80% of large financial institutions have AI in core decision-making. Fewer than 12% have the governance infrastructure that doing so responsibly requires. This article defines trusted AI in banking with operational precision – four specific capabilities, five structural failure patterns, and the mandate reframe that defines AI-first leadership.

Why This Article Matters

Your institution has AI in production. So does every institution on your competitive landscape. The question that now divides the market is not ‘who has more AI’ but ‘whose AI can actually be trusted.’ This article defines trusted AI with operational precision, not as an aspiration or a marketing category, but as a four-property engineering standard with specific regulatory, architectural, and governance implications. If you have ever asked what it would actually take to feel genuinely confident in your AI estate, this is the answer.

The Question Every Banking Leader Is Being Asked and the More Important One They Aren’t

There is a question that almost every banking technology leader has been asked in the last two years – by their board, their CEO, or their regulator: ‘Are you using AI?’ The answer, almost universally, is yes. Fraud detection models. Credit scoring algorithms. Customer-facing chatbots. AML transaction monitoring. AI embedded, in some form, across nearly every major function.

Ask a different question – ‘Do you trust your AI?’, and the answer becomes considerably more complicated.

That shift, from the first question to the second, is the most important transition in AI in financial services today.

The Adoption Illusion

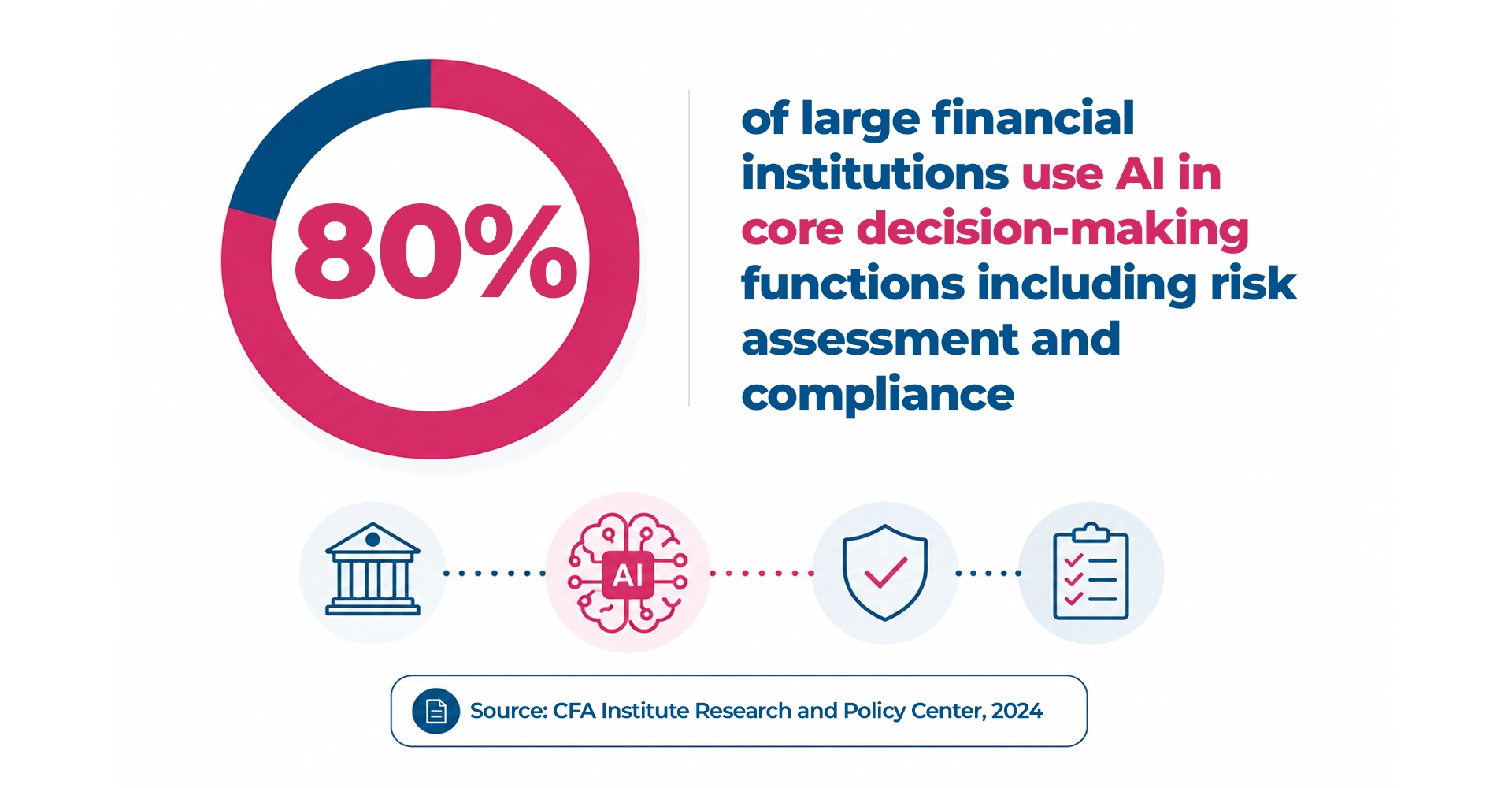

80% of large financial institutions use AI in core decision-making functions including risk assessment and compliance (CFA Institute Research and Policy Center, 2024)

But adoption statistics measure deployment. They do not measure reliability. And reliability – the ability of an AI system to perform consistently, explain its decisions, withstand regulatory scrutiny, and operate without degrading under real-world conditions – is precisely where the gap is widening.

Consider the pattern that has become familiar across the industry: an institution deploys an AI model. It performs well in the testing environment. It clears the governance gates. It goes to production. And somewhere between the third and the twelfth month in production, something shifts. Model performance drifts. A data pipeline changes upstream. A new customer segment enters the population the model was trained on. The outputs become unreliable – not dramatically, not suddenly, but incrementally and quietly, until the institution is looking at a customer complaint, a regulatory inquiry, or a forced rollback.

This is not a story about AI failing. It is a story about trusted AI being treated as an outcome of deployment rather than an engineering discipline applied before, during, and continuously after it.

What Trusted AI in Banking Actually Means

The phrase ‘trusted AI’ carries significant risk of becoming a marketing abstraction. It needs a precise, operational definition.

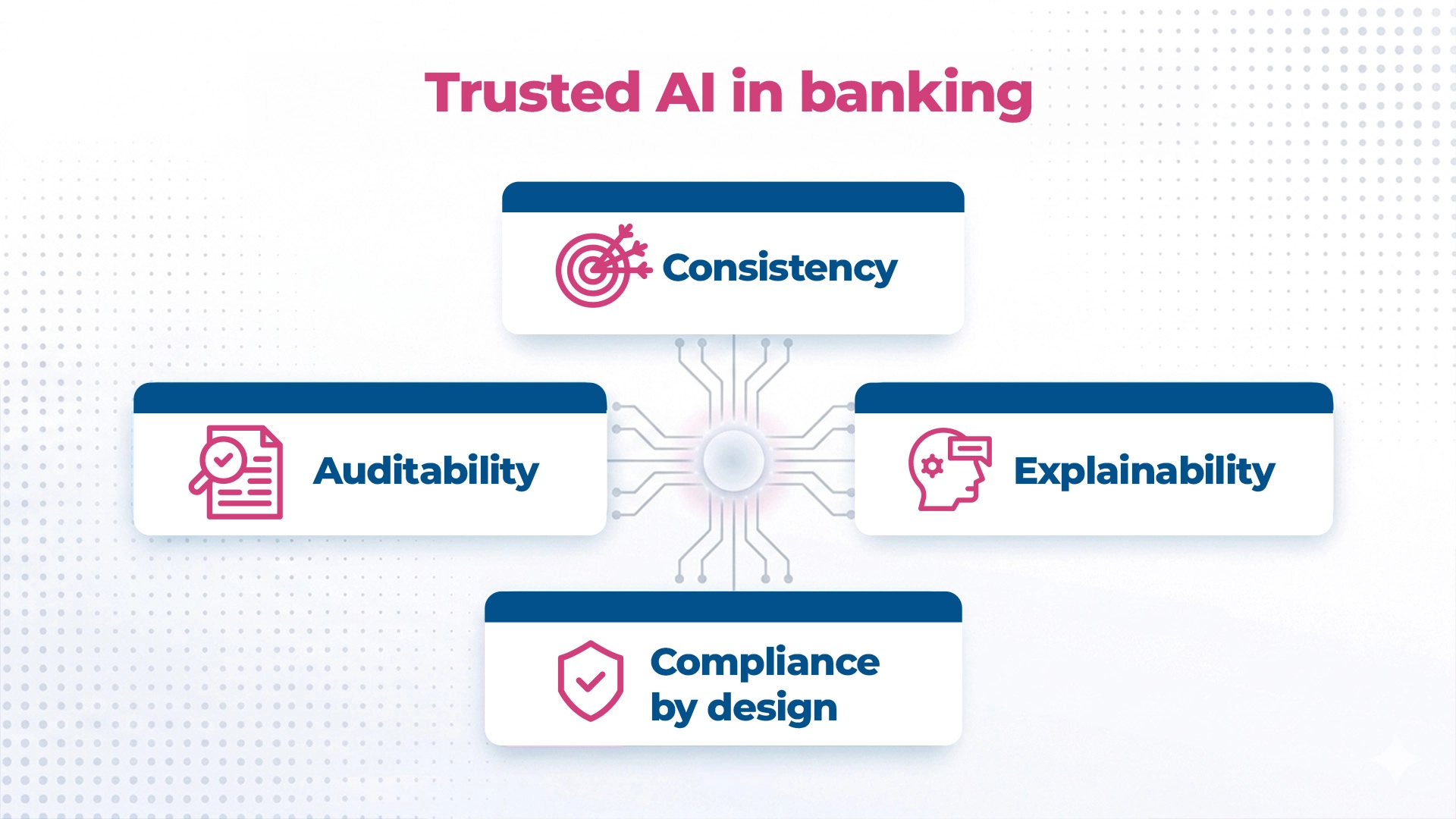

Trusted AI in banking is not a property of a model. It is a property of a system – one that can demonstrate four capabilities simultaneously, under real-world conditions, at production scale:

Consistency

The system produces reliable outcomes across environments, data conditions, customer segments, and time. The credit model that performs well on Tuesday should perform equivalently on Thursday. Consistency is not assumed; it is engineered and continuously validated.

Explainability

When a decision is questioned – by a customer who was denied a loan, by a regulator reviewing adverse action practices, by an auditor examining model governance – the system can provide a coherent, defensible account of how that specific outcome was reached. Not a general description of how the model works. A specific, traceable explanation of this decision, for this customer, at this moment.

The US Consumer Financial Protection Bureau has been explicit: the complexity of an algorithm does not exempt a lender from its obligation to provide specific reasons for adverse credit decisions. Explainability is not a technical nicety. It is a legal requirement.

Compliance by Design

Regulatory frameworks governing AI in banking are not static. SR 11-7 on model risk management, BCBS 239 on risk data aggregation, the EU AI Act’s requirements for high-risk AI systems, GDPR’s constraints on automated decision-making – all place obligations on institutions that go well beyond deploying a model. Trusted AI systems are built with these obligations embedded in their architecture, not retrofitted after a regulatory examination identifies the gap.

The BCBS 239 data point is instructive: these risk data aggregation principles have been in place since 2013, more than a decade. As of 2024, fewer than 30% of Tier-1 banks report full compliance. The AI era has not solved this foundational data governance problem. It has amplified it.

Auditability

Every decision an AI system makes must be traceable – from the input data that informed it, through the model logic that processed it, to the output that was acted upon. Auditability means that when something goes wrong, the institution can reconstruct exactly what happened, identify where the failure originated, and demonstrate to regulators and stakeholders that it was identified, contained, and corrected.

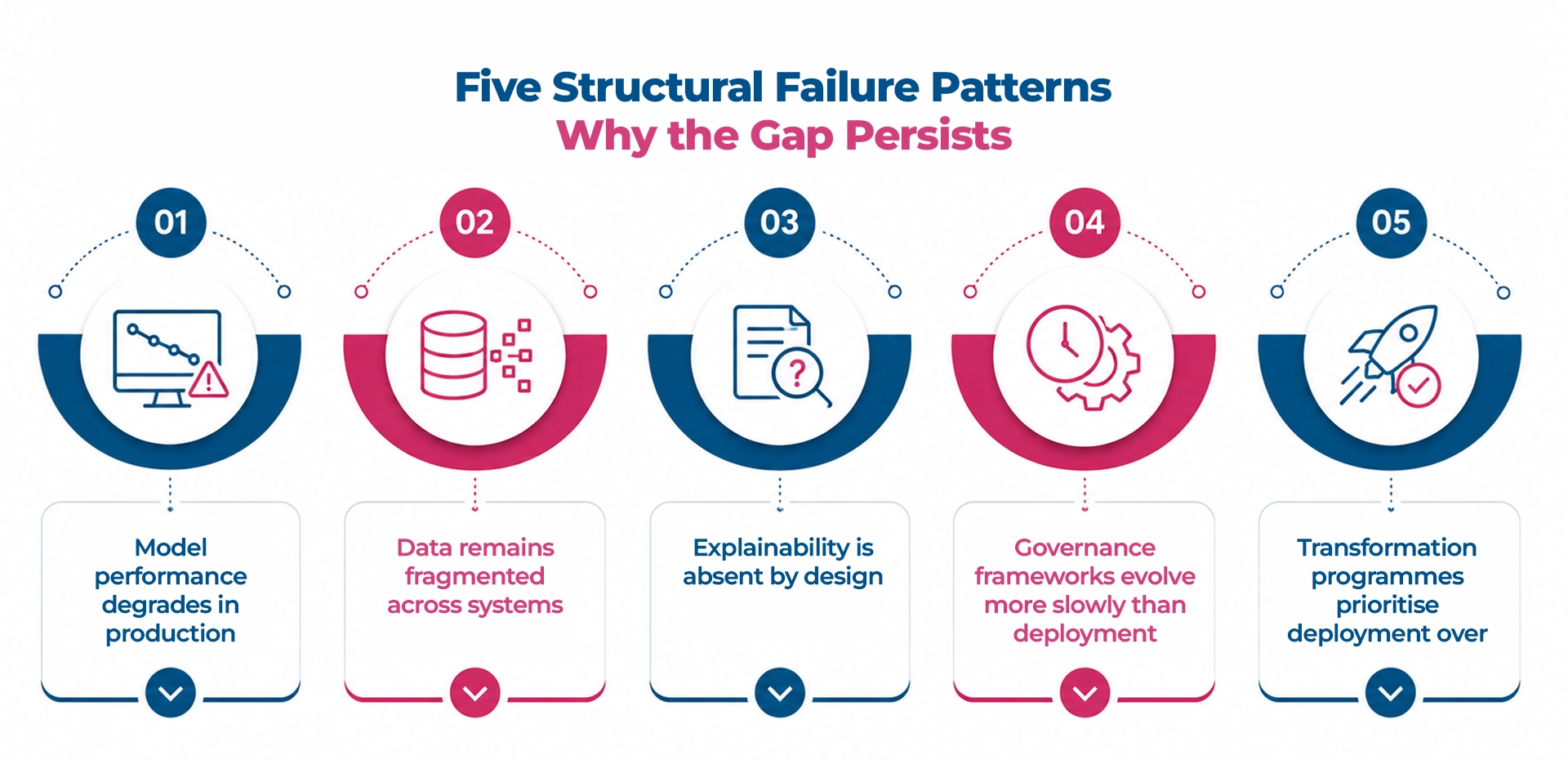

Five Structural Failure Patterns | Why the Gap Persists

The transition from pilot success to enterprise reliability is where most AI transformation programmes in banking stall. Five patterns account for the majority of the gap:

- Model performance degrades in production: test accuracy of 95% is not production accuracy. Environments diverge. Training distributions are not production distributions.

- Data remains fragmented across systems: banking data lives across core banking platforms, CRM, fraud systems, digital channels, and third-party providers. Each with different schemas, update frequencies, and governance standards.

- Explainability is absent by design: models using gradient boosting, deep learning, or LLMs produce outputs through processes that are architecturally opaque. Explainability was not built in because it was not treated as a design requirement.

- Governance frameworks evolve more slowly than deployment: processes designed for model changes measured in months cannot govern AI systems that adapt continuously.

- Transformation programmes prioritise deployment over validation: KPIs measure go-lives, automation rates, and cost reduction. Almost none measure production reliability at month 3, 6, or 12.

The Mandate Shift for Banking Technology Leaders

The question that drove digital transformation in banking for the last decade: ‘How do we deploy faster?’

The question that defines AI-first banking leadership for the next decade: ‘How do we ensure that what we deploy can be trusted – consistently, at scale, under the scrutiny of regulators, customers, and the market?’

This is not a retreat from speed. It is a redefinition of what speed means. In AI-first banking transformation, speed must be measured by confident deployment frequency – the rate at which an institution can release AI-driven changes that it has genuine reason to trust.

Trust is not a constraint on AI transformation in banking. It is the engineering foundation that makes transformation possible – and the competitive advantage that separates those who scale from those who stall.

This article is part of the Engineering Trust in AI-First Banking series.

Read: Complete Framework Overview

Download full research report that examines every dimension of trusted AI in banking

What To Read Next

PREVIOUS: Banking Has Entered the AI-First Era – the structural shift and three new complexity types

NEXT: Speed Without Trust Creates Risk – the four execution failure patterns with institutional evidence and the trust layer architecture

FAQ

1. What is the difference between AI adoption and trusted AI in banking?

AI adoption means having models in production — use cases activated, automation rates growing, deployment milestones met. Trusted AI means those models produce consistent, explainable, compliant, and auditable outcomes over time, under regulatory scrutiny, at production scale. Most institutions have achieved adoption. Very few have achieved trust — and the gap between the two is where AI programmes fail in practice.

2. Why do banks with AI in production still experience model failures and regulatory findings?

Because production deployment and production reliability are not the same thing. Models that pass testing enter environments that diverge from training conditions over time – data distributions shift, edge cases multiply, feedback loops change. Without continuous validation infrastructure, this drift is invisible until it becomes a production incident or a regulatory finding. Deployment is the starting point; sustained confidence requires ongoing monitoring, not a one-time go-live gate.

3. What are the five failure patterns that prevent AI adoption from becoming trusted AI?

The five patterns are: model performance that does not survive the transition from test to production; data inconsistency across systems that corrupts AI inputs; the absence of explainability infrastructure that makes decisions undefendable; governance frameworks calibrated for monthly reviews that cannot keep pace with weekly AI deployment cycles; and measurement frameworks that track deployment speed but not production reliability over time.

4. How should a bank measure whether its AI is genuinely trusted, not just deployed?

Trusted AI is measured not by the absence of incidents but by the presence of a system that detects, contains, and accounts for them before they become consequential. Practical indicators include: the ability to produce a full audit trail for any AI-driven decision on regulatory demand; continuous monitoring that detects model drift before it affects outcomes; and data quality validated at the point of model input rather than assumed from source system reports.

5. Why is the shift from AI adoption to trusted AI described as a mandate reframe rather than a technology upgrade?

Because the core problem is not the technology – it is what the institution is measuring and optimising for. Organisations that treat trusted AI in banking as a technology upgrade continue investing in capability. Organisations that reframe it as a mandate recognise that the infrastructure beneath the capability – data integrity, continuous validation, explainability, integrated governance – is not optional overhead. It is the load-bearing condition that determines whether capability delivers value or accumulates risk.