Digital is the new imperative that is driving the banking and finance industry across the world

Five years ago, an AT Kearney Study had said that digital is touted as a revolutionary transformation that will bring many new features, including any time and anywhere banking, ultra-fast response times and omnipresent advisors. So a natural question people asked then was, why don’t banks pick up the pace? And the answer was simply that the banking and financial institutions needed to make fundamental changes to the way they operated. Well, that was in 2013. In the five years since that report, we have seen some tremendous thaw in the industry which has completely embraced digital.

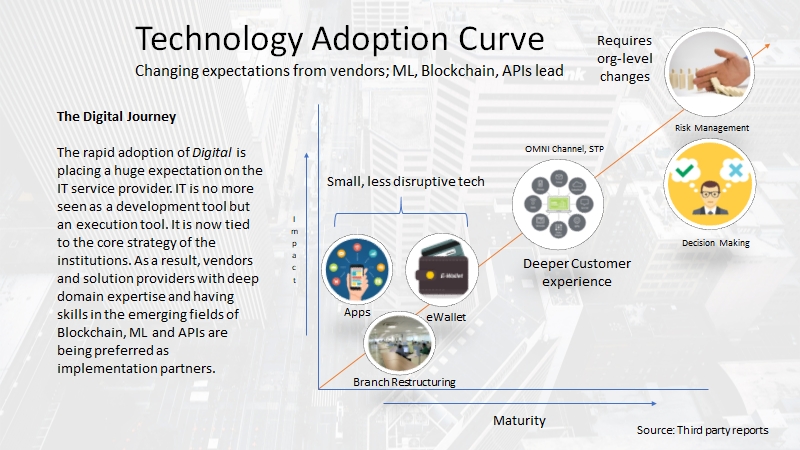

The big change is that Digital is no more seen in a silo of client experience alone. The question today is: how can digital help quicken business decisions, manage new risks effectively and adhere to compliances better. If the client experience really has to jump to a new level, institutions have realized that they should go deeper with digital and change legacy standards and protocols.

For instance, banks and financial institutions are serious about deploying Cognitive Computing to increase productivity by bringing in automation and using the power of data. Cognitive Computing is believed to bring in processes, data and analytics to the point where institutions can service customers at the speed of thought, match customer expectations with specialized products and portfolios on the fly.

To illustrate the point, we look at a couple of key developments. The UK banking system is being revamped. UK, considered to be among the most conservative countries when it comes to technology reforms and adoption in banking and finance. However, it is about to witness a sea change in its retail payment system. While UK market had opened up to digital at the client level, it had held off core banking reforms. This is set to change. The Bank of England has recently approved a new system that will bring in a new clearinghouse, a faster payment engine with new standards and protocols. The NPSO (The New Payment System Operator) in the UK is mandated with building the next generation Open Banking platform. This offers new product opportunities for developers and vendors. It also addresses security and standards requirements that the new digital calls for.

Cross-border payment platform Swift is deploying Blockchains to help corporates track their payment more precisely and pinpoint reasons for hold-ups and delays. Swift helps corporates look at the payment journey from a new viewpoint using Distributed Ledger technology giving vital insights to its corporate users. Whether they are documented components, the purpose of payment, each node in the chain certifying the transaction increases the trust in the network.

In the US, AIX, an AI-powered brokerage house is set to disrupt the decade’s old interdealer brokerage model using Cryptocurrency. AIX is close to disrupting the model where voice negotiation is key in tradings. Typically, a trader wants to execute a transaction, picks up a phone and communicates to other brokers, match prices and conducts the trade. The system needs highly skilled manpower to do it which is expensive. Now, AIX is deploying an AI engine called the Rainbow Cognitive Engine which takes trade information from traders and distributes it throughout the network and brings back relevant information to the original trader. It brings in all kinds of data points across the market through the AI engine’s built-in logic and optimizes the outcome. AIX’s compelling value proposition is that all the markets will be available for a trader on a single platform. One can trade in US bonds market and invest the proceedings into Euro currency market or into Cryptocurrencies for example.

If you check the state of digital push in various regions, we have come a long way. Historically, US, Canada, Australia, UK and central European countries were quite committed to going digital. The birth of Fintech in the Silicon Valley demonstrated the power of applying technology in the sector. Most institutions in these regions began partnering with the young fitech startups to offer value-added services. However, with the growth of data analytics and big data push, banks and financial institutions in the regions committed to Digital soon realized that unless their internal teams were aligned to these new technologies they would not be able to withstand the competitive wave blowing across the globe. This had a cascading effect as bringing new technology in-house mandated that the institutions need to change their internal processes and governance. These regions are now aggressively pursuing the goal of changing core systems to align with the Digital model.

Other countries have been little more cautious. The bolder among them were happy wetting their feet with online and digital value-added services and watch for signals from experiments in going deeper into Digital. However, a quick look at state-of-affairs in more conservative regions shows us that EMEA, South America, and Asia have all jumped on to the Digital bandwagon without reservations. India is one big example which has made a huge jump to digital with traditional banking and finance institutions partnering with fintech companies. Far away in Chile to things are changing rapidly. The San Diego-based Banco de Chile is moving very fast into digital solutions aimed at making customer experience easier. Not to be left behind the Islamic Banking players too have started offering online and digital experiences. These offerings match other solutions except they adhere to the Islamic banking rules.

It’s only a matter of time before Digital takes over the banking and financial sector. The last bastion is the Regulations and Compliance front. With Digital, new risks are emerging and the authorities are racing against time to promulgate new policies, standards, and protocols. If you see Basel 3 Regulations, be it the need to keep data protected, keeping a trail of all electronic transactions or providing complete information on the website for making the informed decision, it is amply clear on how Digital is gaining importance.

References:

Interview of the following people by TheBanker:

- Likhit Wagle, IBM

- Paul Horlock, Chief Executive Officer, New Payment System Operator (NPSO)

- Tom Halpin, global head of HSBC’s payment products

- Steve Compton of AIX

The AT Kearney Report: Banking in a digital world

IFF & McKinsey: The Future of Risk Management in the Digital Era