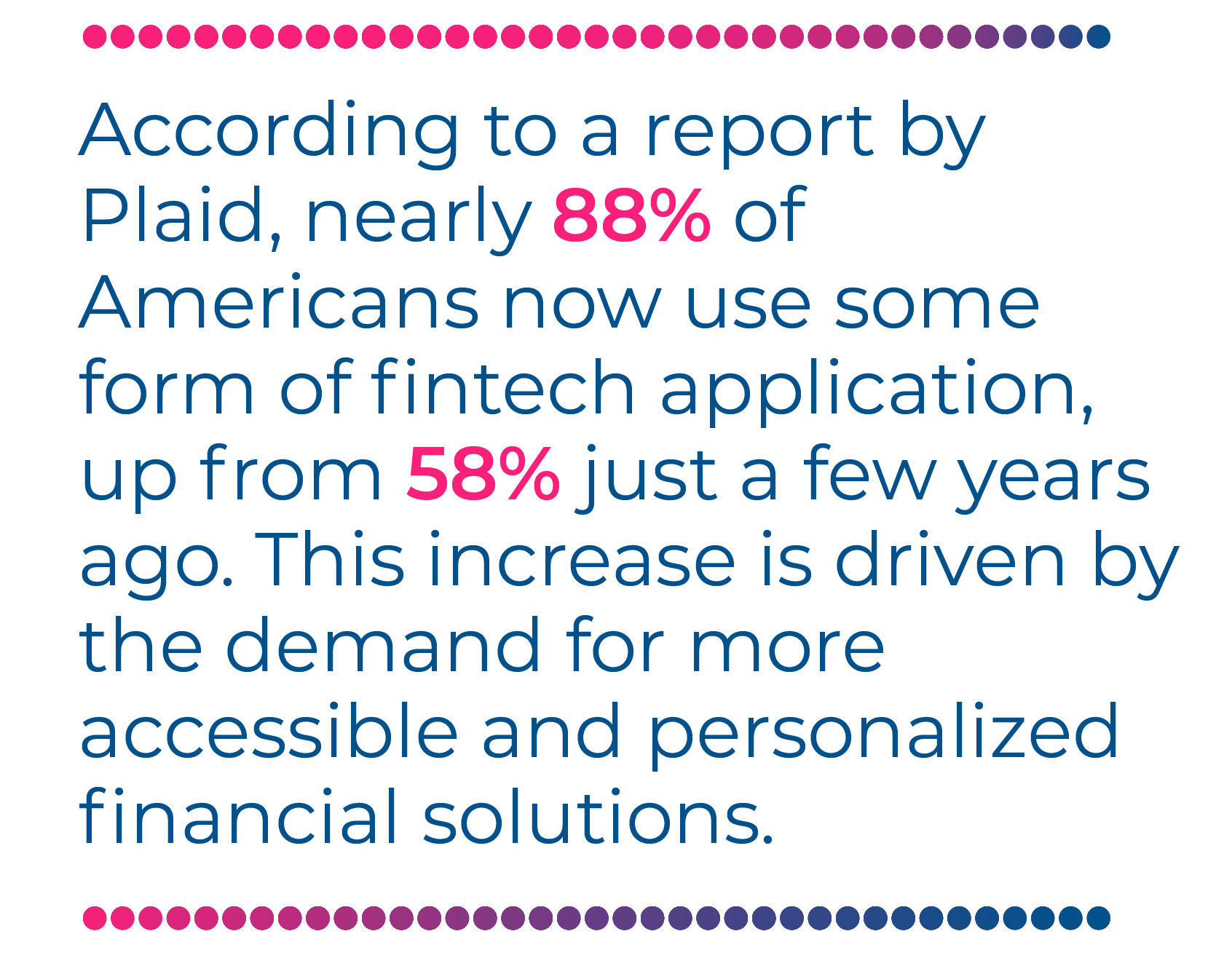

As data and connectivity continue to reshape industries, the financial services landscape is undergoing a paradigm shift. Gone are the days when consumers were content with fragmented financial information across multiple institutions. Innovations like Open Banking have redefined how financial data is shared, paving the way for new opportunities and revolutionizing consumer experiences. Open Banking allowed consumers to share their bank account data with third-party providers, leading to a wave of personalized solutions and competitive offerings that transformed traditional banking.

Today, however, a more profound transformation is underway: Open Finance.

Open Finance represents the next evolutionary step, building upon the foundations of Open Banking to encompass a broader spectrum of financial data.

Unlike its predecessor, Open Finance is not just about sharing bank account information; it covers mortgages, investments, insurance, pensions, and beyond. It gives unprecedented control over their entire financial portfolio, driving a future of hyper-personalized financial services and an inclusive financial ecosystem.

Recent global events, such as the economic shifts induced by the pandemic and the accelerated adoption of digital Finance, have amplified the need for a more integrated financial view.

With Open Banking laying the groundwork, what does the next step, Open Finance, bring to the table?

Beyond Open Banking. What is Open Finance?

Open Finance is poised to be a game-changer, empowering consumers, encouraging innovation, and leveling the playing field across financial services. It integrates different aspects of personal Finance including mortgages, savings, pensions, investments, and insurance—into a unified, accessible digital experience. This interconnectedness gives consumers a holistic financial view, enabling better decision-making, financial planning, and goal achievement.

Pivotal features of Open Finance include

- The ability to access financial product data from multiple providers and integrate it in one place.

- Enhanced financial insights through integrated data analytics can lead to more effective budgeting, saving, and investing.

- Seamless information sharing with authorized financial service providers to deliver personalized services tailored to individual needs.

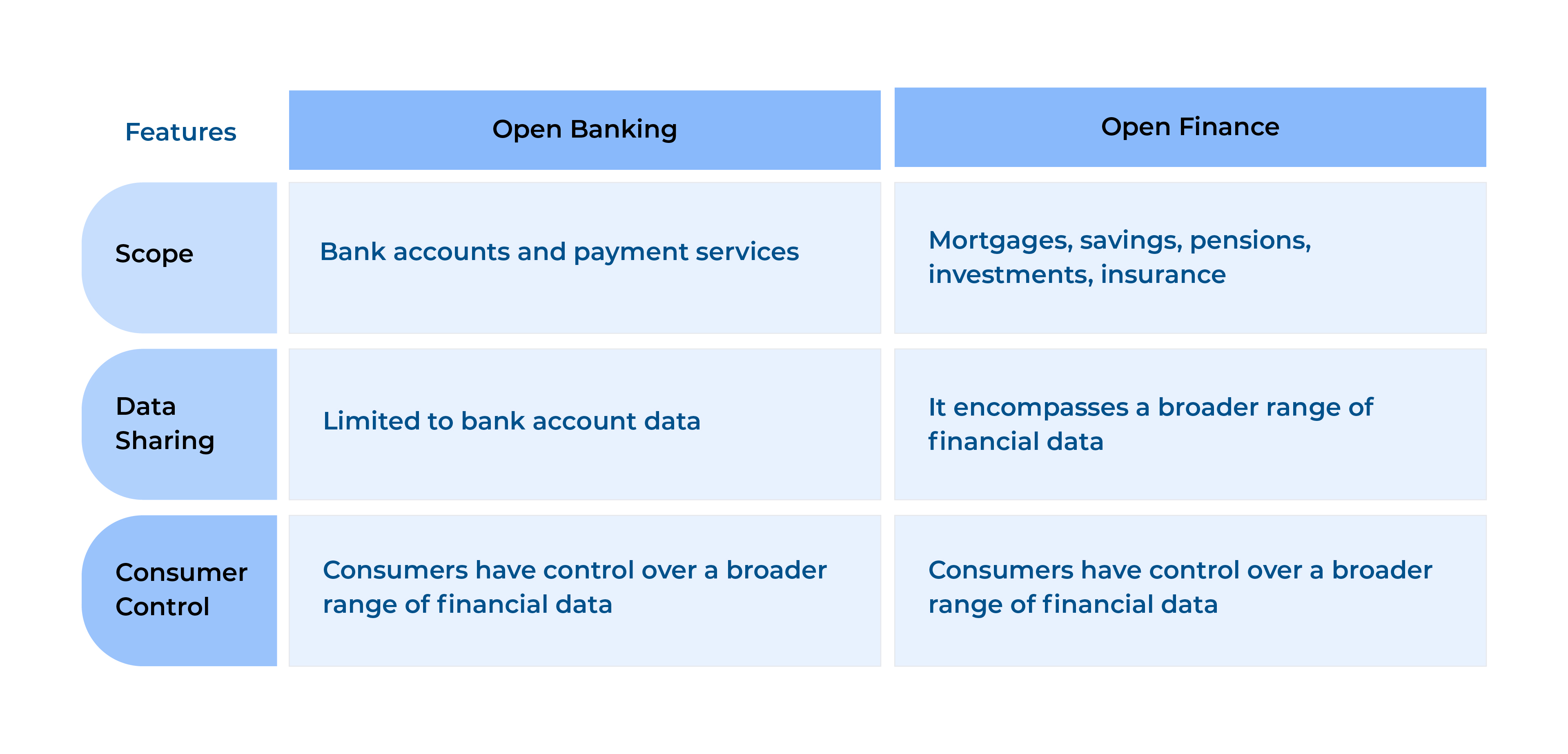

To truly understand Open Finance, it must be differentiated from its predecessor—Open Banking.

From Data Silos to Full Control. Open Banking vs. Open Finance

While Open Banking was a foundational step, focusing primarily on payments and checking accounts, Open Finance extends this concept across the entire financial spectrum. Imagine viewing your pension contributions, insurance policies, mortgage payments, and investment portfolios all in one place that is the promise of Open Finance. Open Finance represents a significant leap forward from Open Banking by addressing consumers’ expectations for greater control, convenience, and customization.

Open Finance represents a significant leap forward from Open Banking by addressing consumers’ expectations for greater control, convenience, and customization. Consumers want to make informed decisions based on a complete picture of their financial health, and Open Finance makes this possible. It is about putting consumers in the driver’s seat and empowering them to manage their financial lives more effectively.

Consumers want to make informed decisions based on a complete picture of their financial health, and Open Finance makes this possible. It is about putting consumers in the driver’s seat and empowering them to manage their financial lives more effectively.

As Open Finance evolves, it involves more than technology it brings together diverse stakeholders across the financial ecosystem.

Building the Open Finance Ecosystem. The Main Players.

Open Finance brings together multiple stakeholders to create a connected ecosystem.

These stakeholders include banks, fintech firms, regulatory bodies, and, most importantly, end consumers. Banks and Financial Institutions serve as custodians of financial data, and through Open Finance, they can leverage these insights to deliver innovative and consumer-centric products.

- Fintech Firms: Fintech companies are at the forefront of utilizing Open Finance data to create new, dynamic applications that provide real-time insights and improve user experiences. For instance, the Latin American fintech Belvo has partnered with multiple financial institutions to enable seamless data integration, enhancing regional financial services.

- End Consumers: Ultimately, the end consumers benefit most from gaining control over their entire financial landscape, allowing them to make well-informed financial decisions.

Setting the Rules. Guidelines for Open Finance

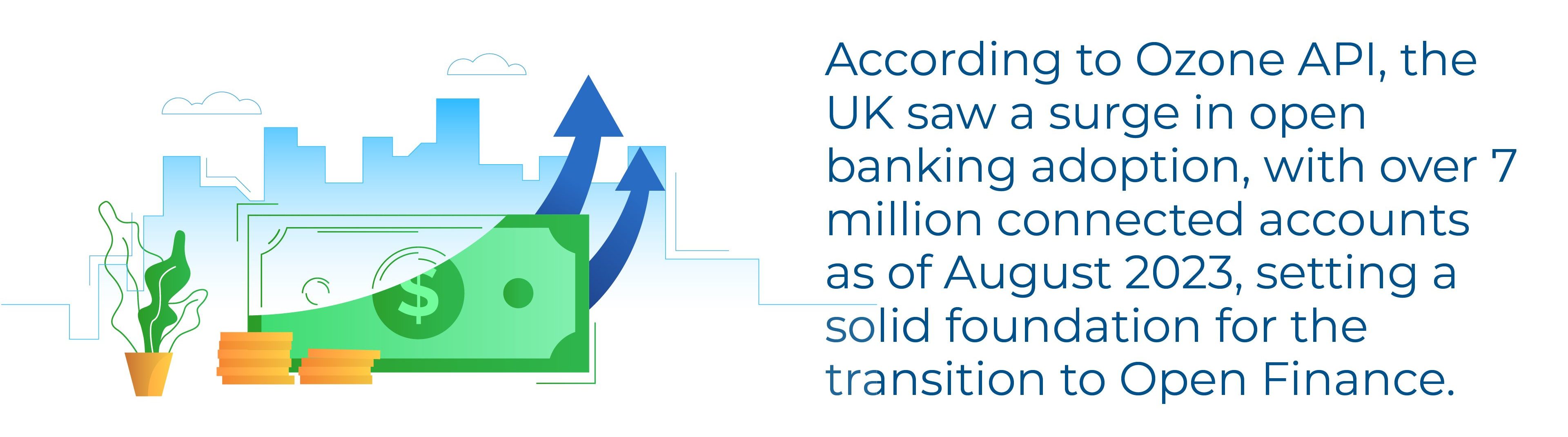

The global regulatory landscape plays a crucial role in shaping Open Finance. Directives such as the European Union’s PSD2 and initiatives by the UK’s Financial Conduct Authority (FCA) have established the framework for secure data sharing, ensuring consumer protection remains a priority. Regulations are crucial in maintaining trust and establishing clear privacy, consent, and data security standards.

The UAE’s Open Finance Regulation (launched by the Central Bank of the UAE) is set to revolutionize the regional financial sector by fostering innovation and competition. By mandating participation from all FIs, the regulation creates a level playing field that encourages innovation and boosts competition among traditional banks and fintech companies. This framework is designed to accelerate the adoption of digital financial services, leading to more seamless banking experiences and increased development of fintech solutions. Furthermore, the regulation promotes financial inclusion by enabling better access to financial data, potentially expanding credit access for underserved segments, and empowering consumers to make better-informed financial decisions.

The United States is making significant strides towards open Finance with the Consumer Financial Protection Bureau’s (CFPB) finalization of the Personal Financial Data Rights Rule in October 2024. This rule, implementing Section 1033 of the Dodd-Frank Act, mandates that financial institutions, including banks, credit card issuers, and other providers, must give consumers free access to their personal financial data and allow them to share it with third parties upon request. Set to be implemented in phases from April 2026 through 2030, the rule aims to boost competition, protect privacy, and enhance consumer choice in financial services. It covers various financial products, including bank accounts, credit cards, and payment apps. Providers must share transaction history, account balances, and payment information through secure APIs.

To Be Continued in Part II

This concludes Part I of our deep dive into Open Finance. In the second part, we build on the discussed concepts, focusing on how Open Finance can deliver real, tangible benefits. We’ll explore the global adoption landscape, the industry-specific challenges, and the key strategies stakeholders need to implement, offering a clearer picture of how Open Finance is transforming the financial services industry.

About the Author

Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.

Avinash brings expertise in strategic delivery, innovative solutioning, and leadership in banking technology. At Maveric Systems, he focuses on advancing BankTech solutions in Wealth Management and Capital Markets, crafting transformative solutions to address client-specific challenges.

For over 25 years, Maveric Systems has been the trusted BankTech expert, empowering financial institutions with domain-driven delivery and cutting-edge technology. Under Avinash’s leadership, Maveric continues to combine deep sector expertise with innovation, enabling clients to thrive in an evolving financial landscape.