Regulatory Compliance – The US Impact

Federal banking authorities are monitoring how the banking industry is changing. On the one hand, banking authorities are utilizing their current supervisory authority to safeguard their operations. On the other, banks are strongly discouraged from dealing with cryptocurrency assets due to state, federal, and international regulatory activities.

Expanding data accessibility and enhancing data quality are top concerns. To begin with, the subject of BFSI regulatory compliance (program mandate and components) is a complex one.

As significant questions face FIs in 2023 on how regulatory frameworks should be extended to counter consumer risks, a vital question comes to the fore. How must banking overseers raise their priorities to become more data-dependent?

The perils for not doing so are immediate and well-known.

Consider this: RBI (India’s Central Bank) imposed a penalty of INR 3.06 Crores on Amazon Pay Services for non-compliance with KYC and prepaid instruments.

Regulatory Compliance – The US Impact

Section 1071 of the Dodd-Frank Act – New Rules for Small Business Data Collection

The section amends the Equal Credit Opportunity Act (ECOA) that requires FIs to aggregate, maintain and submit data to CPFB (Consumer Financial Protection Bureau). Most earmarked businesses (minority-owned, women-owned) with at least 25 small credit transactions in the last 24 months are to comply with business data requirements before March 2023.

Adverse Impact on Cryptocurrency Sector

Due to increased caution brought on by the industry's instability, Crypto businesses face an uphill journey to obtain institutional funding. The plummeting retail investors' interest in cryptocurrency adds to the substantial drop in Venture Capital. Consider the panic, as a report estimates that $540Mn was money-laundered (Crypto cash since 2020) using a service called RenBridge.

Impact of Durbin Amendment on Banking-as-a-service

The Durbin Amendment does not apply to banks with assets under $10 billion, and these institutions are permitted to impose higher interchange fees for processing debit card transactions. The law impacts smaller banks' tactics that support debit card systems offered by Fintechs, where the partners often split interchange revenue. There is a conflict for smaller banks in BaaS between seeking growth and reaping the rewards of staying under the $10 billion asset threshold.

Will 2023 see a long-term shift in debit programs?

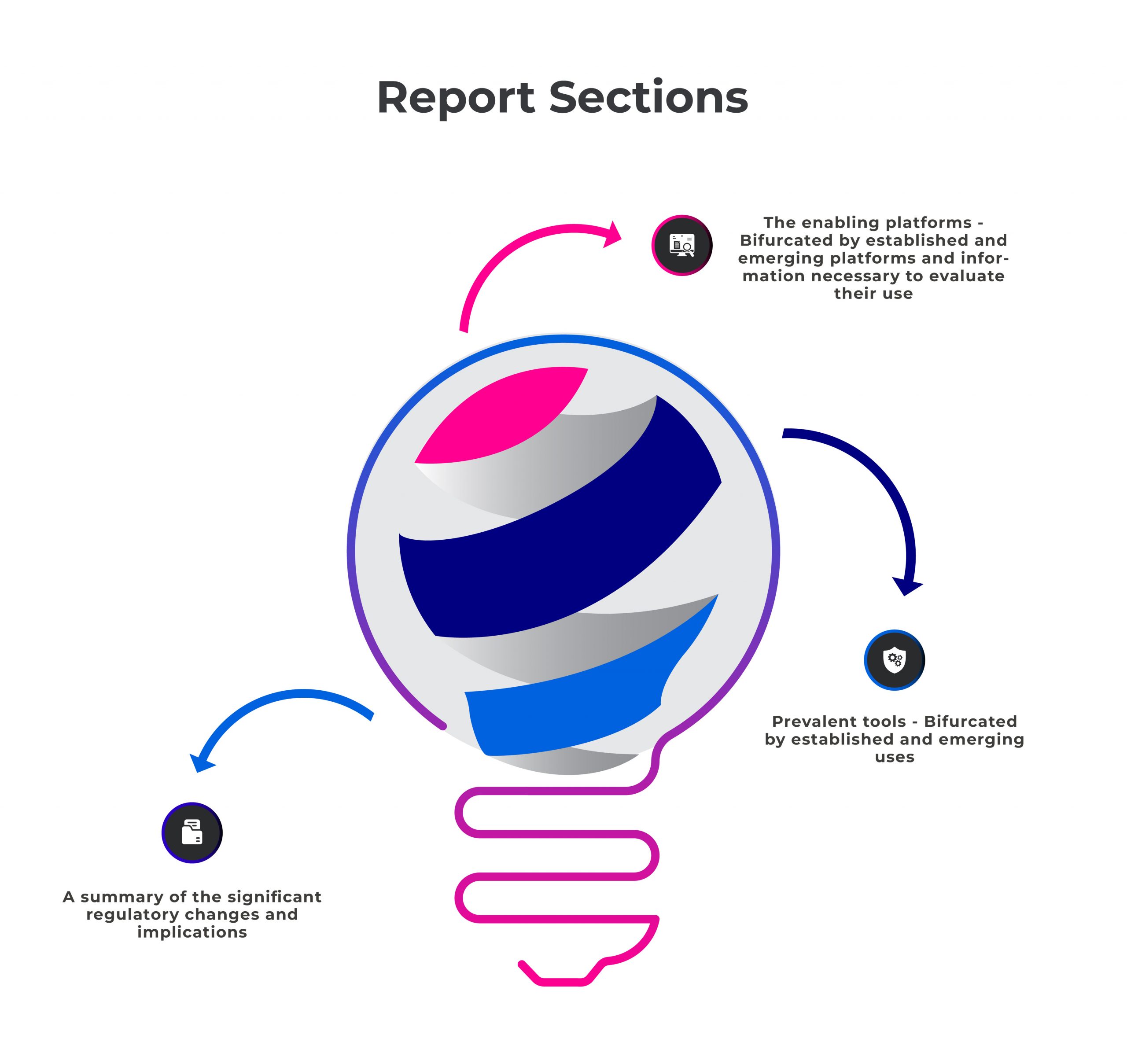

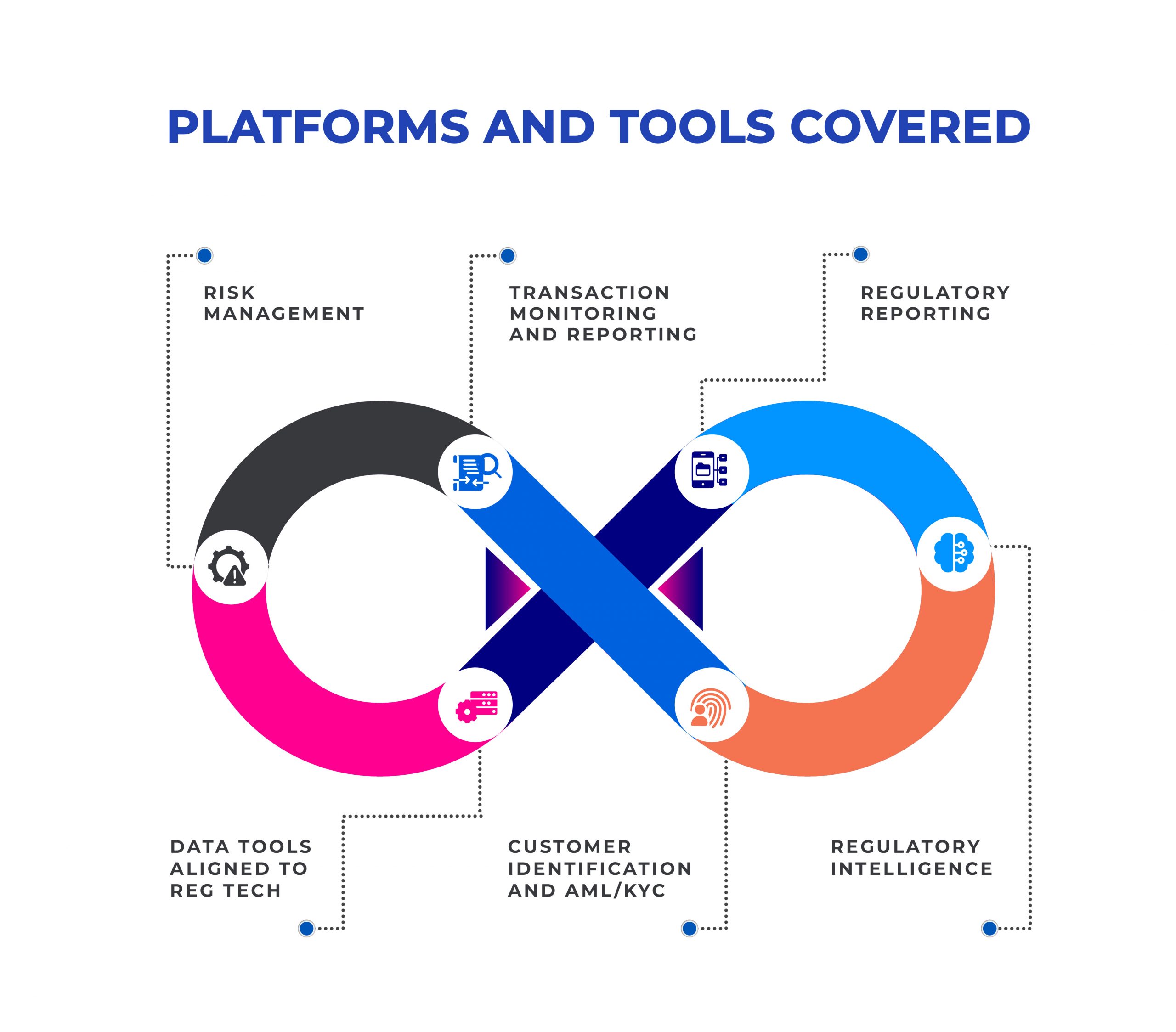

A Sneak Peek - Maveric’s Comprehensive RegTech Study

As banks increasingly rely on digital assets for greater oversight and clarity in the regulatory fragmentation geopolitical setup, Maveric’s report empowers C-Suite with a powerful tool to navigate a climate focused on economic recovery and customer impact.

The 2023 Maveric RegTech report provides banking leaders with a comprehensive view of significant regulatory changes across regions, platforms, and tools

The Way Forward

Undoubtedly, the winning combination for BFSI regulatory compliance outlook is to balance innovation with consumer protection. However, the financial services sector is facing difficult operating conditions as a result of a complicated mix of factors including high inflation, erratic interest rates, interruptions in the supply chain, and weakening economies. In light of this, boards and executive teams ought to ask- what measures are being taken to support consumers and maintain resilience in the face of impending economic difficulties. The way BFSI entities respond to that question will be influenced by their solid understanding of the constantly changing regulatory environment.