In 2017, American banks collected 34.3 billion dollars in overdraft fees. (link). The average value for an overdraft fee is $ 30 in the United States. This means that the average American ended up paying $ 125 in overdraft fees. In a world where the share of digital payments is growing rapidly, a digital assistant (or ABAs – Automated Banking Assistants) can help avoid such situations.

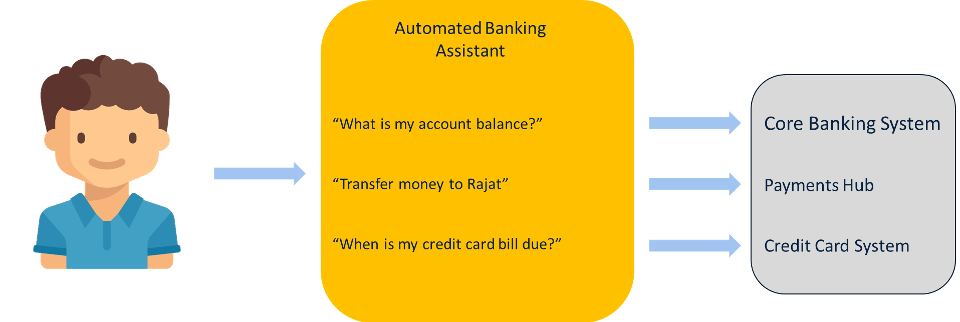

How Do ABAs Work?

AI Benefits the Business:

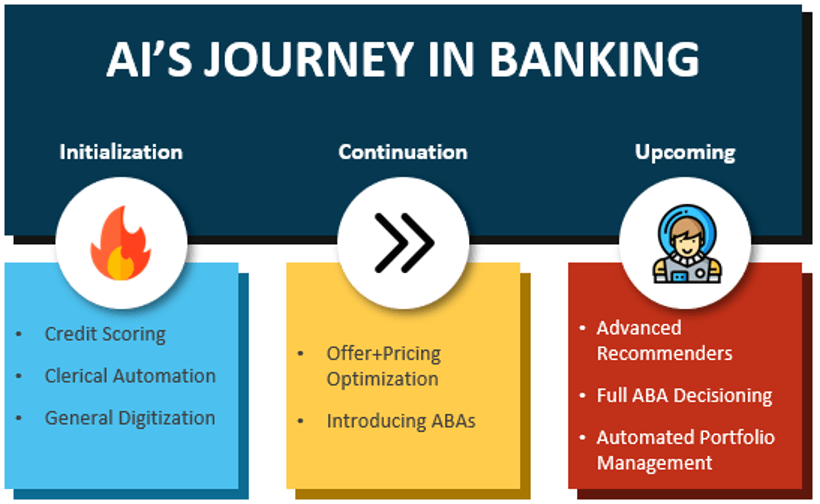

For decades, banks have used AI to automate their credit decisioning processes. From simple rules-based systems, they have have now evolved considerably. Products like Mindbox® have been used by mortgage servicers to predict questions that might be asked based on a customer’s past behaviour, recent transactions and their loan disposition.

By 2022, about 90% of all client banking interactions will be handled by Automated Banking Assistants (ABAs), saving $8 Billion annually (source). In addition to cost savings, the improved turnaround time will encourage the ABA to cross sell other bank products, thus actively expanding our business.

AI Benefits Consumers:

In developing countries, customers do not have the pervasive problem of overdraft fees. However, they can sometimes be careless with spending. Many of them engage in grey spending – paying for Netflix but never watching it, getting a 12-month gym membership, but dropping out. Third Party Apps like ‘AskTrim’ allow customers to not only to list out their spending but will also negotiate costs on Internet/ Phone bills. Consumers can also use the app to make timely payments, avoid fees and gain insight into their own spending

Banks were not far behind in introducing proprietary Automated Banking Assistants (ABAs), their reasoning being manifold. Good in-house chatbots would reduce the reliance on outside party apps, be safer, quicker, and give the bank more control on their interactions with customers. In addition, switching customers to automated advisors will help banks lower customer service costs.

Recent Developments:

Bank of America introduced an Automated Bank Assistant, ‘Erica’. It reached 1 million users in 2 months, Facebook took 10 months. ‘Erica’ supports advanced functionality like money transfers, account lockdowns and detailed transaction summaries.

When it comes to financial products, banks cannot afford to get recommendations wrong. Banks cannot make incorrect recommendations and subsequently reject customers for specific products. Likewise, Banks cannot make approvals that are not in line with the bank’s risk appetite. The former results in poor customer experience and the latter could directly impact the bank’s reputation. Hence, it is important that banks focus on making relevant offers to customers.

Banks often use the concept of ‘Next Best Offer’ or ‘Next Logical Product’ to best serve customers with complementary products to those already availed. Global banks have used event prediction techniques like Markov Chains to inform businesses of how likely customers are to adopt a new product (or even close an existing relationship). This would answer questions like:

“What is the probability that a customer will add a home loan to their product portfolio if they already hold 2 FDs and 3 credit cards?”

“What are the chances that a credit card will cancelled by a customer, now that they have a personal loan at a lower rate than what they were revolving at?”

Banks in developing economies have also started using such advanced analytics techniques. Let us discuss what we expect to see in the coming decade.

Improved Performance & Improved Adoption Cycle – A Virtuous Circle

Recommendation Systems are reactionary and obviously need a fair amount of previous data. In the next decade, an improvement loop will emerge – better services will attract more usage, which will give us better data to improve our services further. It is a classic case of more people using an improved product which drives even more innovation.

As innovation drives all forms of ABAs, we expect to see them in various regional languages – this will promote parity in banking.

Automated Portfolio Management

We expect to see many other sources of data being incorporated through the ABA system – like stock ticker data, detailed views for ETFs. The information parity coupled with an increased trust in automated systems will allow the average customer to be better invested in market instruments. We will no longer depend on fund managers and brokers.

Real time decisioning

Today’s automation revolves around process optimization, not decisioning. When we ask for a reduction of APR or an overdraft charge to be reversed – any time a money related decision is to be made, we always encounter a human who decides. They might consider the longevity of our banking relationship, number of favours we have asked of the bank in the past, amount of money in our account and a variety of other factors – but why can’t an ABA decide in the future?

The 2020s will be a revolutionary era for banking. The need for automation and convenience is implicitly obvious. We have many technologies that are already used in the tech industry that will translate seamlessly into the banking sector – for now we are only waiting on compliance. The next decade will become a time for us to bank and invest with more inclusivity, transparency and confidence. And of course, we hope to not talk to our bank tellers and branch managers again.

This was originally published on Finextra website and is being reproduced here.

https://www.finextra.com/blogposting/18829/beyond-chatbots–conversational-ai-in-banking