AI risk in banking is the set of exposures created when a model’s decisions can’t be explained, reproduced, or defended under regulatory examination, ranging from unfair credit outcomes to compliance failures that surface only after a customer or examiner challenges a specific decision. For a CRO or CIO evaluating an AI roadmap, understanding these risks as engineering failure patterns, not abstract governance concerns, is what makes them possible to design against before they show up in production.

Why AI Risk Looks Different in Banking Than in Other Industries

In most industries, an AI system that performs well on aggregate accuracy is considered successful. In banking, a model can hit strong benchmark accuracy and still create serious risk exposure, because the standard that matters isn’t how often the model is right in a controlled test. It’s whether any individual decision, a specific credit denial, a specific fraud flag, a specific compliance escalation, can be traced back to the data and logic that produced it and defended to a regulator or customer who challenges it. That single distinction, between aggregate accuracy and individual accountability, is the source of most AI risk in banking that doesn’t show up until an examination or a customer complaint forces it into the open.

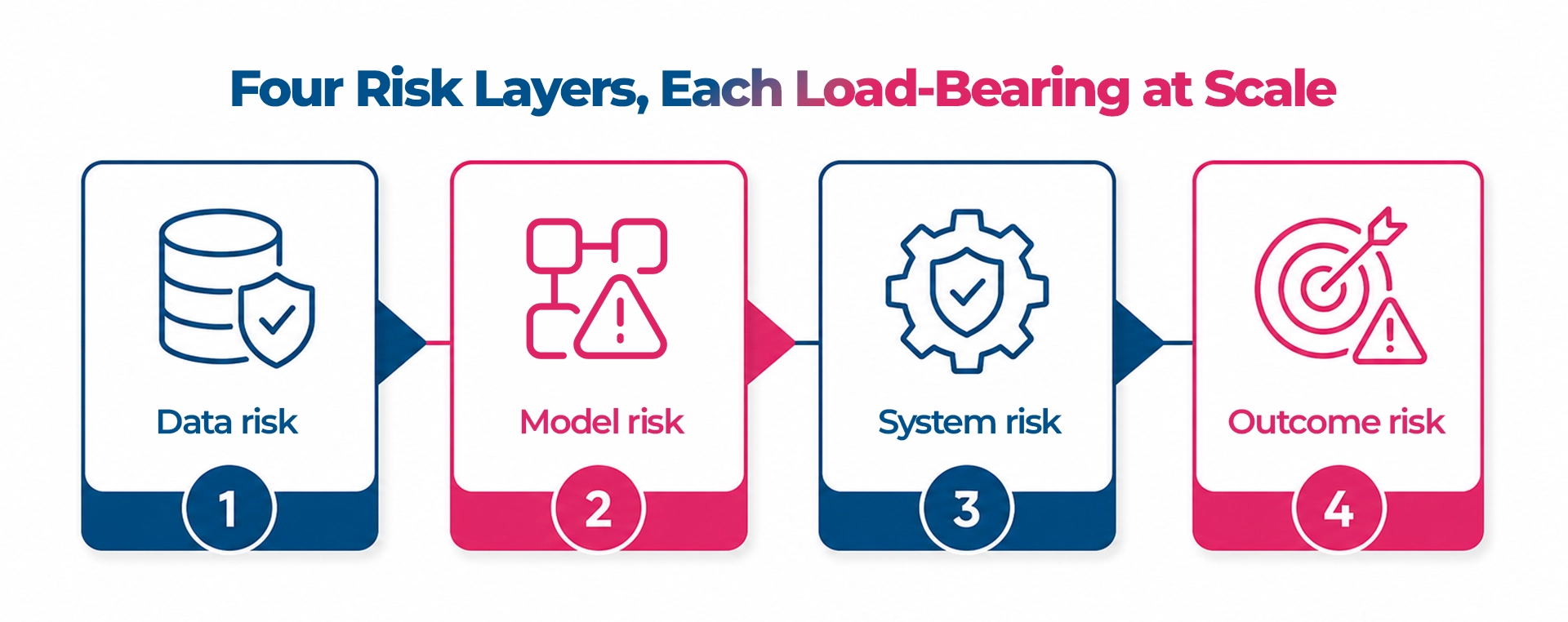

Four Risk Layers, Each Load-Bearing at Scale

AI risk in banking breaks down cleanly into four layers, and each one is largely inconsequential in a small pilot but becomes load-bearing the moment AI moves into production decisioning:

1. Data risk:

the accuracy, completeness, and reliability of the data an AI engine depends on. A data risk failure means a fraud model trained on historical patterns starts systematically misclassifying behavior that has shifted since training, often without anyone noticing until loss rates move.

2. Model risk:

explainability, bias, and drift. A model risk failure means a credit decision triggers a regulatory inquiry because there’s no audit trail supporting the specific inference behind it, even if the model’s aggregate accuracy looks fine.

3. System risk:

Integration stability and resilience across environments. A system risk failure surfaces as inconsistent behavior between the environment a model was tested in and the live production environment it actually runs in.

4. Outcome risk:

consistency and auditability of decisions over time and at scale. An outcome risk failure means the institution can’t demonstrate, months or years later, that a batch of decisions was made consistently and compliantly.

These aren’t hypothetical categories. Governance failures across these four layers have already prompted regulatory action in multiple jurisdictions, which is why treating them as engineering requirements rather than compliance checkboxes has become the operating standard for institutions that want to scale AI without accumulating risk faster than they can manage it.

The Regulatory Frameworks Shaping AI Risk Today

AI risk in banking doesn’t exist in a regulatory vacuum, and the frameworks that define acceptable risk are specific enough that generic AI risk management approaches consistently fall short. BCBS 239 requires demonstrable data lineage and accuracy under stress conditions for risk data aggregation. SR 11-7, now updated to SR 26-2, governs model risk management and mandates validation of every model before deployment, explicitly including AI models. The EU AI Act classifies credit scoring and risk assessment tools as high-risk AI systems subject to pre-market conformity assessments. Under these frameworks, an AI model used for credit or risk decisions isn’t treated as software; it’s treated as a regulated model, with the validation and documentation obligations that classification carries.

The Risk of Underuse Is as Real as the Risk of Overuse

Most conversations about AI risk in banking focus on the danger of deploying AI too aggressively without adequate testing, and that risk is real. But research shows nearly half of banks fall into the opposite failure mode too: underusing AI systems they’ve already validated, out of caution that isn’t calibrated to the actual risk profile of the use case. Both failure modes carry a cost. Overuse of undertested AI creates regulatory and reputational exposure. Underuse of validated AI is a slower-burning risk: competitors capture the efficiency and customer experience gains while your institution continues paying the fully-loaded cost of the manual process the AI was built to improve.

Designing Against Risk Instead of Auditing for It

Most AI governance in banking today is retrospective: risk gets identified after deployment, documented after an incident, explained only after a regulatory query. That pattern is remediation, not risk management. Designing against AI risk means specifying fairness, explainability, reliability, and privacy requirements before model training begins, treating bias checks as automated deployment gates rather than annual reviews, and generating audit trails as a natural output of the delivery pipeline rather than reconstructing them under examination pressure. The difference between reconstructed documentation and embedded traceability is structural: reconstruction is approximation, and examiners increasingly know the difference.

What This Means for the CRO and CIO Agenda

The institutions that manage AI risk well aren’t the ones deploying the least AI. They’re the ones who’ve engineered fairness, explainability, reliability, and privacy into the architecture from the start, so that risk is a designed-for property of the system rather than something discovered during an examination.

The Architecture of Trust in AI-Driven Banking whitepaper maps the four-layer trust architecture, data, model, system, and outcome trust, that turns AI risk management from a retrospective audit exercise into a designed-in engineering discipline.

FAQs

1) What are the main categories of AI risk in banking?

Four load-bearing layers: data risk (the reliability of the data feeding a model), model risk (explainability, bias, and drift), system risk (integration stability across environments), and outcome risk (consistency and auditability of decisions at scale over time).

2) Why can a highly accurate AI model still create regulatory risk?

Because regulators and examiners increasingly evaluate accountability, whether a specific decision can be traced back to the data and logic behind it, not just aggregate statistical accuracy. A model can perform well on a benchmark and still fail an examination if individual decisions can’t be explained.

3) Which regulations most directly shape AI risk management in banking?

BCBS 239 (data lineage and accuracy for risk aggregation), SR 11-7, now updated to SR 26-2 (model risk management and validation), and the EU AI Act’s high-risk classification for credit and risk assessment tools are the frameworks most directly relevant to AI-driven credit, fraud, and compliance decisions.

4) Is underusing validated AI actually a risk?

Yes. Nearly half of banks fall into a pattern of either underusing AI they’ve already validated or over-relying on AI that hasn’t been adequately tested. Underuse doesn’t create regulatory exposure the way overuse can, but it’s a competitive risk, since it leaves efficiency and customer experience gains on the table.

5) How does a bank move from reactive AI risk management to designed-in risk management?

By specifying fairness, explainability, reliability, and privacy requirements before model training begins, treating bias and fairness checks as automated deployment gates rather than periodic reviews, and generating audit trails as a byproduct of the delivery pipeline instead of reconstructing them after an incident or examination.