AI-enabled core banking modernization is the shift from systems of record to systems of intelligence: banking cores that can generate customer- and transaction-specific data access, validation logic, and decisioning on demand, instead of relying only on predefined services and reports. For CIOs at regional and community banks, the conventional modernization narrative, moving from batch processing to real-time, event-driven architecture, is accurate, but it describes the plumbing. It doesn’t describe what that plumbing is actually for.

The Real Shift: From Predefined Services to Context-Specific Intelligence

Digital-era architecture gave banks service-oriented systems and, later, microservices. Both were genuine advances, decomposing monolithic cores into reusable units. But both had a ceiling: a service was built for a defined purpose and served every consumer identically. If a specific customer or transaction needed something the service wasn’t designed for, the answer was always the same: build a new service.

AI dissolves that ceiling. Through agentic context assembly, an AI-enabled core can dynamically construct a data request specific to one customer, one transaction, one moment, pulling from multiple sources, combining structured and unstructured data, and returning exactly what a decision requires, without pre-engineering a new service or report.

For a lending decision, that means the AI doesn’t retrieve a generic customer profile. It assembles a context built from repayment history, current account behavior, the content of the customer’s last interaction, and unstructured signals from uploaded documents, synthesized specifically for that decision. That’s a different level of granularity than anything digital-first architecture could deliver.

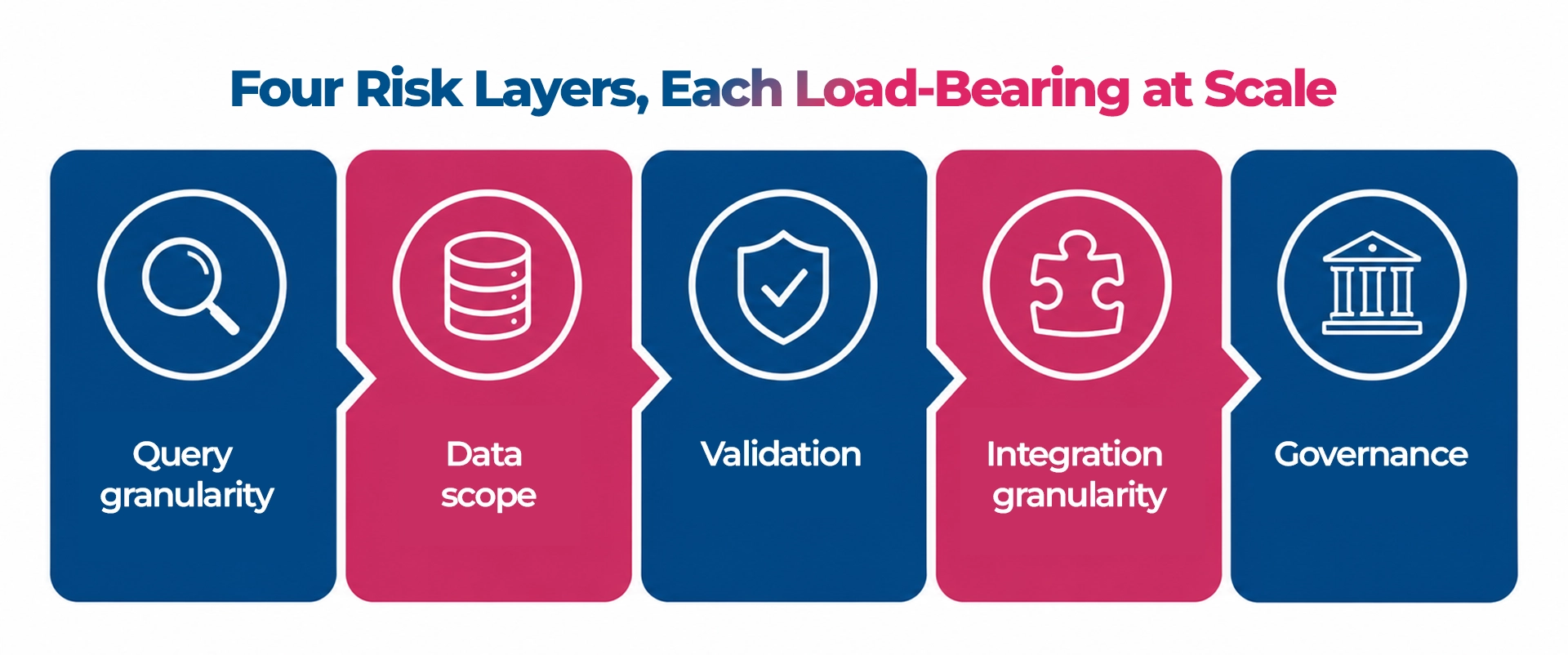

What Actually Changes at Every Layer of the Core

The shift from digital-first to AI-first isn’t limited to one layer of the architecture; it touches query granularity, data scope, validation, integration, and governance simultaneously:

- Query granularity moves from service-level constructs predefined for a period, product, or segment, to context-specific queries generated dynamically for a specific customer, transaction, or moment.

- Data scope expands from structured data queryable only by date, value, and column name, to structured and unstructured data queryable by content, meaning, and pattern.

- Validation moves from predefined, aggregated rules embedded in the data mart and applied uniformly across segments, to context-specific, pattern-enhanced validations generated on the fly for the individual customer or transaction.

- Integration granularity moves from reusable, standardized service-level APIs to customer- and transaction-level intelligence generated on demand for the specific decision at hand.

- Governance moves from API version control at the service level, with lineage established at the document or code level, to intelligence-layer governance, with lineage granularized down to the paragraph and sentence level.

None of these shifts happens automatically as a side effect of moving to real-time infrastructure. Each has to be deliberately architected, which is precisely why “faster plumbing” is an incomplete modernization objective.

Unstructured Data Becomes Part of the Decision Surface

Pre-AI, banking systems could only query structured fields: columns, values, dates. The narrative inside a transaction description, the explanation behind a manual override, the content of a compliance note: all invisible to any model, no matter how sophisticated the digital core around it.

AI-enabled core banking makes the content of those fields queryable, not just the fields themselves. In AML transaction monitoring, this is often where the highest-value gains show up: reasoning over transaction narratives alongside values and counterparty data can materially reduce false-positive escalation rates, because the model can finally read the transaction instead of just pattern-matching against it. In credit risk assessment, the same principle lets a model process the text of a customer’s complaint history alongside their numerical credit metrics, surfacing patterns that structured fields alone can never capture.

Query-Level Validation: Solving the BCBS 239 Compliance Gap Without a Data Mart Rebuild

More than a decade after BCBS 239 established risk data aggregation principles, fewer than 30% of Tier-1 banks report full compliance, and the gap is rarely a data quality problem. It’s a validation architecture problem. In the predefined report model, adding or removing a validation rule requires re-engineering the data mart itself: a data engineering project, not a configuration change.

AI-enabled cores move validation logic out of the data mart and into the query layer, which changes three things for the CIO’s regulatory obligations:

- New validations deploy without a data mart rebuild. A new BCBS 239 requirement or examination finding becomes a rule in the intelligence layer, not a re-engineering project.

- The system reports what it can’t validate, not just what passed or failed. For the first time, governance has full visibility into the validation coverage gap.

- Validation failures become a learning loop. Patterns in failed validations surface data quality issues and incorrect specifications for human review, so governance becomes continuous, not a periodic audit cycle.

Why This Matters Most for Real-Time Lending, Deposits, and Payments

Query-level validation has a direct bearing on how much a bank can trust its real-time, semi-autonomous decisioning engines. Two lending systems can post identical benchmark accuracy and still have very different reliability profiles. The difference shows up at the edge: the transaction outside the predefined validation rules, the customer profile with an anomaly the data mart never anticipated, the regulatory requirement updated after the last release.

In the predefined model, those edge cases pass silently, either generating an incorrect decision or triggering exactly the kind of manual review the semi-autonomous system was built to eliminate. In an AI-enabled core with query-level validation, they surface, flagged, contextualized, and routed for the right response, in real time, at the transaction level. The same principle applies to deposits and payments: real-time payment systems operating without query-level validation carry the risk of processing a transaction against a data state with an undetected inconsistency, such as an account status that hasn’t updated or a sanction flag added after the last batch cycle. Query-level validation closes that gap without requiring every upstream system to have already resolved the inconsistency.

Governance Has to Move With the Logic

In service-oriented architecture, governance lived at the API and service level. In an AI-first core, decision logic has moved into the intelligence layer: the prompts, context specifications, validation rules, and agentic workflows that now carry the weight the service definition used to carry. Governing the API layer while leaving prompts and context specifications ungoverned means governing the pipes while leaving the actual decision logic unaccountable, precisely what a regulatory examination is built to find. This obligation extends to agentic workflow governance and exception management: when AI agents orchestrate multi-step decisions, the institution has to be able to account for what the agent did, in what sequence, with what data, and route anything it couldn’t resolve for human review.

What This Means for the CIO Agenda

The most consequential modernization question isn’t “how do we move from batch to real-time?” It’s how do we move from predefined constructs to context-specific intelligence, and govern the intelligence layer that makes it possible?

The CIO’s Guide to AI-Enabled Core Banking Modernization maps the three battlegrounds, context-specific intelligence, unstructured data as a decision surface, and intelligence-layer governance, into a four-directive playbook for banking CIOs.

FAQ

1) What is AI-enabled core banking modernization?

It’s the process of embedding AI directly into a bank’s core systems, moving from systems of record that execute predefined rules to systems of intelligence that generate customer- and transaction-specific data access, validation, and decisions on demand.

2) How is this different from moving to real-time, event-driven architecture?

Real-time architecture changes how fast data moves. AI-enabled core modernization changes what the system can reason about, enabling context-specific intelligence, unstructured data access, and validation logic generated at query time rather than pre-built into a data mart or report.

3) Does AI-enabled core banking require rebuilding the data mart?

No. AI-generated, query-level validation is applied at the point of data retrieval, on top of the existing data mart, without altering its structure. This is what allows new regulatory validations to be operationalized in days rather than months.

4) Why does BCBS 239 compliance remain so low across Tier-1 and regional banks?

Because the predefined report model can’t accommodate an evolving regulatory standard without continuous re-engineering. The gap is a validation architecture problem, not primarily a data quality problem, and it’s solvable with query-level validation intelligence.

5) What is “intelligence layer governance”?

It’s the governance framework, including version control, lineage tracking, exception management, and audit capability, applied to the prompts, context specifications, and validation rules that now carry decision logic in an AI-first core, down to the paragraph and sentence level of the source documents that inform them.