The second payment services directive (PSD2) joins the global trend in banking regulation and focuses on innovation, open-data sharing, and improvement in security. As banks across Europe adopt open banking, we take a closer look at its impact on consumer behavior and the challenges before traditional banking systems.

The move to open banking has laid the impetus on banks to providing customer services that are available on-the-go. Banks have to enter the tech-race where services and products are user-friendly, secure and bug-free. HSBC responded to the new open banking directive by launching its own app, Connected Money, which enables users to access accounts from 21 different banks in one place – setting the precedence for other banks to follow.

|

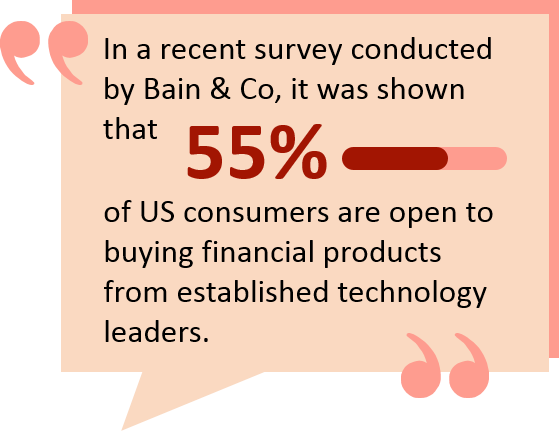

But still, when it comes to customer experience, traditional banks are hit by FinTech companies that excel in offering streamlined customer experience. Banks cannot ignore their low Net Promoter Scores (NPS). The NPS answers the fundamental question of “On a scale from 0 to 10, how likely are you to recommend this company to your friends and family?” Tech companies are known to score higher on NPS and this hurts banks when non-banks start offering similar services to banks. What does this mean for banks? If a tech company like Google or Amazon is to offer a credit card or loan, their existing users would opt for the new service. |

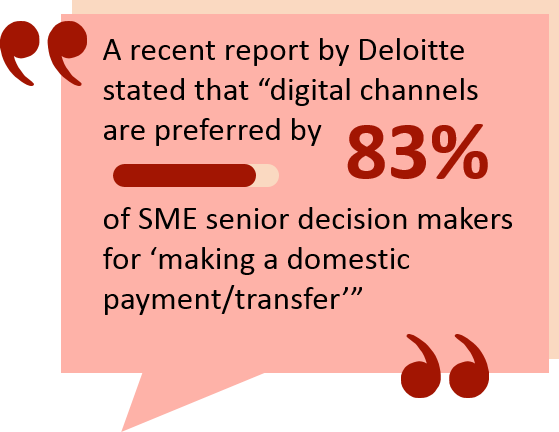

| If tech companies weren’t enough, banks are also threatened by the rise of online banks – those that replace the traditional brick and mortar enterprises. Companies like Alibaba, Baidu and Tencent have built an online banking infrastructure that caters to SMEs and businesses. Banks have to differentiate themselves from new entrants and incumbents by providing greater customer experience and pricing transparency. |  |

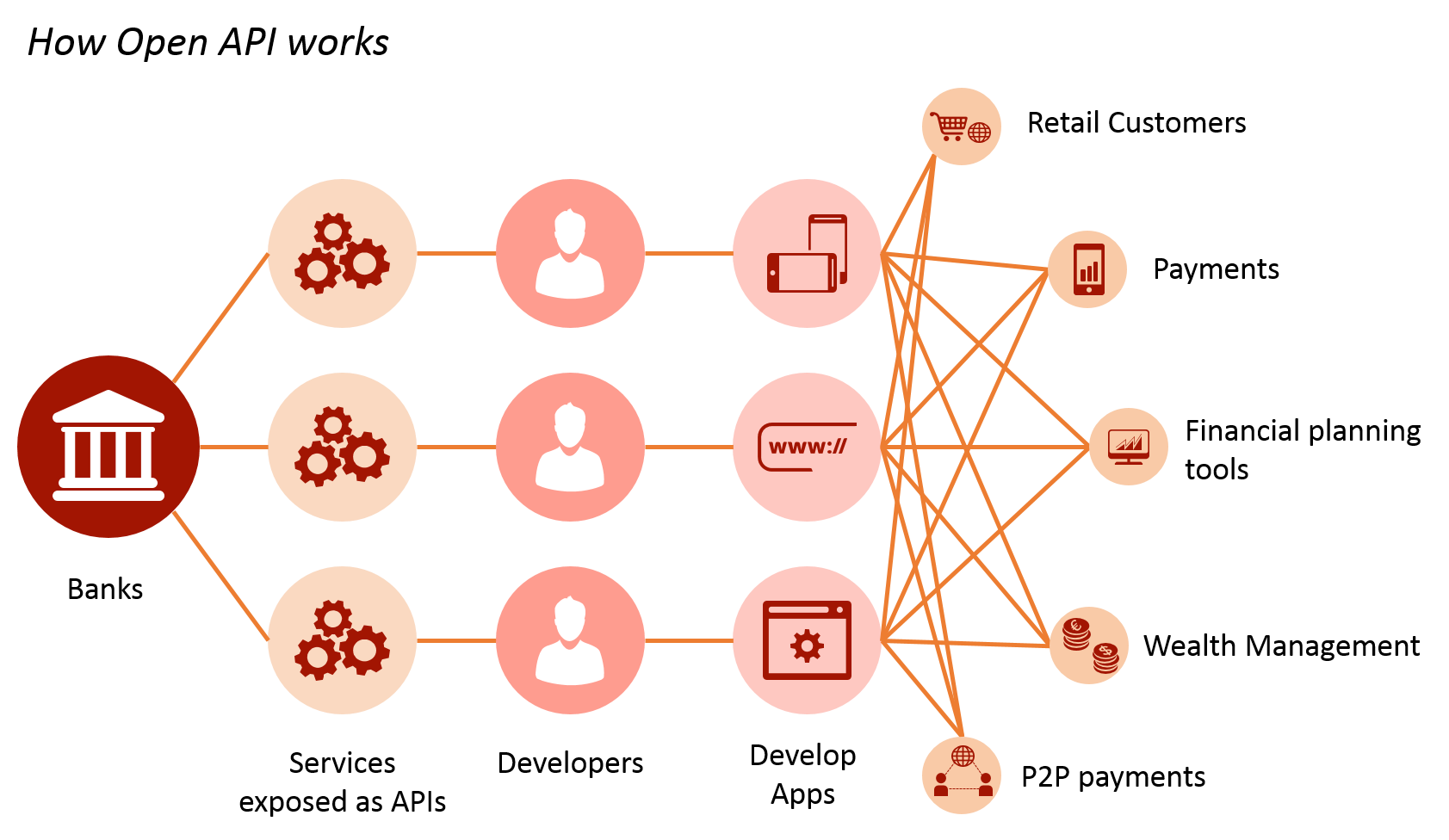

As a direct consequence of such innovation, banks have opened up their banking operations to various industries. Such an open-source approach is now heralding a sea of change in the finance industry through Open APIs, revolutionizing products and services quicker than ever before. Open APIs enable FinTech companies to access bank data and functionality, bringing a great change in the digital banking ecosystem.

This revolution has been fruitful for the banks who embraced Open APIs and Open architecture in building their services. However, by opening up their APIs, banks face several issues, especially in terms of security, as nothing should possibly go wrong when banks open their APIs up.

Digital developers are becoming faster at building integrations with banks using Open APIs, but they lack knowledge on business and regulatory compliance. On the other hand, banks still need to take full accountability of all the security and compliance issues that are likely to arise.

Furthermore, the PSD2 has opened up the banking industry for new entrants to bank-held customer account data to Account Information Service Providers (AISPs). The current banking operating models constitute consumer interfaces owned by the bank. The open banking initiative can change the scenario with companies essentially taking over the interface. For example: Apple has already launched its Apple Pay services across Europe for digital payments. The service caters to in-store payments via smartphones and contactless payments. Amazon is also in the payments services where it provides loans and credit cards. With the introduction of their voice-enabled speakers, Echo, Amazon has enabled ease of everyday banking. Users can say “Alexa, pay my electricity bill” and the process would be over in a jiffy.

Even though big banks don’t face any imminent danger in losing customers, not adopting technology or creating strategic alliances could mean the loss of business. Currently, traditional financial organizations rely on FinTech for their technological needs – from chatbots to cloud computing. What keeps FinTechs from taking over the finance industry is the strong regulatory compliance framework. The entry of tech giants into core banking services would rattle the banking industry and effectively change the financial landscape. If banks don’t up their digital game they will get eaten up by well-established tech companies. The future may seem uncertain for now, but one thing is sure that open banking is here to stay. It would be interesting to see who wins the banking battle between banks, FinTechs and non-banking companies.