What does the current landscape look like for Retail Banking?

Firstly, the post-pandemic retail banking industry is moving out of a climate of muted financial performance. Secondly, with common enablers of open hybrid or multi-cloud solutions, banks embrace Data & AI tech to combat security and fraud risks.

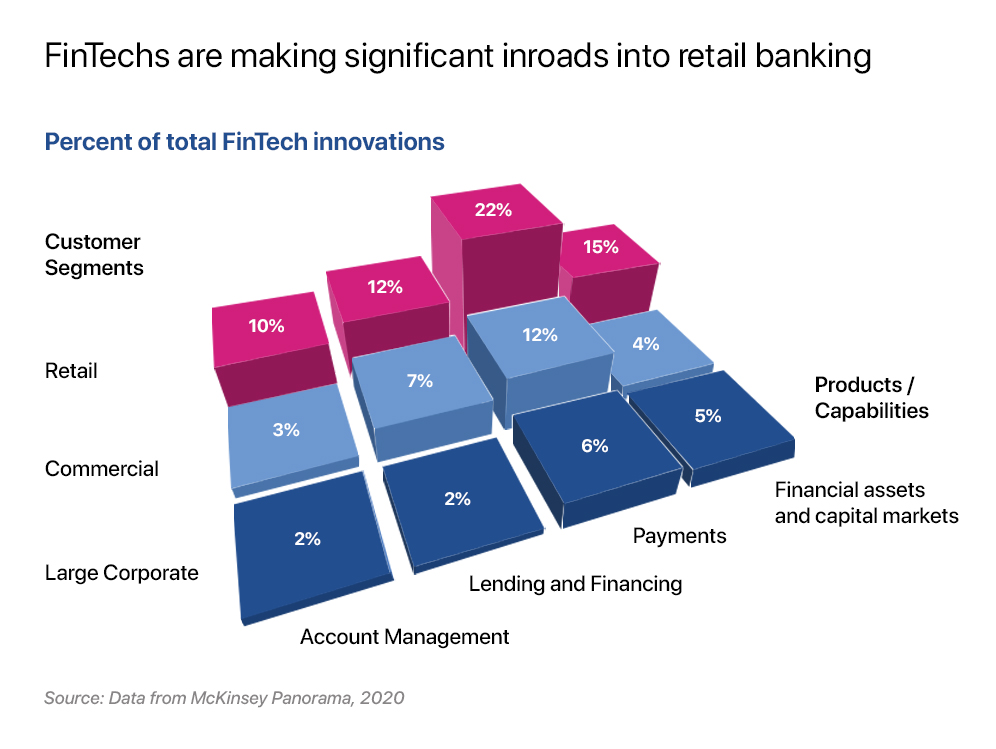

So far, breaking away from the pack signifies the next normal for the retail banking industry. And why is that? Now with most COVID protocols behind us, the urgency for retail FIs to accelerate digital transformation is driven by the sustained competition coming from Fintechs (Refer to infographic)

Here is a roundup of the Top Four Insights for the Retail Banking Industry

Tomorrow’s Competitive Advantage will come from Customization.

As part of their digital transformation journeys, top retail banks must invest significantly in high-tech analytics to improve Customization. Micro-segmentation of consumers through customer relationship management (CRM) data (such as socio-demographics, client strengths and product usage, and recent transactions) and digital behavior will be the integral aspects of digitally- agile sales programs.

From adopting various processes – increasing sub-segments in customer profiling, working through test-and-learn strategies, personalizing communications with each customer (altering the email subject line, tweaking the language tone, optimizing communications for the time of the day), and constructing a multichannel contact tree are mechanisms that will boost customer centricity.

Retail Banking’s next battleground is Digital Sales.

Successful FIs have figured out how to address more, and higher-value client needs digitally. Even though the global crisis slowed monthly unit sales across channels in many markets, it did accelerate the redistribution of the sales mix as channels recovered at different rates.

Leading retail banks are accomplishing top-tier digital sales by continuously developing the digital customer experience and optimizing it across the customer journey.

Here are a few optimization examples from CX journeys

- Deploying and testing new features

- Using customer relationship management (CRM) software to make preapproved offers

- Shortening the application and approval process by pre-filling information

- Employing digital signatures to speed up the fulfillment process.

To quickly digitize multiple priority customer journeys, more and more banks are establishing a digital “factory” – bringing together hundreds of staff to build new, best-in-class digital experiences and products.

Upping the ante in Retail Banking through Digital Services

Banks have helped clients feel secure using digital and telephone banking during COVID-19. They have therefore enabled the next generation of digital services. As of May 2020, people have shown great satisfaction with digital channels, and anywhere from 60% to 85% of consumers in Western Europe, including those aged 65 and up, prefer to utilize digital for everyday transactions.

Successful banking businesses have reported that increasing their mobile strategies has resulted in five times the engagement. Almost a third of all digital purchases today come from the mobile app. Several factors, including more exciting app features, frictionless user experience, and creative capabilities, are all responsible for this surge.

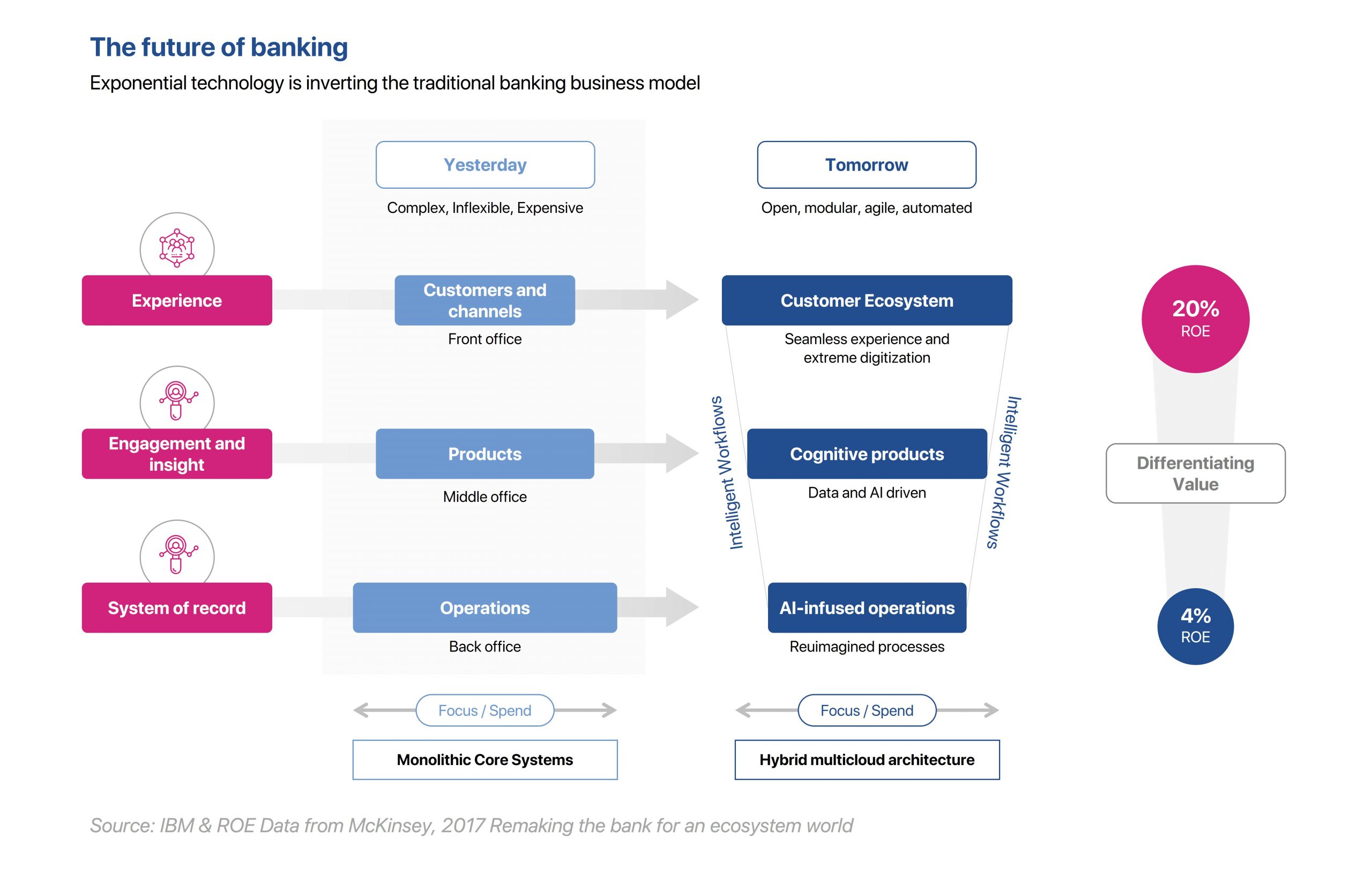

The infographic below traces the shifts in banking business models. The rate at which it evolves across various geographics is different and determined by regional influences.

Amping up the “human” in virtual channels.

To improve customer service through the call funnel, leading retail banks invest in cutting-edge Data & Analytics technology. Using chatbots to keep digital customers has helped reduce customer service calls. Conversational and adaptive IVRs today draw on a wealth of interaction history to deliver targeted answers to individual users’ questions while freeing up agents’ time to focus on more complex cases. When calls get through to agents, innovative tools like voice-to-text transcription create data sets that can be mined for insights using text analytics, sentiment analysis, and natural language processing.

It’s no secret that several financial institutions have dabbled in remote advice models like branch-to-hub or hub-to-home banking. Through screen sharing, remote advisory can mimic the benefits of face-to-face meetings and digital capabilities, such as identification for quick fulfillment and a more gratifying experience. Ultimately, these features link clients with the most qualified specialists for their inquiries, allowing for more productive dialogues.

Conclusion

In sum, there are two crucial questions retail banks must address before drawing up their next growth strategy:

- How likely are banks and other FIs to see digital channels overtaking physical locations as the primary means of selling their products and services?

- After the pandemic, do banks expect a reversion in customer behavior to pre-outbreak norms?

Answers to these two questions will prove crucial in the final analysis.

In 2022 and the following year, expect to see more retail banks reevaluating their revenue drivers, searching for new product launch prospects, and reorienting their offerings towards an advisory and insurance slant.

For retail banks, with escalating revenue and growth pressures, it is advisable to employ advanced analytics that identifies relevant growth niches so that optimized digital sales journeys and innovative marketing approaches can fuel growth.