CX ROI in Banking: Linking Customer Experience to Business Outcomes

In the fiercely competitive world of banking, products and rates are no longer the sole differentiators. Today, Customer Experience (CX) has become the battleground where loyalty is won or lost. But as CX teams advocate for greater investments in design, technology, and service, business leaders ask a critical question:

❝ What’s the return on investment for improving customer experience? ❞

The answer? When done right, CX isn’t a cost center — it’s a growth engine.

Why CX Matters More Than Ever in Banking

The modern customer expects anytime-anywhere access, hyper-personalized communication, and zero friction across channels — whether digital or physical. But it’s not just about meeting expectations. It’s about understanding how meeting (and exceeding) those expectations impacts key financial metrics.

Let’s break it down:

How Great CX Directly Impacts Business Outcomes

1) Retention and Loyalty Drive Long-Term Revenue

Acquiring a new banking customer costs 5–7x more than retaining an existing one.

- CX initiatives that reduce customer pain points—like streamlining onboarding, improving app navigation, or enabling instant issue resolution—lead to higher retention.

- Loyal customers are more likely to stay through rate fluctuations, new fees, or minor errors.

ROI Link: A 5% increase in retention can increase profits by 25%–95%. That’s direct revenue, saved acquisition costs, and greater LTV.

2) Satisfied Customers Expand Their Relationship

Customers who feel valued are 4x more likely to buy additional products.

- A seamless credit card application, a frictionless mortgage journey, or proactive fraud alerts build trust—and trust builds wallet share.

- Predictive CX, powered by data, enables timely offers: “You’re pre-approved for a home loan” hits differently when it appears just after a customer browses listings.

ROI Link: Higher cross-sell and upsell rates improve revenue per customer and drive down average acquisition cost per product.

3) Digital CX Reduces Cost-to-Serve

A digital transaction costs a fraction of an in-branch or call center interaction.

- But digital migration only works if the experience is delightful.

- Banks investing in user-centric mobile apps, AI chatbots, and seamless KYC verification are seeing massive adoption—and saving millions.

ROI Link: Reduction in branch traffic and support center load leads to direct operational cost savings.

4) Promoters Fuel Organic Growth

82% of consumers trust recommendations from friends and family over ads.

- When customers are happy, they don’t just stay—they recommend.

- A single promoter may bring in 2–3 new customers, and in high-trust domains like banking, those referrals convert faster and churn less.

ROI Link: Higher NPS leads to referral-based growth and reduced acquisition spend.

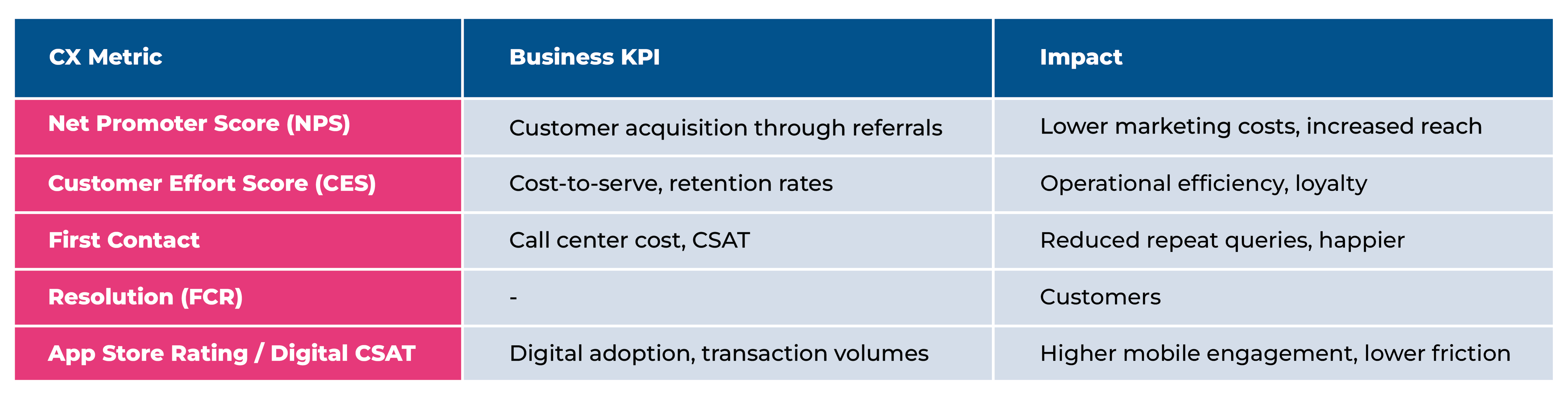

Proving the ROI: CX Metrics vs. Business KPIs

To make CX investments boardroom-proof, banks must connect experience data with financial impact.

Real-World Examples: CX That Pays Off

DBS Bank

Used customer journey mapping to streamline digital onboarding. Result:

- 3x increase in mobile onboarding

- 30% higher cross-sell in digital customers

Barclays

Introduced personalized financial coaching in-app. Result:

- 15% boost in NPS

- Increased uptake in investment products

ICICI Bank (India)

Revamped WhatsApp banking and chatbot services. Result:

- 60% drop in call center volumes

- $1.2M in annual cost savings

Final Word: CX is Strategy, Not Support

When you invest in customer experience, you’re not just designing better journeys you’re designing better financial performance.

The most future-ready banks are those that:

- Treat CX as a strategic lever

- Build a culture of continuous listening and improvement

- Marry customer insight with business analytics to track ROI

Bottom Line:

Happy customers stay longer, buy more, cost less to serve, and bring in others. That’s not just good CX — that’s smart business.

With 25 years of expertise in BankTech, Maveric Sytstems has been at the forefront of driving transformative solutions in the banking domain. Through the Maveric BankTech Insights newsletter, we bring you deep insights overcome digital friction in Banking that not only attract but also retain and delight customers for the long term.

Wish to know more? Subscribe to our Newsletter

View

Cross-functional organizations, eliminate the inefficiencies of multiple handoff that result in productivity lapses impacting end customer satisfaction. Cross functional organizations seamlessly integrate the engineering skills in the operations teams, thereby ensuring not only the reliability and availability of the platform but also significantly reducing the lead time for critical issues. Availability of moder observability solutions deliver right insight about the topography while Introduction of AI, accelerates the speed of delivery. This whole chain come together effectively to make sure that the business is able to focus on what matters to them, and measure them effectively, instead about worrying about the system efficiency.

Cross-functional organizations, eliminate the inefficiencies of multiple handoff that result in productivity lapses impacting end customer satisfaction. Cross functional organizations seamlessly integrate the engineering skills in the operations teams, thereby ensuring not only the reliability and availability of the platform but also significantly reducing the lead time for critical issues. Availability of moder observability solutions deliver right insight about the topography while Introduction of AI, accelerates the speed of delivery. This whole chain come together effectively to make sure that the business is able to focus on what matters to them, and measure them effectively, instead about worrying about the system efficiency.