Creating Future-Ready digital wealth management platforms

The wealth management landscape is experiencing a profound shift as digital solutions reimagine how advisors serve their clients and investors manage their wealth. Digital wealth management platforms are at the forefront of this revolution, empowering financial institutions to provide personalized, data-driven advice at scale – all while enhancing client experiences. However, these platforms must evolve to meet rising expectations and embrace next-generation technologies to thrive in the future.

Why Future-Readiness Matters

In traditional wealth management, high-net-worth individuals (HNWIs) can access tailored advice and portfolio management. However, this model is often inaccessible to broader demographics. Digital platforms democratize wealth management, opening access to services historically reserved for an exclusive clientele. The future belongs to platforms that can balance this accessibility with the sophistication and personalization that clients demand.

Maveric Systems understands the nuanced challenges of wealth management, providing a robust foundation for implementing digital solutions. Their 3Cs Advantages of Contextualization, Competence, and Commitment ensure that digital wealth management platforms are designed with a deep understanding of industry dynamics, supported by technical expertise, and aligned with long-term strategic objectives.

Critical Elements of Future-Ready Platforms

Let’s explore what makes a digital wealth management platform truly future proof:

1) Hyper-Personalization:

AI-powered analytics can delve into a client’s financial profile, risk tolerance, and goals to create customized portfolios that are optimized and aligned with individual needs.

2) Holistic Financial View:

Platforms must integrate with a broad range of financial accounts, providing a consolidated view of an investor’s assets, liabilities, and overall financial health.

3) Gamification:

Engaging features like simulations, leaderboards, and educational content can boost financial literacy and make managing wealth an enjoyable experience.

Hybrid Models:

Blended “robo-advisory” models that combine algorithms with human advisor expertise will deliver an optimal mix of efficiency and personalized touch.

Seamless User Experience:

Intuitive interfaces and cross-device compatibility are essential to attract clients seeking accessible, user-friendly wealth management.

The Role of Emerging Technologies

Looking ahead, these technologies are poised to reshape the digital wealth management landscape:

Blockchain:

The potential applications include streamlined asset transfer, automated record-keeping, and secure fractional ownership of high-value assets.

Virtual/Augmented Reality:

These technologies can create immersive, interactive environments for client consultations, portfolio visualizations, and financial education.

Strategic Ways Forward

Here’s how wealth management firms can build future-focused digital platforms:

Focus on the Client Journey:

Map out the ideal customer experience, ensuring that every touchpoint delivers ease of use and meaningful value.

Prioritize Data Security and Transparency:

Handling sensitive financial information demands robust security protocols, ethical data usage, and clear communication to build trust.

Embrace an Agile Mindset: Be prepared to iterate and adapt platforms in response to changing technologies, investor preferences, and market conditions.

Find the Right Partner:

Work with a partner like Maveric Systems, which can deliver the specialized expertise needed to build and maintain a cutting-edge platform that instills client confidence.

Conclusion

The future of wealth management is undoubtedly digital. Platforms that successfully balance personalization, flexibility, and the seamless integration of new technologies will empower investors and advisors. By carefully considering these trends, wealth management firms can harness the power of digital solutions to attract new clients, improve satisfaction, and position themselves as leaders in a competitive and technology-driven landscape.

About Maveric Systems

Established in 2000, Maveric Systems is a niche, domain-led, BankTech specialist, transforming retail, corporate, and wealth management digital ecosystems. Our 2600+ specialists use proven solutions and frameworks to address formidable CXO challenges across regulatory compliance, customer experience, wealth management and CloudDevSecOps.

Our services and competencies across data, digital, core banking and quality engineering helps global and regional banking leaders as well as Fintechs solve next-gen business challenges through emerging technology. Our global presence spans across 3 continents with regional delivery capabilities in Amsterdam, Bengaluru, Chennai, Dallas, Dubai, London, New Jersey, Pune, Riyadh, Singapore and Warsaw. Our inherent banking domain expertise, a customer-intimacy-led delivery model, and differentiated talent with layered competency – deep domain and tech leadership, supported by a culture of ownership, energy, and commitment to customer success, make us the technology partner of choice for our customers.

View

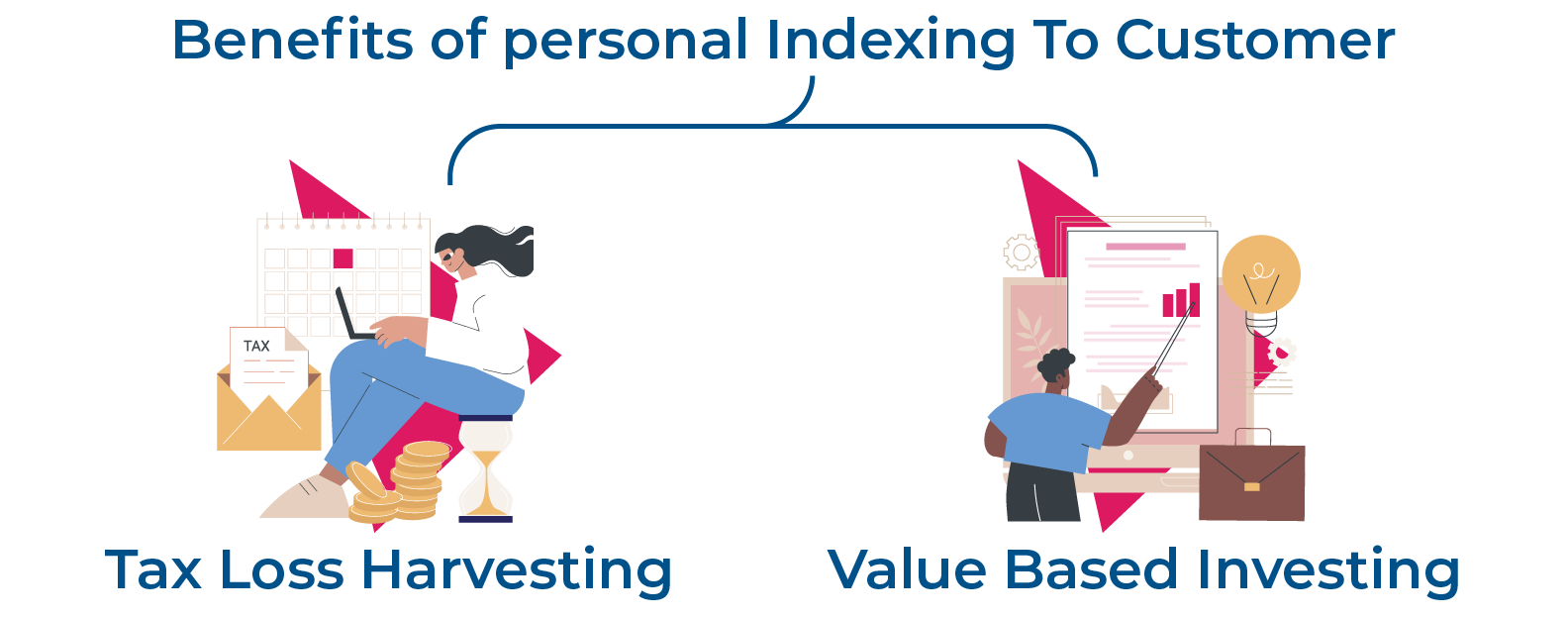

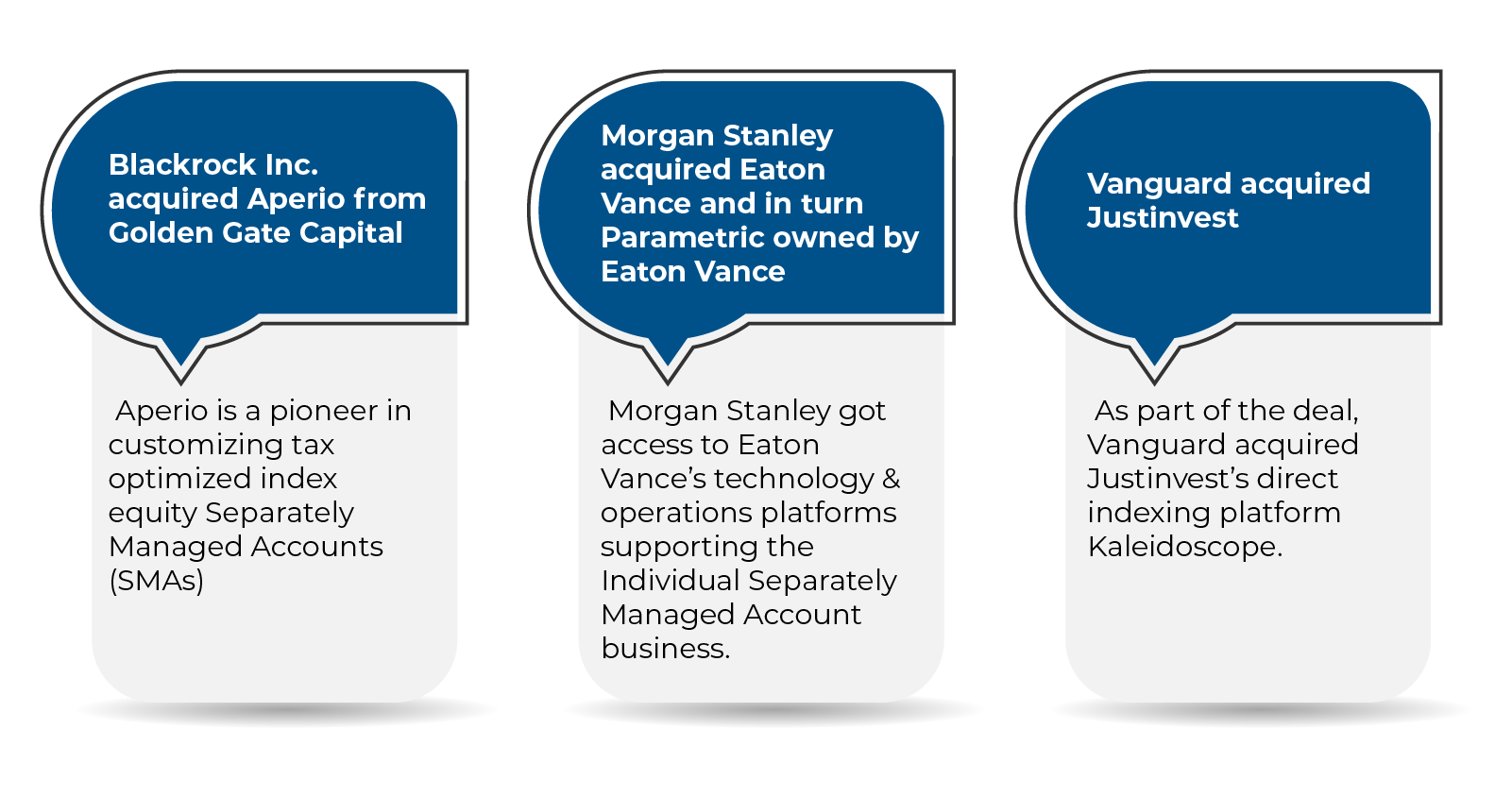

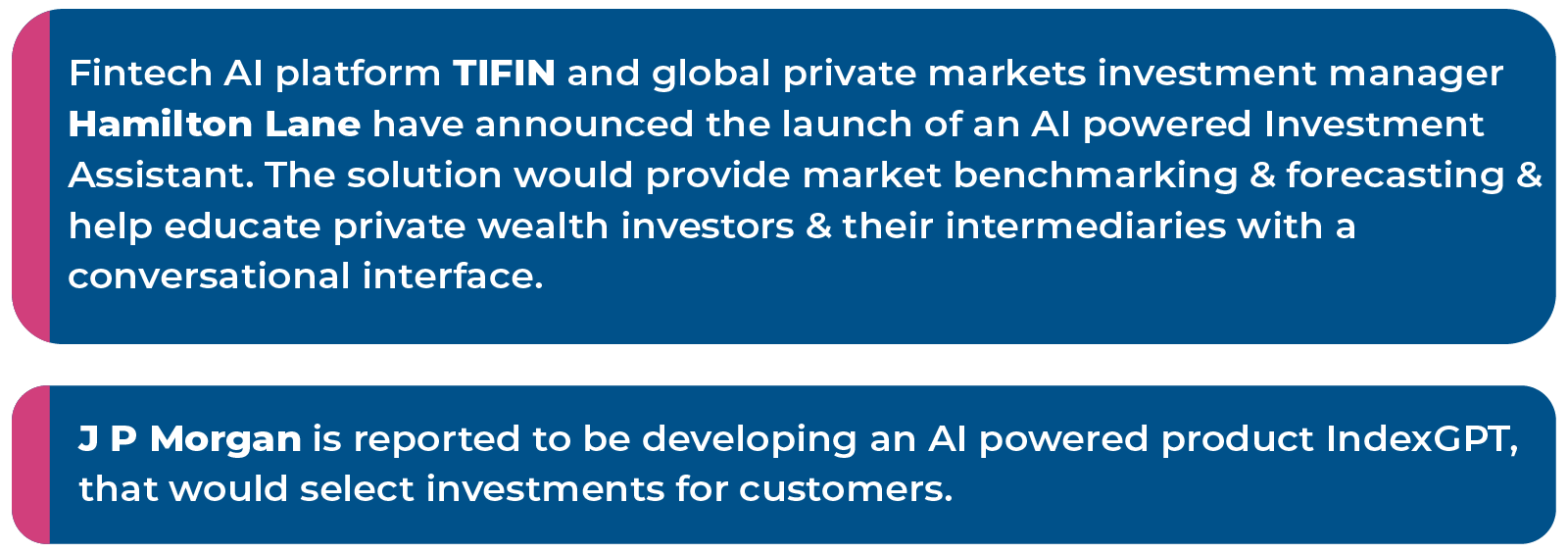

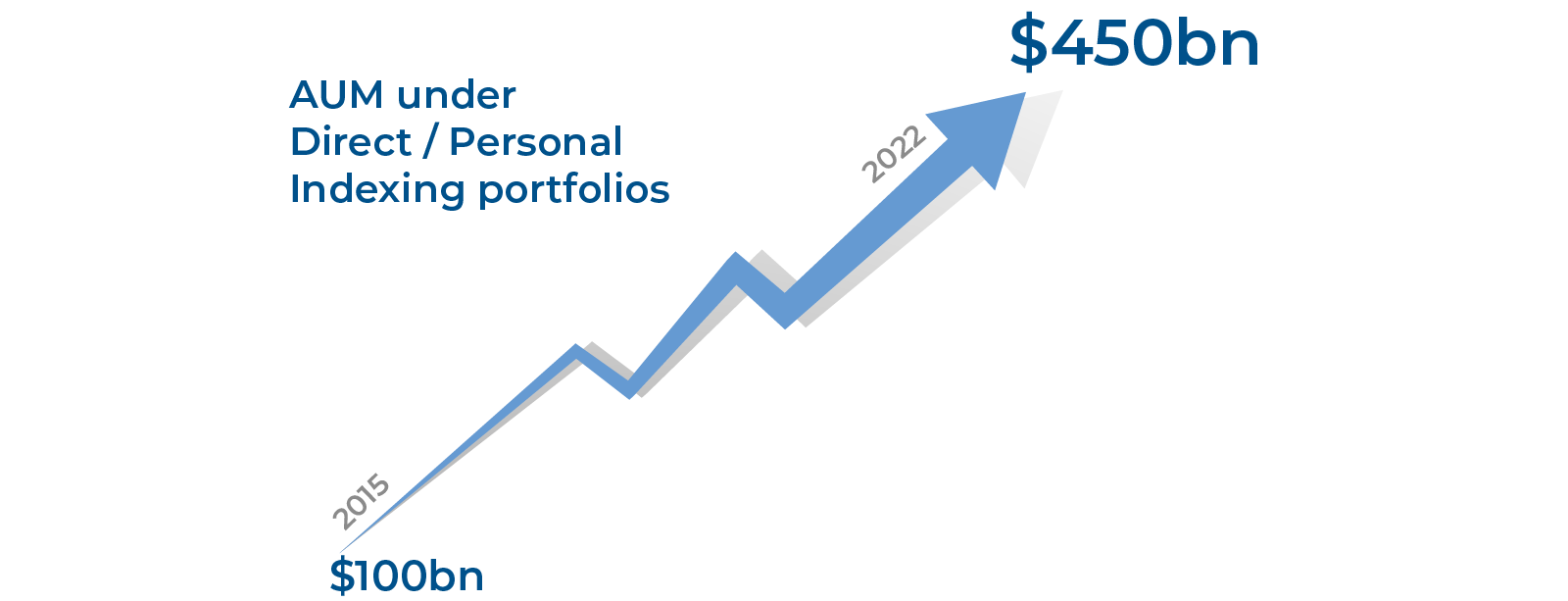

AUM under Direct / Personal Indexing portfolios is estimated to have grown more than four-fold from about US $ 100 billion in 2015 to about US $ 450 billion as at the end 2022 & is expected to be a key investment option for investors going ahead. The last few years have seen major players in the WM business like Morgan Stanley, Blackrock, J P Morgan Chase, Vanguard, Franklin Templeton, Charles Schwab, Fidelity etc. move into Direct / Personal Indexing space, reflecting the perception on future growth potential of this product.

AUM under Direct / Personal Indexing portfolios is estimated to have grown more than four-fold from about US $ 100 billion in 2015 to about US $ 450 billion as at the end 2022 & is expected to be a key investment option for investors going ahead. The last few years have seen major players in the WM business like Morgan Stanley, Blackrock, J P Morgan Chase, Vanguard, Franklin Templeton, Charles Schwab, Fidelity etc. move into Direct / Personal Indexing space, reflecting the perception on future growth potential of this product.