While significant strides in recent years have helped streamline regulatory reporting, the regulatory burden for banks has increased at an unprecedented rate.

For CFOs and CROs, one challenge in this maze of ever-evolving regulatory compliance is to keep costs in check. Shrinking margins mean dwindling resources (and budgets) are available to combat the growing complexity and granularity needed for regulatory reporting.

The problem increases for FIs that operate in more than a single regulatory jurisdiction. The question for legacy banks is how to leverage automation to deliver undiscovered value.

This blog article rounds up the changing nature of regulatory reporting, the need for RegTech, and the leading intervening technologies in this space.

It would help by tracing today’s business landscape that demands additional regulatory risk and compliance reporting on banks.

FIs challenges in Regulatory Reporting.

- Constantly evolving financial regulations by governments and other bodies (especially in the aftermath of the pandemic)

- A significant change in the macro-economic climate (triggered by armed conflicts and other geo-political developments)

- Rising overhead costs on production and implementing solutions for regulatory compliance.

- The steep fines and penalties for regulatory violations and non-compliance(s)

- Burdensome legacy systems that resist integration with modern automation and digitization solutions.

- Fragmentary organizational culture often results in non-standardized approaches and process inefficiencies.

- The listed problem statements call for a radical approach that favors open architectures and hyper-precision.

But before we get down to the technology enablers that hold promise, let us understand how the situation is not about costs alone.

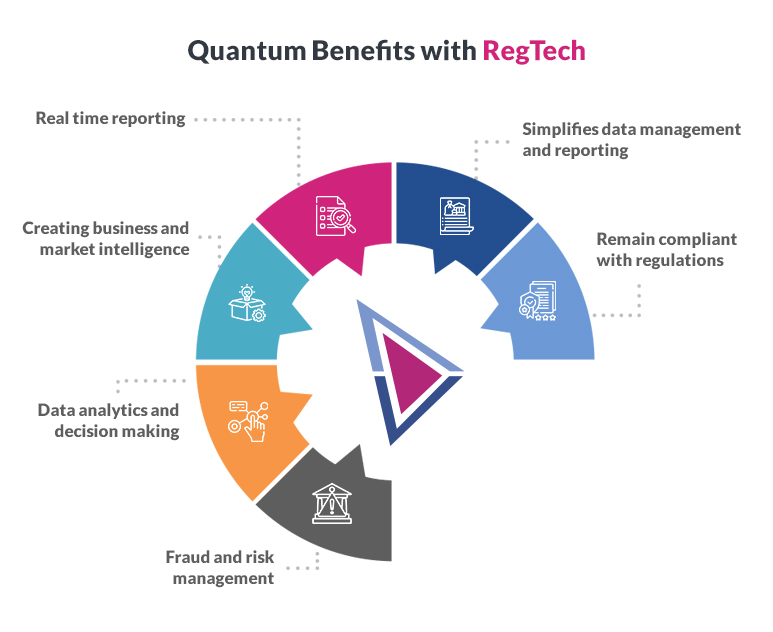

RegTech is more than costs and efficiency.

Post the pandemic, regulatory reporting in banking and securities has taken an additional responsibility – adding value to the business through Marketing Intelligence (MI) insights and offering customer-centric insights.

Unsurprisingly, compliance operations use more RegTech to gain greater visibility into future regulatory demands. Also becoming mainstream is the emerging tech areas of Distributed ledger technology, Advanced analytics, Robotic Process Automation (RPA), and Cognitive computing.

In all of this, the goal for leading FIs is common: Implement strategic end-to-end reporting solutions – from extracting input data to performing regulatory computations, generating regulatory returns, and producing MI for analysis wired into business strategy.

Having a strategy is one thing, but gaining a deeper understanding of the tech enablers is another. Next, we look at how a successful RegTech approach leverages (or experiments with) use cases and scales faster with reduced costs and risks.

Having a strategy is one thing, but gaining a deeper understanding of the tech enablers is another. Next, we look at how a successful RegTech approach leverages (or experiments with) use cases and scales faster with reduced costs and risks.

Developing Robust FinTech solutions for Automating Regulatory Reporting

Cloud Computing: When central servers connect to a network of remote computers (as opposed to maintaining infrastructure in-house), the FIs make significant cost savings, amp up their agility, and elevate adaptability to integrate with a slew of (established and emerging) technologies that we explore next.

Blockchain Technology. Using ‘smart contracts and shared data, Blockchain technology eliminates costly intermediaries in processing and calculates contract cash flows and revenues in real-time. The use cases for this emergent tech are centered on reducing the time (and resources) spent in validating transactions.

Robotic Process Automation. Consider the routine and repetitive tasks like reconciliations, monthly closing, and preparation of automated financial statements to achieve efficiency, and cost savings and free up the use of human expertise for complex activities.

Advanced Analytics. From intelligent dashboards that report performance management to forecasts of business metrics related to budgeting, treasury forecasts, cash flows, and commodity prices, Predictive and BI tools help FIs predict future outcomes and organize data into trends and patterns, often through intelligent visualization.

OCR and ML. Finally, the technology that has been in use for some years now in regulatory reporting is optical character recognition and the associated Machine Learning engines. These tools accelerate data analysis and increase output accuracy, the vital levers to cost optimization. Additionally, monitoring thousands of transactions in real-time brings handsome returns to the bank’s tech investment.

Conclusion

In sum, before other vital Enterprise pieces of Regulatory risk and compliance reporting can be worked upon (say, an integrated corporate reporting system), a few questions to gauge the internal demand for RegTech must be spelled out.

- What percentage of time does the finance team spend on repetitive, routine, and unproductive tasks?

- What is the degree of complexity and changes in recurring tasks – monthly recons and closing report?

- Does the present regulatory reporting involve significant manual hand-overs and data inputs?

- In terms of accuracy, and error rates, are the metrics showing an improvement or not?

- What is the quality of data visualization for leadership decision-making?

Answering these questions (and identifying the improvement areas) is a good starting point for banks to formalize their RegTech mandates.