1. The ‘Smart’ Spirals

In 2019, India had over 560 million internet users across the country. After China (at 854 Million users) India ranks as the second largest online market worldwide. This could however, be misread as a flattering statistic. Because with 40.1% Internet penetration, India languishes far behind many of its South East Asian neighbours (South Korea – 95.1%, Japan – 93.5%, Malaysia – 80.1%, China – 58.4%, Bangladesh- 56.2%)

Compounding the country’s low internet penetration, Indian banks are confronted with poor penetration of smart phones as computing devices. In 2018, there were 290 Million smartphones being used in rural India. World bank developmental data categorises 860 Million as ‘Rural India’. Do the math.

Change however is not far behind. Spurred by the government’s Digital India campaign focussed on levelling this digital divide; higher availability of bandwidth, cheaper data plans and competitive pricing for smart phones; the subscriber base for digital transactions can only grow in 2020 and beyond.

In fact, the current numerical scenarios described above, do not deter Indian banks from augmenting their digital capabilities and offerings. Digitizing processes and reimagining digital technology is today’s topmost strategic banking agenda. Done well, these radical process-changes translate into cost reductions, higher employee productivity and stronger customer engagements.

All said, Smart phones will spiral Smarter banking. And Soon.

2. Dismantle to Evolve for the new ‘DISC’ consumer

Customers that are digitally native, intelligent, social and connected (DISC) seek engaging service designs that match the coolest Internet companies. This rising customer demand of ‘convenience without additional cost’ brings legacy banks under a constant subliminal threat. Not to be cowed down either, most conventional banks look to leverage their pre-existing customer data and trust. In addition to the process digitizing approach spoken earlier, traditional players incubate new ‘all – digital bank’ to stave off digital disruptors making serious dents to their market positions. Abundance of software talent in this country makes this ‘dismantling-for-evolution’ proposition easier.

3. Brick and Click; Not an ‘either-or’

Most of today’s digitally savvy customers check account balances on phones but want to speak for say enhancing their credit card limits and yet like to visit a physical branch for discussing home loan options. Different horses for different courses.

New age banking mindsets get this dynamic. They view the present reality as a persistent challenge and a creative opportunity. The situation is not an ‘either/or’ but, an ‘AND.

Unsurprisingly enough, the proliferation of digital banking technology has not diminished the number of (or significance that) clients place on transacting inside an actual bank.

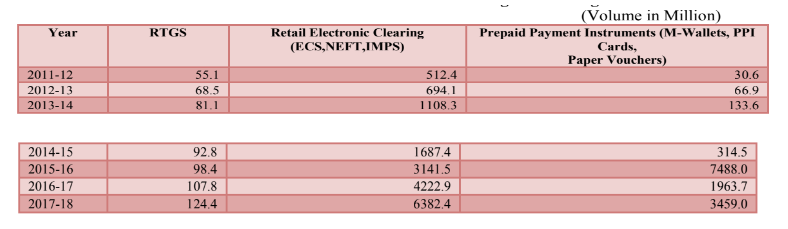

In fact, per RBI data tracking data (below), the volume of transactions in digital banking throws up interesting trends: Customers visiting branches for activities continues to be on the higher side but for higher amounts. At the same time, small value transactions continue to flourish through digital wallets, internet banking etc.

Searching for ‘that’ elusive customer experience sweet-spot often guides these banks to fine-tune their customer loyalty strategies.

As illustrated by a Gartner study, another element at the core of Brick Vs Click debate are ‘chat bots’. By end 2020, it is estimated customers will manage 85% of their relationships with banks without directly interacting with a human (another study points out that chat bots save up to $0.70 per interaction).

The con of the argument however is that chat bots (yet) do not offer culturally nuanced and unique service touch that say, a rural banking customer is habituated at his retail branch counter. These gaps often raise unanswered privacy concerns and creates a wariness against digital transactions. That debate will be decided by how quickly banks can consciously contextualise their digital solutions.

4. The ‘why’ before the ‘what’

The sheer glut of digital transformation initiatives in the Indian banking industry (pegged at $24.5 Billion in 2018) does invite confusion – which digital transformation projects are ‘urgent’ and which are ‘important’? Decisive banks are the ones that separate quantum innovation from the incremental transformation efforts. Beyond experimenting for product costs and features, the focal point today is on ‘customer experience’. Competitive edge comes from designing superior customer experiences that drives higher adoption and eventually secures brand recognition and digital loyalty.

And often, the question at heart of such transformation journeys explores not the ‘how’ or ‘what’ but why?

5. Home Alone, Home Secure

Indian cyber security market – $ 2 Billion, 2019 – is estimated to grow to $3 Billion by 2022; a compound growth rate of 15.6% that is predicted at one and half times the global rate.

One of the largest challenges for digital banking transformation initiatives has and will remain the ability to solve security issues at scale.

Today’s banking environments heavily draw upon collaborative ecosystems – meaning, hundreds and thousands of networked computers and other connected devices. Add Social, Cloud, Mobile and other channels into the continuously evolving mix and we are talking about managing financial vulnerabilities on a never-before seen scale.

In fact, today it is the digital banking transformation that powers the Cyber Security Industry to continually create stronger security and compliance solutions capable to scale on demand. No matter how the cyber security and banking technologies commingle tomorrow, the number of digital transactions will be influenced by how secure (and how alone) we feel in our ‘digital homes’ today.

While more can be discussed about challenges and opportunities applicable to digital era banking, but banks – that prepare to seize the globe’s second largest digital market (yet maturing) stabilized by the current popular government and a stable regulator invested in capitalizing the global digital economy – will eventually succeed.

Disclaimer: The views expressed in the article above are those of the authors’ and do not necessarily represent or reflect the views of this publishing house. Unless otherwise noted, the author is writing in his/her personal capacity. They are not intended and should not be thought to represent official ideas, attitudes, or policies of any agency or institution.

This was originally published on Business World website and is being reproduced here.