Innovations in Retail Banking Services: Fintech Collaborations and Open Banking Initiatives

The retail banking industry is profoundly transforming, driven by technological advancements, and changing customer expectations. Fintech collaborations and open banking initiatives have emerged as powerful catalysts for InnovationInnovation in retail banking services. In this blog post, we will explore the exciting innovations that arise from fintech collaborations and open banking, highlighting their benefits and impact on the customer experience. Working with partners like Maveric brings an undeniable edge to leading FIs to sharpen their growth strategies and up their product innovation pipeline.

1. Fintech Collaborations: Fueling Innovation and Customer-Centric Solutions

Fintech companies, known for their agility and technological expertise, are partnering with traditional banks to revolutionize the retail banking landscape. Here’s how fintech collaborations are driving InnovationInnovation:

- Enhanced Customer Experience: Fintech collaborations bring customer-centric solutions that simplify banking processes and offer personalized experiences. From intuitive mobile banking apps to budgeting tools and automated investment platforms, customers benefit from innovative services designed to meet their needs.

- Advanced Digital Payments: Collaboration with Fintechs enables banks to offer seamless and secure digital payment solutions. Peer-to-peer payments, mobile wallets, and contactless payment options transform how customers transact, providing convenience, speed, and improved security.

- Improved Access to Credit: Fintech collaborations have developed alternative credit scoring models, leveraging non-traditional data sources such as transaction history and social media profiles. This allows banks to extend credit to underserved populations and make informed lending decisions beyond traditional credit scores.

- Robo-Advisory and Wealth Management: Through fintech collaborations, banks can offer robo-advisory services, combining algorithms and machine learning to provide automated investment advice and portfolio management. This technology-driven approach democratizes wealth management, making it accessible to a broader range of customers.

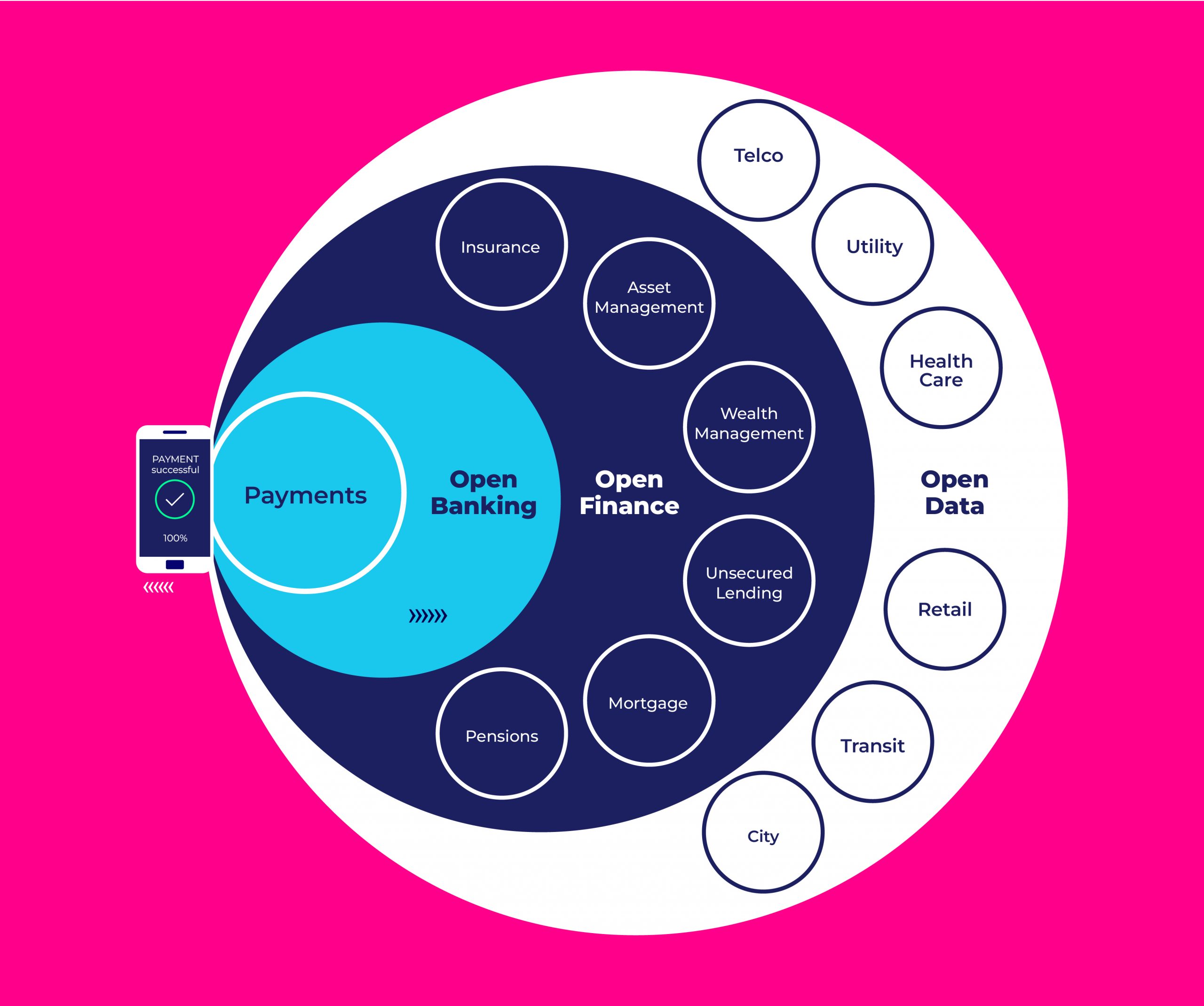

2. Open Banking Initiatives: Empowering Customers and Encouraging Innovation

Innovation

Directed by regulatory mandates and industry collaboration, open banking initiatives are reshaping the retail banking landscape. Here’s how open banking is fostering InnovationInnovation:

- Customer Data Empowerment: Open banking allows customers to securely share their financial data with trusted third-party providers through APIs. This empowers customers to access personalized financial services, such as account aggregation, budgeting tools, and loan comparison platforms, all within a single interface.

- Collaborative Ecosystems: Open banking encourages collaboration between banks, fintechs, and other service providers. This collaborative ecosystem fosters InnovationInnovation, enabling banks to leverage fintech expertise and offer a wider range of products and services. For example, banks can integrate loan origination platforms or digital identity verification services through API integrations.

- Personalized Financial Management: Open banking provides customers comprehensive financial insights by aggregating data from multiple accounts and sources. Personal finance management apps can analyze spending patterns, offer budgeting recommendations, and provide a holistic view of customers’ financial health.

- Seamless Payments and Account Integration: Open banking allows customers to initiate payments and transfers directly from their bank accounts through third-party applications. This eliminates manual data entry and offers a seamless, streamlined payment experience.

Conclusion:

Fintech collaborations and open banking initiatives are revolutionizing retail banking services, empowering customers, and driving InnovationInnovation. Through partnerships with fintech companies, traditional banks can tap into these innovative startups’ agility, technological prowess, and customer-centricity. Open banking initiatives enhance customer experience by enabling secure data sharing, personalized financial management, and seamless integrations with third-party services.

As the retail banking industry evolves, embracing fintech collaborations and open banking initiatives becomes crucial for banks aiming to stay competitive. By fostering partnerships and leveraging open APIs, banks can unlock a world of innovative solutions, elevate the customer experience, and create a more inclusive and customer-centric banking ecosystem.

About Maveric Systems

Starting in 2000, Maveric Systems is a niche, domain-led Banking Tech specialist partnering with global banks to solve business challenges through emerging technology. 3000+ tech experts use proven frameworks to empower our customers to navigate a rapidly changing environment, enabling sharper definitions of their goals and measures to achieve them.

Across retail, corporate & wealth management, Maveric accelerates digital transformation through native banking domain expertise, a customer-intimacy-led delivery model, and a vibrant leadership supported by a culture of ownership.

With centers of excellence for Data, Digital, Core Banking, and Quality Engineering, Maveric teams work in 15 countries with regional delivery capabilities in Bangalore, Chennai, Dubai, London, Poland, Riyadh, and Singapore.

View