Decoding Global ESG Compliance: What’s next on the horizon for asset managers?

A Shifting ESG Regulatory Landscape

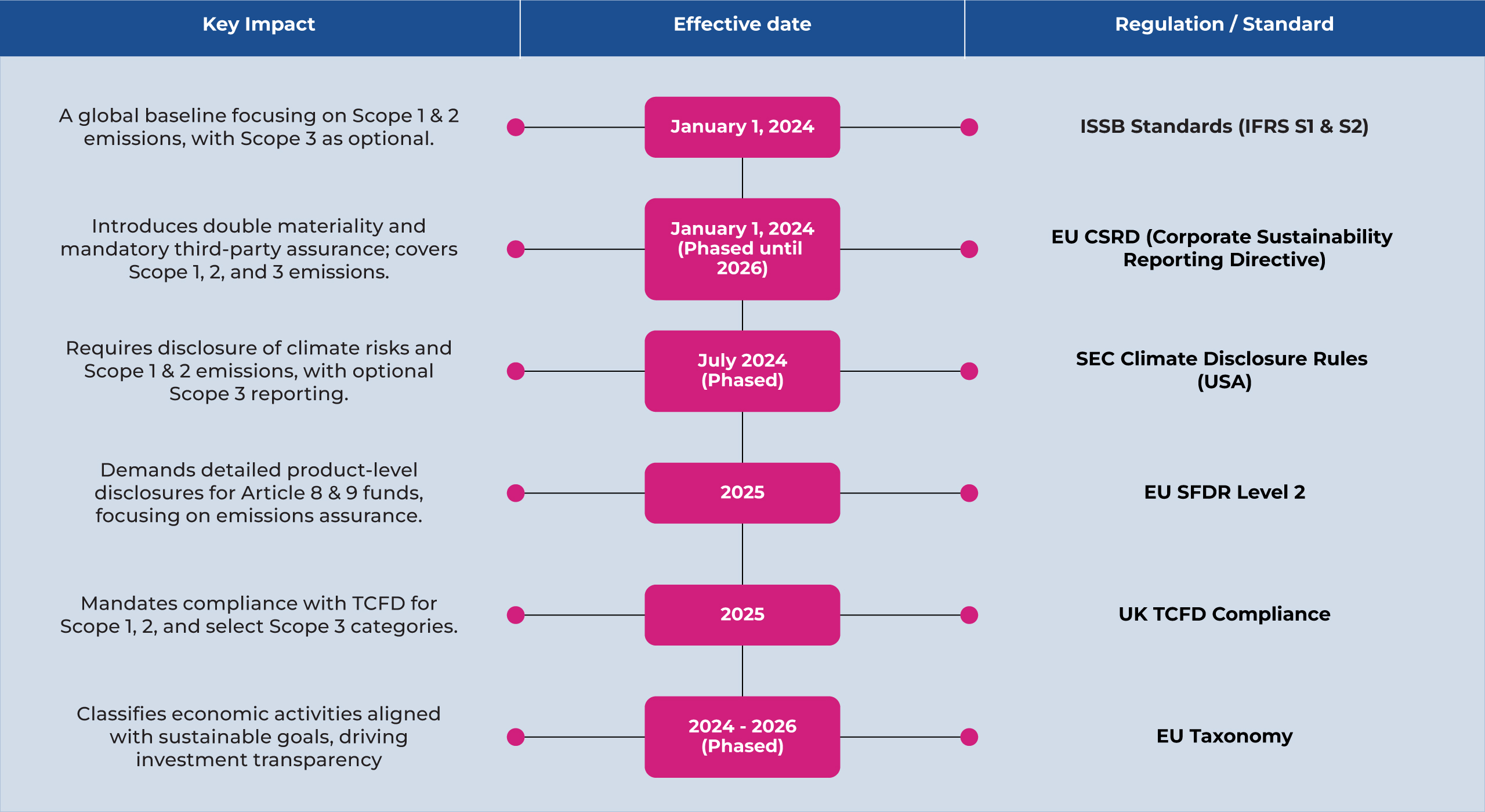

The ESG compliance journey has entered a pivotal phase, marked by the convergence of global and regional frameworks. With the International Sustainability Standards Board (ISSB) launching IFRS S1 and S2 standards in January 2024 and major regional regulations like the EU’s CSRD and SEC’s climate disclosure rules nearing implementation, the ESG landscape is rapidly transforming into an era of rigor and standardization.

This evolution isn’t just about meeting new requirements it reflects the growing integration of ESG into financial decision-making. Asset managers now face a reality where sustainability metrics are no longer optional add-ons but essential components of financial reporting.

Milestones Defining the ESG Regulatory Horizon

The following key regulatory deadlines are set to shape the strategies of asset managers worldwide:

While ISSB’s global standards aim to unify reporting practices, regional nuances such as the EU’s mandatory third-party assurance and double materiality principle add complexity. Asset managers must navigate these intricacies as jurisdictions implement staggered timelines while maintaining operational consistency.

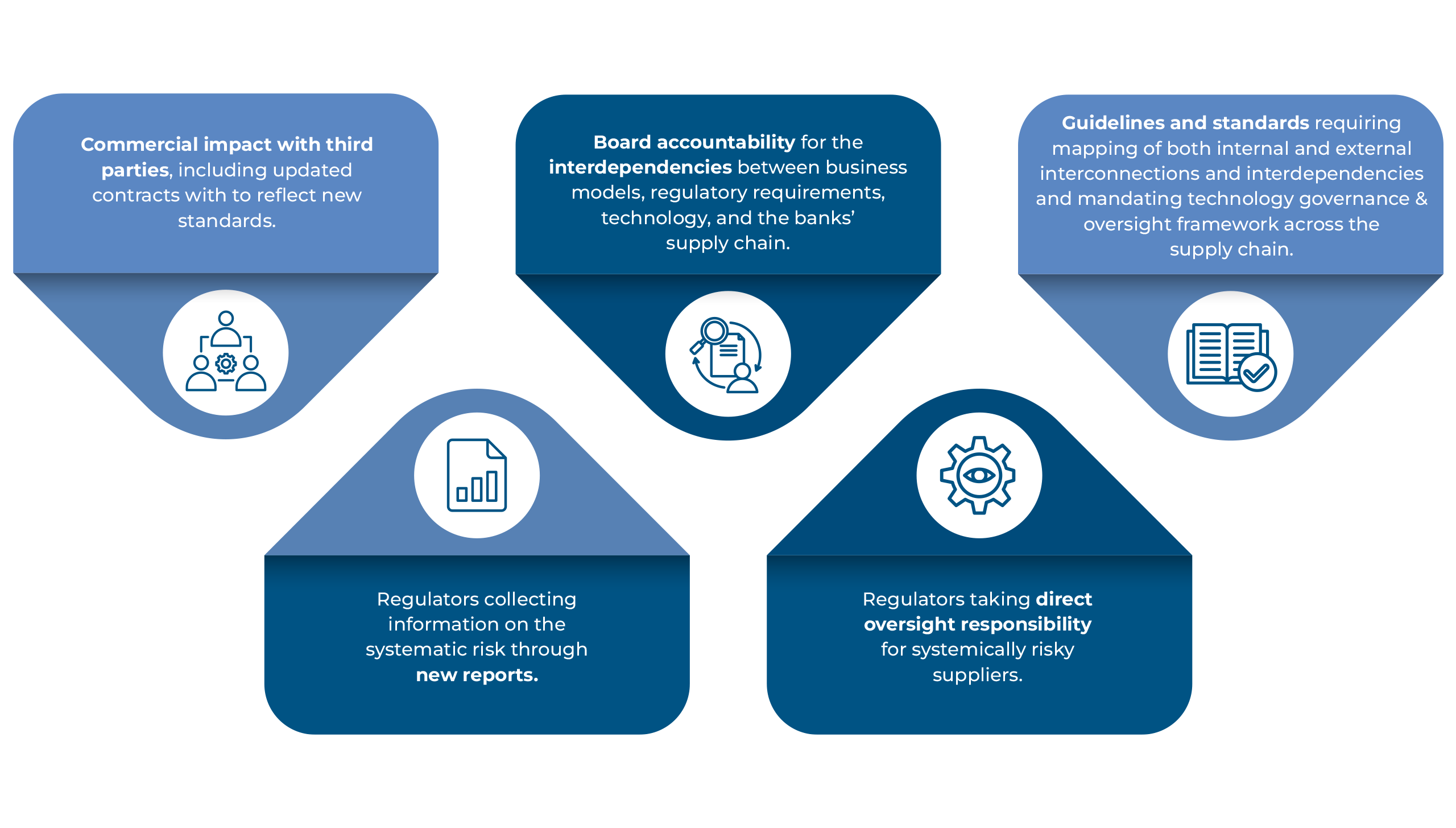

What This Means for Asset Managers Now?

As these regulations take effect, asset managers should anticipate three key developments:

these regulations take effect, asset managers should anticipate three key developments:

1.) Higher Reporting Complexity Across Jurisdictions

Region-specific requirements accompany the push for global alignment via ISSB standards. For instance, the EU’s CSRD emphasizes double materiality, while the SEC focuses narrowly on climate risk. This divergence will demand granular, tailored reporting across multiple regions and the balance of global consistency with regional customization.

2.) An Intensified Push for Data Quality and Assurance

Mandatory third-party assurance, particularly under the CSRD, signals a new era of accountability. Asset managers must ensure their ESG data is accurate and audit-ready, encompassing Scope 1, 2, and increasingly, Scope 3 emissions.

3.) Integration of ESG into Financial Frameworks

ESG data is evolving from standalone sustainability metrics into core financial components. ISSB’s standards and the EU’s directives underline the expectation that ESG should be as central to financial reporting as traditional financial metrics. Governance structures will also adapt, with ESG ownership increasingly shifting to CFOs for financial integration.

Looking forward – ESG has a new normal

As the compliance landscape continues to evolve, asset managers should anticipate the following shifts:

1.) Heightened Supply Chain Accountability:

The focus on Scope 3 emissions and supplier data is intensifying, with regulators and investors pushing for greater transparency across the value chain.

This means asset managers must conduct detailed lifecycle assessments and measure and assure indirect emissions numbers across their supplier networks. Enhanced traceability and data integration will be key to staying ahead.

2.) Investor Demand for Real-Time ESG Insights:

Investors’ expectations will continue to be more demanding than regulators’ and will keep driving the transformation. Investors today are expecting more dynamic, real-time ESG dashboards that provide ongoing visibility into portfolio performance and specific asset-level metrics. This shift toward continuous disclosure requires asset managers to integrate advanced analytics and reporting tools that can deliver timely insights and retain investor trust.

3.) Stricter Enforcement and Elevated Reputational Risks:

The consequences of non-compliance are becoming more severe, with recent cases resulting in hefty penalties, fund delistings, and significant reputational damage. Regulatory scrutiny will only deepen, so robust ESG governance frameworks and data assurance must be prioritized to avoid legal repercussions.

Conclusion: ESG as a Driver of Long term shareholder value

The evolving ESG landscape is reshaping how asset managers operate, pushing ESG from a regulatory requirement to a driver of strategic differentiation. Firms delivering transparent and credible ESG disclosures are strengthening investor trust and attracting capital in a market increasingly driven by sustainability priorities.

As regulations tighten and enforcement strengthens, asset managers must navigate increasing scrutiny on Scope 3 emissions, supply chain accountability, and real-time ESG performance insights. Recent penalties and fund delistings for non-compliance clearly signal that the focus on data accuracy, assurance, and transparency will only grow.

Meeting these expectations will require a rethink of strategies within firms and across their ecosystems. Asset managers must enhance internal processes, including the technology adoption, collaborate more deeply with suppliers and investors, and engage with regulators on an ongoing basis.

These strategies and more are explored in detail in our report – “Mastering ESG Data: Practical CFO and CTO RegTech Strategies – Securing a regulatory and Market Edge in 2025”

Key takeaways include:

- Navigating the regulatory mosaic with technology and data-driven strategies.

- Integrating ESG into financial reporting frameworks for lasting value.

- Building governance models that align with evolving investor expectations.

To get more updates, subscribe to our Monthly Newsletter

View

The maturity profile of NFR Risk management usually differs significantly between

The maturity profile of NFR Risk management usually differs significantly between