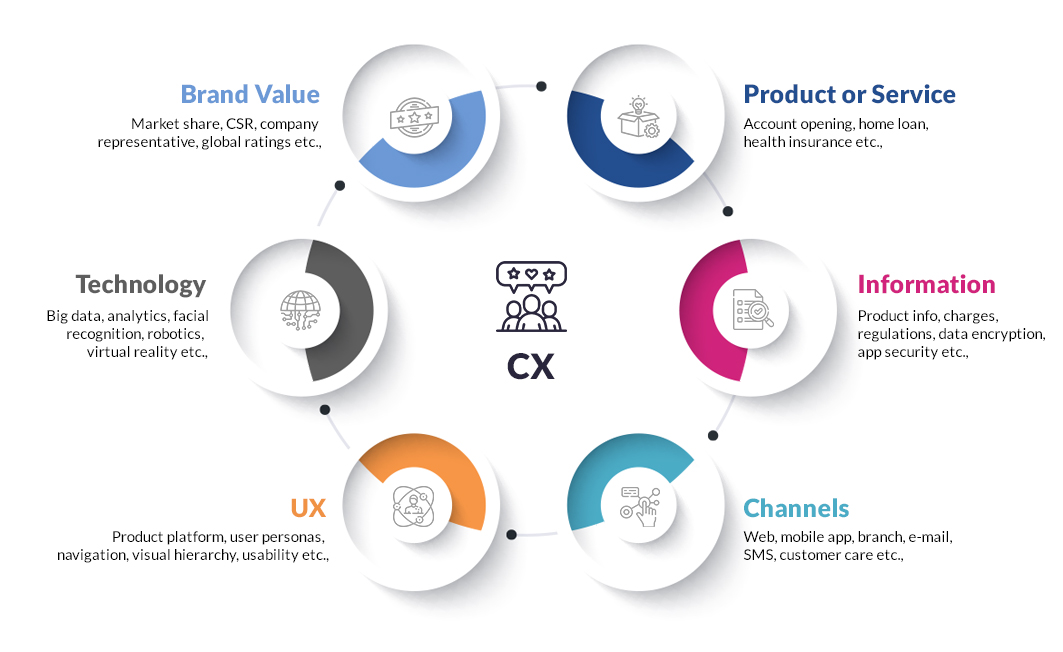

CX components detailed

Managing Customer Experience in the Fintech Industry – Three Critical Practices

While many generic best practices apply across industries – listening to customer feedback and taking prompt actions, Improving the UX and UI touchpoints, and going omnichannel – let’s focus on niche CX best practices and their underlying mechanisms.

People First, Technology Second.

Be it chatbots and virtual assistants for consumer education, creating seamless UX that is intuitive, or learning from specific digital native audiences, one profound principle for designing successful banking CX programs is – to think of customers from a 360-degree perspective.

So even if an AI use-case experimentation is underway and reams of customer analytics data are revealed, it is pertinent to connect it to customer behavior, preferences, and pain points. When technology is complementary to customer-centricity principles, banks can create hyper-personalized experiences that customers demand today. The overarching lesson is that banks must see customers as co-creators and evolution partners.

Automating for Frictionless CX

The efficiency of customer service (and overall CX) can be enhanced through the automation of administrative tasks. End-to-end automation is an excellent choice for extensive, repetitive procedures, as digital data extraction makes it possible to verify and validate documents with ease.

Notifying, communicating, and providing access to information with customers is often a straightforward automated process. For creating a bank account, it is easy to collect and verify relevant consumer information across several platforms and under specific criteria.

This can be automated entirely, relieving stress from the already-burdened staff in the banking industry. Automation facilitates quicker service, boosts client loyalty, and directly impacts the top and bottom-line metrics.

Embracing the Trust Equation.

To rid customers of their confusion or anxiety is to gain instant trust.

A widely cited Banking Trust Barometer report highlights how a climate of “information bankruptcy” can erode an organization’s immediate and longer-term reputation. So, while customers’ involvement may be restricted to opening an account, applying for a home loan, or buying a specific insurance product, it is pragmatic for banks to educate them across the more significant aspects of the economic outlook, market, and investment trends, and noteworthy regulatory changes that they should anticipate.

A successful banking CX program evaluates various UX, and UI touchpoints from the lens of “Trust created Vs. Trust lost.” Consider, for instance, the Monzo lending app that uses reminders to ensure customers celebrate their on-time payments or the TransferWise app that offers pricing calculators for customers to understand their charges – two examples of bolstering customer confidence at appropriate moments in their journey.

Finally, how big is the “CX-stakes”?

A BCG research study credits exceptional CX as the springboard that differentiates the market leaders – Amazon, Apple, and Google.

Seen across a ten-year run, companies with higher customer satisfaction scores quickly generate twice the shareholder value over the average performers.

The firms report higher price-to-earnings ratios, greater total shareholder returns, and better earnings.

Conclusion

While the entire digital transformation journey for banks involves processes, rules, engines, scalable tech-ops, governance compliance, and increasing usage of intelligent self-learning systems, the gains of doing the right thing at the right time (or the CX-beneficial actions as mentioned above) will be rewarding in the longer term.