Enhancing the Customer Experience in Banking and FinTech

Several companies make it simple for customers and entrepreneurs to do all their financial transactions online, providing convenient access to banking services whenever and wherever they need them. Online banking is a suitable alternative to “traditional,” in-person banking, especially among younger generations.

Even though the vast majority of brick-and-mortar banks now provide some online banking services, there may be more they can do to differentiate themselves and win over modern customers. Making customers happy can mean the difference between success and failure. Many millennials will look elsewhere if they can’t bank from their phone.

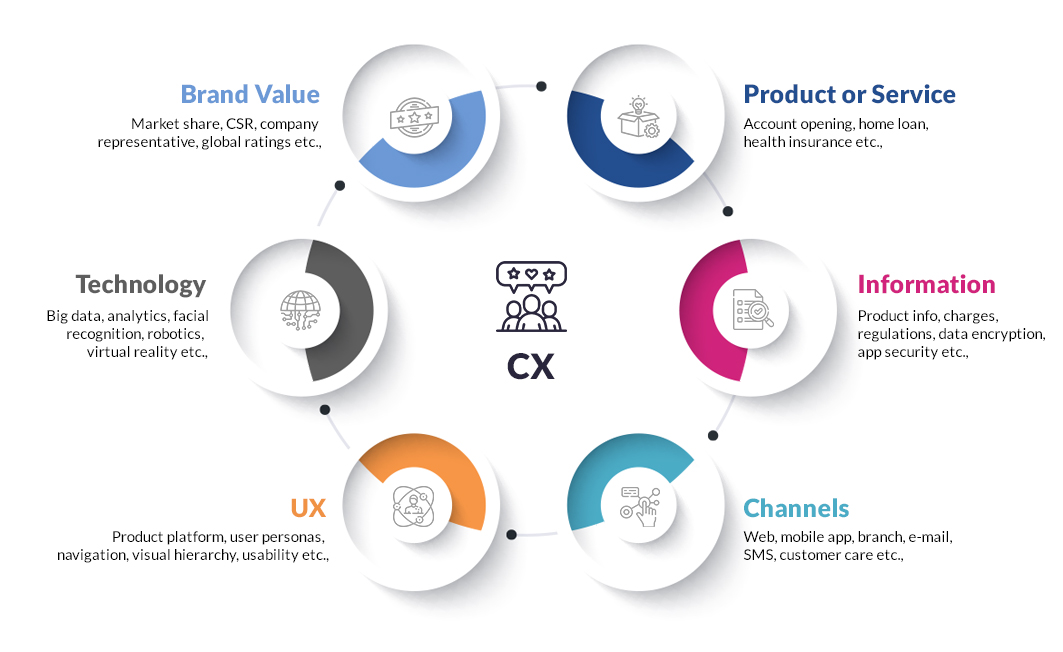

Consistency and efficiency in Banking services define Customer Experience

The banking industry is no different from any other service industry in that the quality of service to the customer is entirely dependent on the customer’s expectations. A bank customer’s experience with a teller may be pleasant for one person but frustrating for another.

However, what constitutes a positive banking encounter can be standardized. Having a unified profile of your customers across all touchpoints is crucial to providing excellent service. Whether a customer interacts with you in person, over the phone, or on the web, they will always receive the same high-quality service and seamless experience from the bank. Experienced banking customers know when they have received top-class service.

The future of CX in Banking

The emergence of FinTech start-ups was a major driving force behind the digitization of banking procedures, which compelled traditional financial institutions to improve their methods for providing financial services to customers. Similarly, banks are undergoing digital transformations, automating processes across entire departments to reduce overhead. To understand how these landscape-shaping trends impact Customer experience in FIs, the banking domain and tech experts like Maveric Systems bring a fresh approach.

Enhancing CX through Product and Service Innovation

Strategic requirements in banking tend to fluctuate over time. The banking industry is shifting its attention from improving the client experience to developing new products. Message and offer (sometimes masked as “advice”) customization have taken a backseat to product personalization in recent years. Banking as a service (BaaS) providers collaborate with fintech and non-financial brands to manage the overall customer experience.

There is room to enhance the experience of using conventional banks.

Three critical considerations for amplifying CX in Banking and Fintechs

- Data: Credit card purchases, cash withdrawals, credit history, and other financial tools generate an enormous amount of data. The more information fintech companies have about their clients, the better they can meet their needs. Insights like these allow for more tailored promotions to specific audiences.

- Hyper-personalization: Customers are more receptive to targeted advertisements. – In addition, AI and ML are being used to provide consumers with on-demand credit at reduced rates and other hyper-tailored offers specific to their financial situations.

- Loyalty and Total Wallet Share: Clients’ income, investment history, tolerance for risk, and other factors are used by investment platforms to make personalized recommendations for investment opportunities. Evidence suggests that a higher proportion of a customer’s spending comes from happier clients; in fact, one study found that a client’s likelihood of becoming a profitable customer increased by 2.4% for every point of increase in satisfaction.

Conclusion

Due to the increasing digitization of everything in existence, banks are increasingly prioritizing innovation in customer service. Bain & Company polled 111,000 clients in 2015 on whether they would miss their mobile phones or wallets more. The fact that more than half of consumers opted to pay with their phones instead of wallets is evidence of how much the mobile and digital revolution has altered society at large and, in particular, people’s perspectives on money and their ability to manage their day-to-day finances.

About Maveric Systems

Starting in 2000, Maveric Systems is a niche, domain-led Banking Tech specialist partnering with global banks to solve business challenges through emerging technology. 3000+ tech experts use proven frameworks to empower our customers to navigate a rapidly changing environment, enabling sharper definitions of their goals and measures to achieve them.

Across retail, corporate & wealth management, Maveric Systems accelerates digital transformation through native banking domain expertise, a customer-intimacy-led delivery model, and a vibrant leadership supported by a culture of ownership.

With centers of excellence for Data, Digital, Core Banking, and Quality Engineering, Maveric Systems teams work in 15 countries with regional delivery capabilities in Bangalore, Chennai, Dubai, London, Poland, Riyadh, and Singapore.

View

This blog deliberates on the challenges the traditional banking sector faces that emergent technologies can fix.

This blog deliberates on the challenges the traditional banking sector faces that emergent technologies can fix. Conclusion

Conclusion