Why Banks Must Adopt Digital Transformation Strategies

The goal of digital transformation plans is to make things easy to use and up-to-date. In this age of IoT and emerging deep tech, digital change is essential to stay ahead of the competition. The plan for digital transformation in banking needs hyper-personalized to customers. After Covid, most customers depend on digital technologies, making it even more important to update your old systems before your competitors catch up to you.

Why must banks embrace digital transformation?

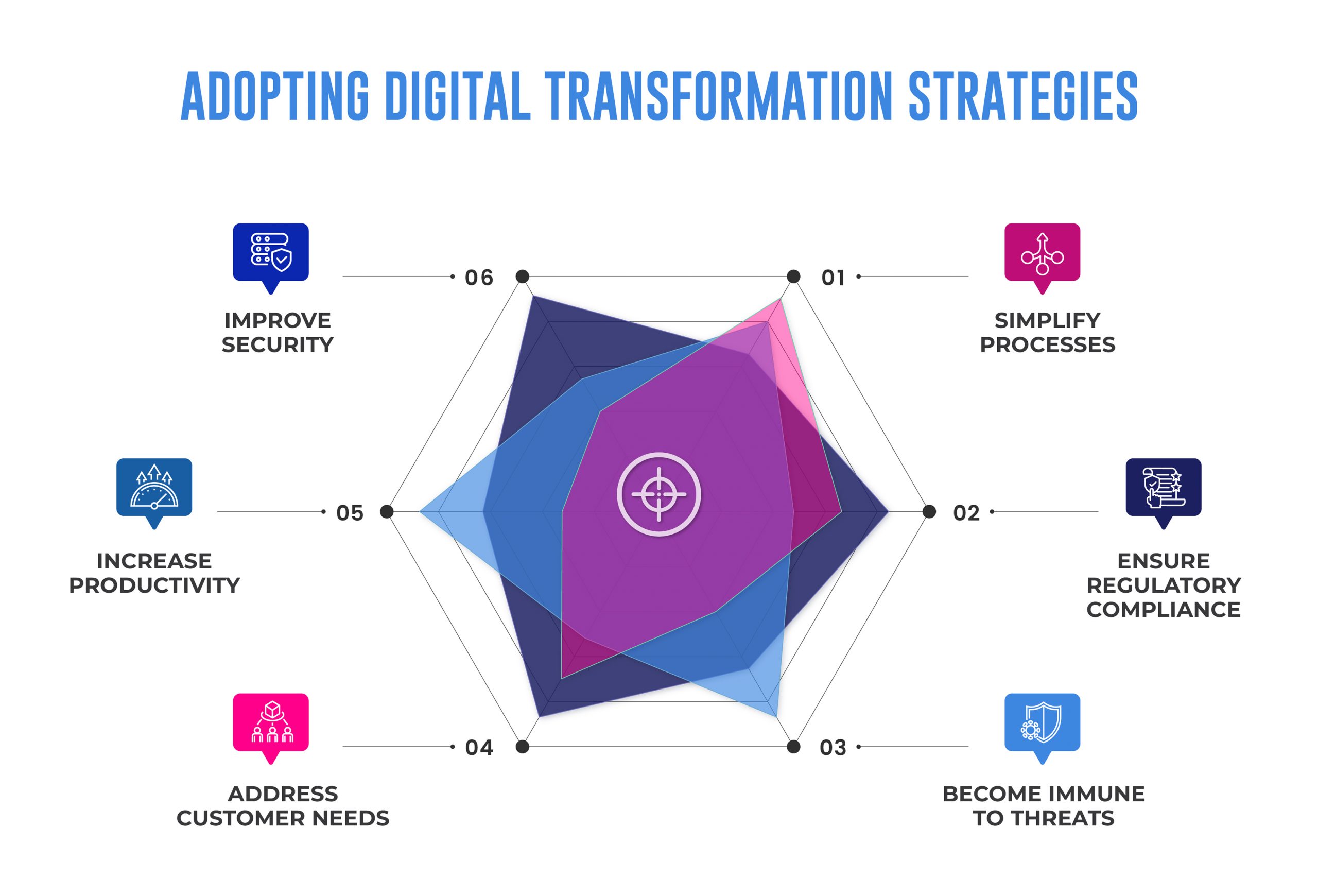

- The customer is important: Make sure you understand what the customer wants. In today’s fast-changing market, customer happiness is based on smooth service delivery, a high-end user experience, a personalized product experience, openness, and safety. In today’s demanding market, businesses have to put the customer first if they want to be successful.

- Continuous Improvement: Continuous improvement requires a pipeline for delivering new ideas that work well and are built on agile concepts. The process should be so good that it’s easy to keep up with changing market trends, test new products, and set up quick ways to get feedback so they can be improved. This cycle quickly leads to on-demand service delivery, constant innovation, and constant improvement, which speeds up go-to-market times.

- Operating Model: Now, buyers want a hybrid experience, which is a mix of a digital experience that has never been seen before in terms of speed and ease of use and the look and feel of the unique product. This can be done by changing the business in three different ways using digital transformation technologies:

Partnering with domain experts in Digital Transformation like Maveric Systems offers leading FIs substantial intellectual capital to pursue the core strategy and grow brand loyalty

Partnering with domain experts in Digital Transformation like Maveric Systems offers leading FIs substantial intellectual capital to pursue the core strategy and grow brand loyalty

- Identify Viable Solutions: Ensure you get everything as you implement the digital transformation plan. Even things you think are old can still help in meaningful ways. Please find all the minimum viable digital transformation options and figure out how to use their potential to their fullest. Then, add them to the digital transformation services. Make sure to use the best and most meaningful choices you already have.

- Use the Strength of Data: Banks should realize how important data and the tools and resources that go with it are to their business success. They need to think more about using data analytics to understand and track customers’ thinking. This helps them make the products that meet customer wants the best. This will also help them learn important market information that will help them improve their products, services, and customer relationships.

Conclusion

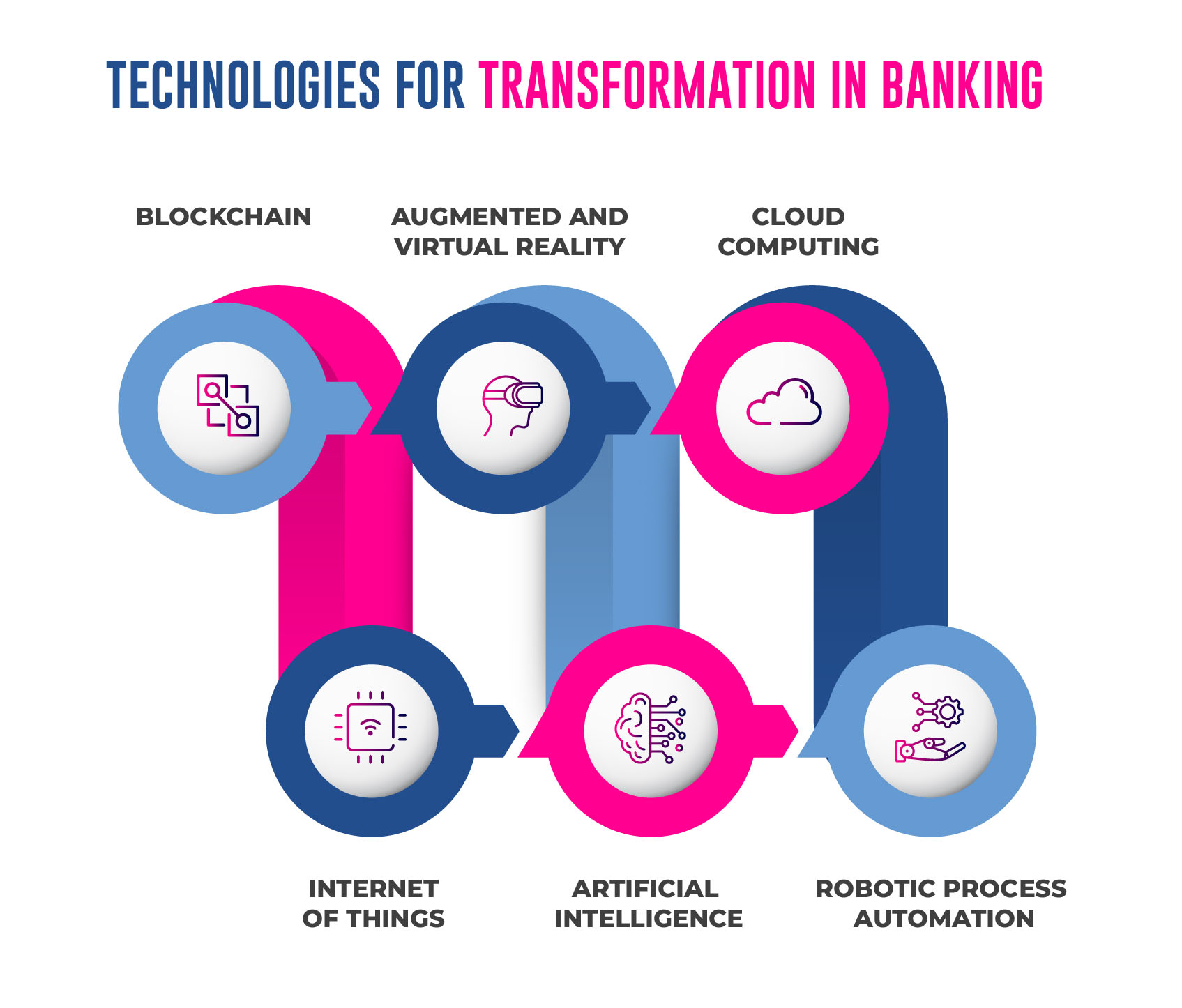

FIs must speed up their transitions to digital banking. The BFSI sector needs to change its front-facing and back-office business models to keep up with how the world is changing and prepare for possible future shocks. Adopting the latest technologies, like blockchain, cloud computing, and the Internet of Things, is the basis of real digital banking and a complete transformation.

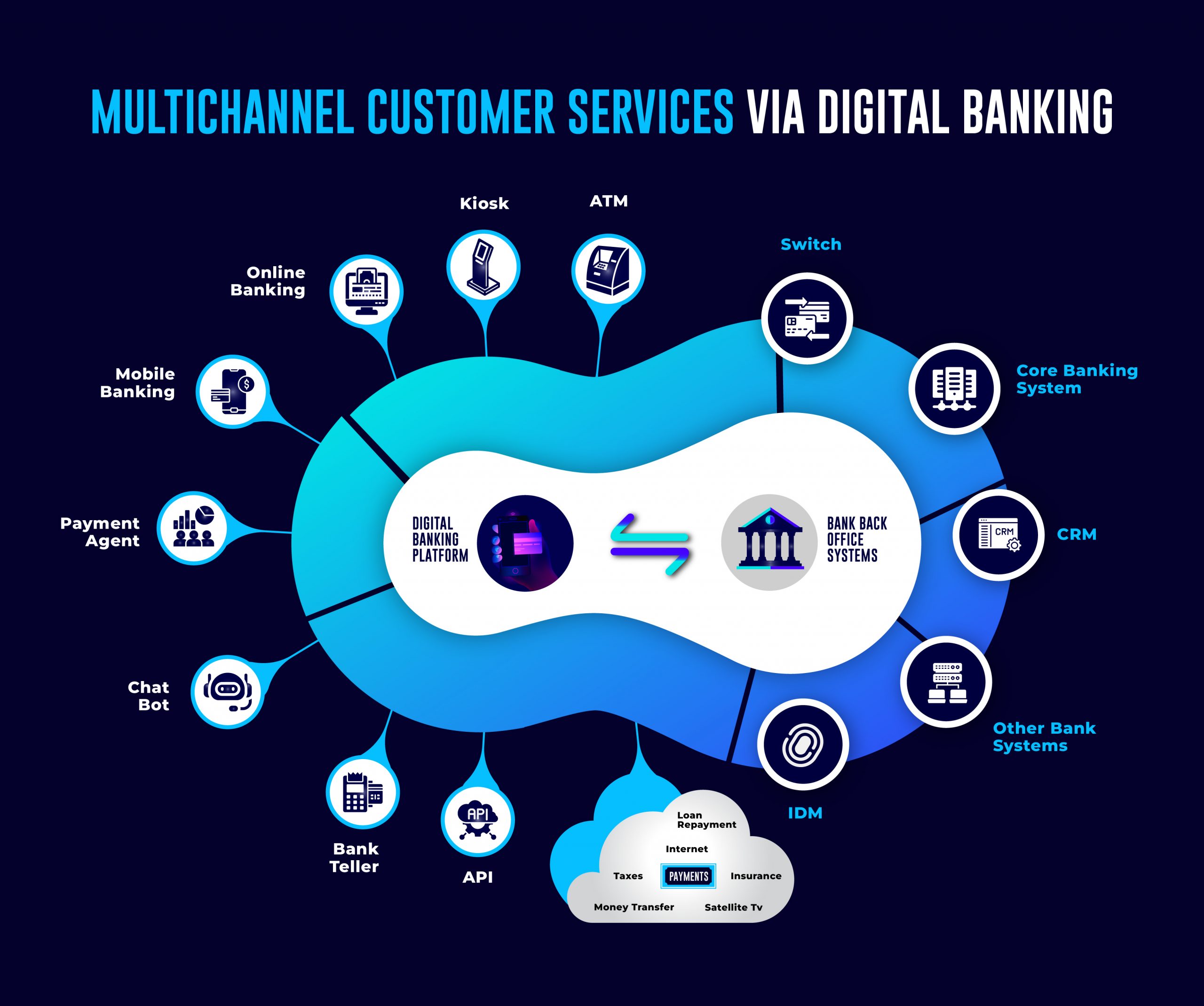

The consumer is the most essential part of any change plan. With interest rates close to 0%, banking fees going down significantly, and customer expectations increasing, financial institutions must use big data to automate business processes and cut costs. Banks can quickly create omnichannel goods, services, and functions by updating their applications with artificial intelligence, cloud technology, and automation.

About Maveric Systems

Starting in 2000, Maveric Systems is a niche, domain-led Banking Tech specialist partnering with global banks to solve business challenges through emerging technology. 3000+ tech experts use proven frameworks to empower our customers to navigate a rapidly changing environment, enabling sharper definitions of their goals and measures to achieve them.

Across retail, corporate & wealth management, Maveric accelerates digital transformation through native banking domain expertise, a customer-intimacy-led delivery model, and a vibrant leadership supported by a culture of ownership.

With centers of excellence for Data, Digital, Core Banking, and Quality Engineering, Maveric teams work in 15 countries with regional delivery capabilities in Bangalore, Chennai, Dubai, London, Poland, Riyadh, and Singapore.

View