Why This Article Matters

Core banking modernisation is not a new challenge. What is new is the standard that AI-first operations require it to meet – and the consequence of meeting that standard partially rather than fully. This article makes the insight that most core modernisation programmes miss: AI redistributes and amplifies risk before it reduces it. The transition period – while the new architecture is being built and intelligence is being integrated into a core in active evolution – is a period of elevated, not reduced, risk. The four architectural shifts described here each open a specific migration risk window. Understanding what that window contains – and how to govern it – is what separates successful modernisation from faster fragility.

The Structural Mismatch

Core banking systems were engineered for a specific and well-understood purpose: transaction accuracy, data integrity, and operational stability under high volume. They achieved that purpose. They were not engineered for real-time inference, continuous model integration, event-driven data flows, and probabilistic decisioning.

The result is a structural mismatch that most institutions are managing through layering – adding AI capabilities on top of legacy cores rather than re-architecting the underlying systems. This generates a specific and predictable failure pattern: the AI layer makes a decision based on data that the core system has not yet updated, because the core runs on a batch cycle.

A fraud detection model flags a transaction as high-risk based on real-time behavioural signals, while the core updates account status overnight. A credit decision engine approves a limit based on data that will only be refreshed in the next batch run. The AI is technically correct at the moment of inference. By the time the decision is acted upon, it is based on a representation of reality that no longer holds.

This is not a marginal inefficiency. It is a structural reliability risk that compounds as the AI estate scales and the gap between decision speed and core update frequency widens.

The Central Insight: AI Redistributes and Amplifies Risk Before It Reduces It

This is the observation that core banking modernisation programmes most consistently underestimate.

AI does not eliminate the risks that the legacy core was designed to contain. It redistributes them. The risk of incorrect data – which the legacy core managed through batch reconciliation and human oversight – becomes the risk of real-time data inconsistency, which propagates at the speed of the new architecture and surfaces in live decisions before human oversight can catch it.

And AI amplifies risk in proportion to the velocity and scale at which it operates. A legacy core that makes a wrong decision in a batch cycle makes that decision for the transactions in that batch. An AI-enabled core that makes a wrong decision in real time makes that decision at the speed and volume of live operations – across thousands of transactions, in the time it takes to detect the error.

This is not an argument against modernisation. It is an argument for governing it with the rigour that its risk profile demands – specifically for understanding that the risk management question is not ‘how do we protect the migration?’ but ‘how do we ensure the AI-enabled core amplifies confidence as efficiently as it amplifies decision velocity?’

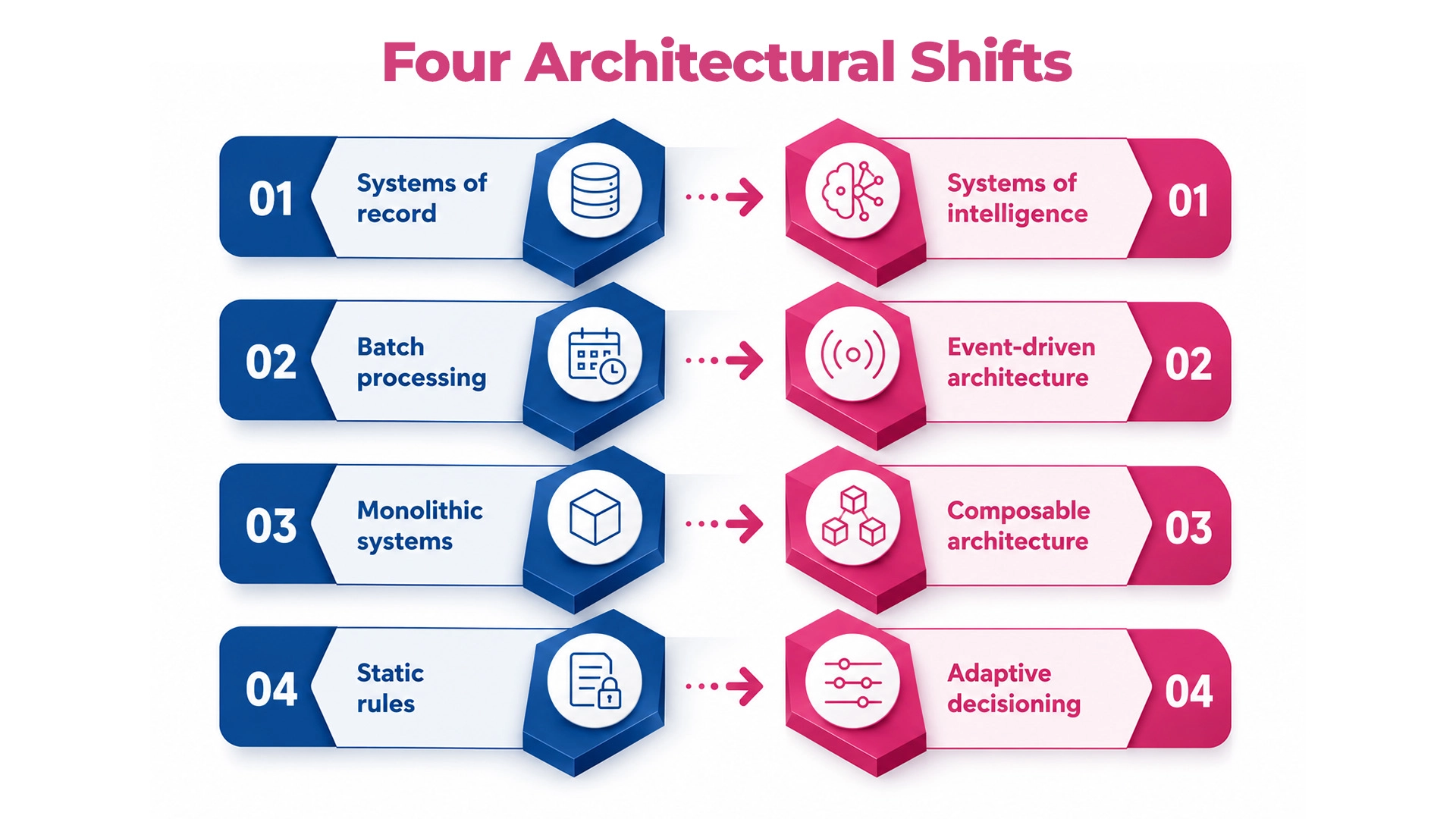

Four Architectural Shifts – And What Each One Demands

Shift 1: From Systems of Record to Systems of Intelligence

In a system of record, the core stores authoritative state. Other systems query it. In a system of intelligence, the core must maintain state in real time, expose it through interfaces that AI models can consume at inference speed, and ensure the state it exposes is consistent across every system that depends on it simultaneously.

The governance discipline: data consistency as a first-class architectural requirement – a defined, monitored, enforced standard for how quickly state changes propagate to every consuming system, with explicit governance of the lag tolerance that each AI model has for the data it consumes.

MIGRATION RISK

Moving from storing authoritative state to exposing it in real time, before consistency enforcement infrastructure is in place, creates a period where the core is exposing data faster than it can guarantee its accuracy. This is when real-time AI decisions are most likely to be made on information that does not reflect the actual state of the account.

Shift 2: From Batch Processing to Event-Driven Architecture

Every significant state change generates an event that propagates through the system in real time. AI models subscribe to relevant events and update their inputs continuously. The governance discipline: event integrity and ordering guarantees. Events delivered out of sequence, duplicated, or lost in transit produce data states inconsistent with the actual sequence of events that occurred.

MIGRATION RISK

The period during which batch processes and event-driven processes run in parallel – the standard migration approach – is when the same data is being updated by two systems with different consistency guarantees. AI consuming from one system may be inconsistent with the other.

Shift 3: From Monolithic Systems to Composable Architecture

A composable core enables AI services to be integrated, updated, and replaced as independent components without requiring changes to the core transaction processing infrastructure. The governance discipline: API contract governance and service dependency management. A change in the core’s data interface must trigger managed updates in every consuming AI service – not be discovered when the AI service silently begins consuming through a deprecated interface.

MIGRATION RISK

Deploying AI services against interfaces that are not yet stable, in an architecture that is not yet fully composable, creates integration dependencies harder to manage than the monolithic dependencies they were supposed to eliminate.

Shift 4: From Static Rules to Adaptive Decisioning

In a rule-based core, governance is straightforward: document the rules, audit their application. In an AI-driven core, governance requires the ability to reconstruct why a specific inference was made for a specific transaction at a specific moment – using the specific data state that existed at that moment. The governance discipline: decision-level audit infrastructure built before adaptive decisioning goes live.

MIGRATION RISK

The period between deploying adaptive decisioning and completing audit infrastructure is a period of unaccountable operation – where the system is making AI-driven decisions that cannot be retrospectively explained. Every day that period extends is another day of decisions that cannot satisfy a regulatory reconstruction request.

What the Re-Architected Core Must Ensure

When the four shifts have been executed with the governance discipline each demands, the AI-enabled core’s purpose has expanded: not just processing transactions correctly, but ensuring that every decision flowing through it is reliable, explainable, and consistent – all four properties of outcome trust operating at the transaction level.

A core that has been modernised for speed but not for intelligence is faster and more fragile than what it replaced. A core that has been modernised for composability but not for auditability is more flexible and less accountable. The institutions navigating this correctly are those that build the trust infrastructure for each shift before the shift goes live – not after it has accumulated the governance debt that a regulatory examination will eventually find.

The core is no longer just where transactions are processed. It is where trust is continuously executed – or where, in its absence, the entire AI-first transformation discovers its ceiling

Core banking modernisation in the context of the full Four-Layer Trust Architecture – how the data trust and system trust layers apply specifically to the re-architected core, and what governance infrastructure each shift requires – is examined in full in the research report.

Download the Full Research Report: Engineering Trust in AI-First Banking

What to Read Next

PREVIOUS: AI Banking Solutions: Capability Without Trust Does Not Scale

NEXT: AI-in-Compliance: From Automation to Assurance – the proving ground for every trust claim

This article is part of the Engineering Trust in AI-First Banking series, examining the framework that separates institutions that scale AI from those that stall.

FAQ

1. What are the four architectural shifts required to make core banking AI-ready?

The four shifts are: from batch-based to real-time data architecture (enabling AI models to consume live transaction and customer data rather than overnight snapshots); from monolithic to modular systems (allowing AI capabilities to be integrated without destabilising the core); from periodic to continuous data governance (ensuring model inputs are validated at the point of consumption, not assumed from source systems); and from rule-based to intelligence-augmented decisioning (where AI supplements or automates decisions in lending, deposits, and payments with appropriate governance overlays).

2. Why is the transition period of core banking modernisation described as the most dangerous phase?

During transition, institutions are simultaneously operating legacy systems and new architecture – with data flowing across both environments and AI models consuming inputs from mixed sources. Data consistency, lineage traceability, and governance coverage are all at their weakest during this period, precisely when the complexity of managing two environments simultaneously makes oversight hardest. Banks that compress this transition to accelerate deployment often accumulate governance debt that surfaces as production incidents or regulatory findings six to twelve months after go-live.

3. How does AI-enabled core banking differ from core banking modernisation without AI?

Standard core banking modernisation focuses on replacing legacy transaction processing with more scalable, cloud-native infrastructure. AI-enabled core banking requires the additional capability to expose clean, governed, real-time data to AI models – and to integrate AI-driven decision logic into core workflows in ways that are explainable, auditable, and maintainable. The architectural requirements are different: specifically, data contracts between the core and AI systems, continuous monitoring of model behaviour within core processes, and explainability infrastructure at the transaction decision level.

4. What is the role of data integrity in AI-enabled core banking transformation?

Data integrity is the foundational constraint that determines whether AI-enabled core banking delivers on its promise. Core banking systems are the primary source of the data that AI models consume – and if that data is inconsistently governed, poorly lineaged, or not validated at the model input boundary, the AI systems built on top of it will produce unreliable outputs regardless of model sophistication. In practice, most core banking AI failures trace back to data integrity gaps that existed before the AI was deployed and were exposed, rather than caused, by AI deployment.

5. How should a bank sequence AI capability development during a core banking transformation programme?

Sequence trust infrastructure first, AI capability second. Specifically: establish data governance and lineage tracking across the modernised architecture before deploying AI models that depend on it; embed continuous validation in the CI/CD pipeline before increasing deployment frequency; and define explainability requirements at the architecture design stage before model development begins. Institutions that invert this sequence – deploying AI early to demonstrate progress, then attempting to retrofit governance – consistently report higher remediation costs and longer time-to-trust than those that sequenced correctly.