Four execution failure patterns repeat across banking institutions of every tier and every market – release velocity without validation, data fragmentation, model opacity, and disconnected transformation layers. This article diagnoses each with institutional evidence including a £12M remediation case, and presents the trust layer as a named architectural system with four capabilities and an explicit C-suite ownership map.

Why This Article Matters

This is where the argument moves from strategic framing to operational diagnosis. The four execution failure patterns described here are not hypothetical, they are documented, repeating patterns visible across institutions of every tier and every market. More importantly, this article presents the trust layer not as an abstract principle but as a named architectural system with four specific capabilities and an explicit ownership map: who is accountable for each layer, at the C-suite level, and how they coordinate. If you are accountable for AI transformation delivery, this is the article that turns the problem into something you can actually build a solution for.

The Execution Confidence Gap

Every bank has an AI strategy. Most have AI in production. Many have invested at a scale that would have been unimaginable five years ago.

And yet, across the industry, a pattern emerges with enough consistency that it can no longer be attributed to individual institutional failure, poor vendor selection, or insufficient ambition.

Banks are moving fast but not reliably. They are deploying AI but not trusting it. They are transforming systems but losing control of outcomes. The cost of that gap accumulates across remediation programmes, regulatory interventions, emergency rollbacks, and the quiet erosion of internal confidence in AI-driven decisioning.

This is not a technology gap. It is an execution confidence gap – the inability to build, deploy, and operate AI systems in a way that generates genuine, sustained, evidence-based confidence in the systems themselves, in the decisions they produce, and in the institution’s ability to account for both.

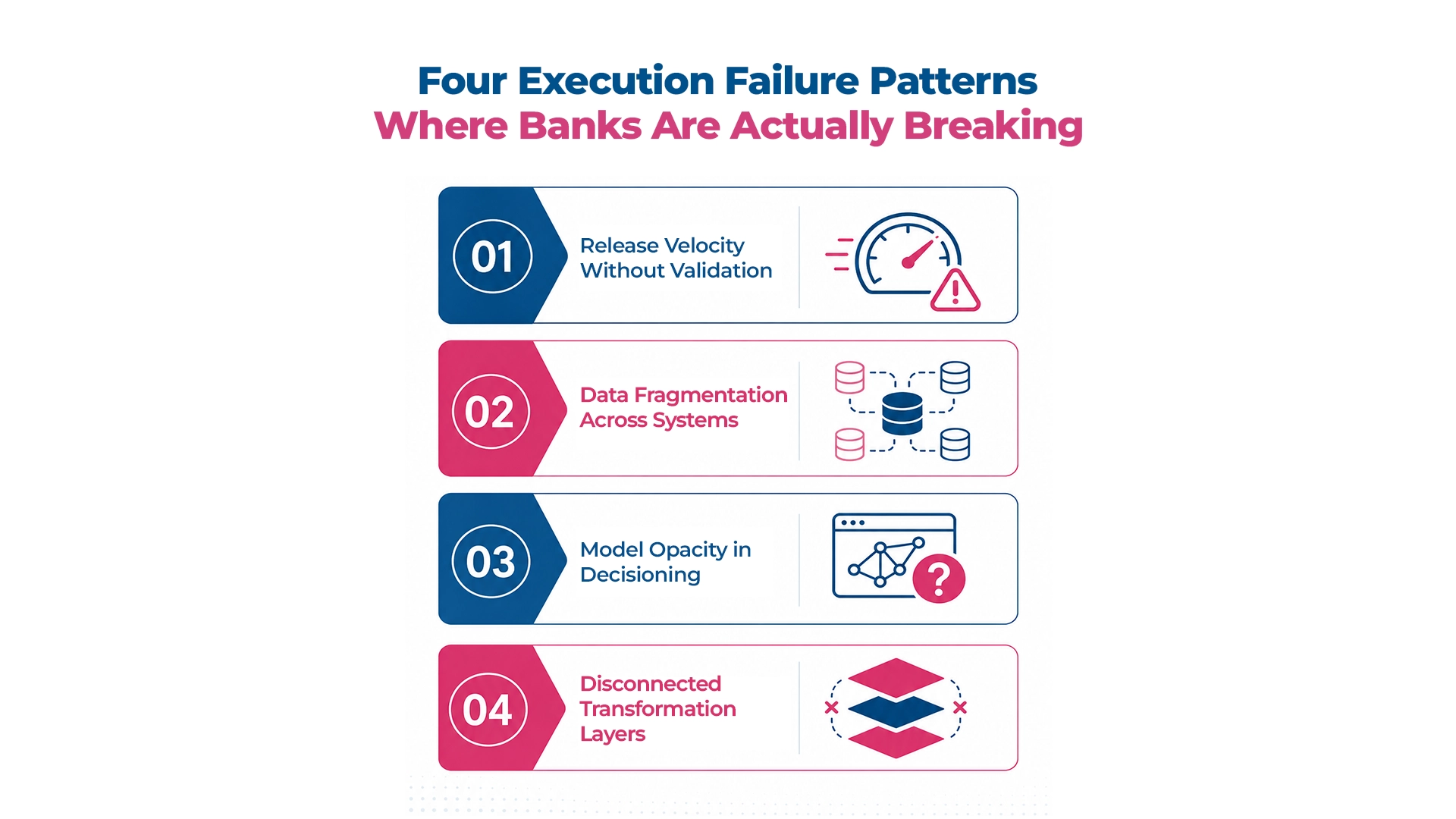

Four Execution Failure Patterns, Where Banks Are Actually Breaking

The failure manifests in four patterns that repeat across institutions, tiers, and geographies with striking consistency.

Pattern 1: Release Velocity Without Validation

Banks are pushing faster release cycles to stay competitive. What has not shortened at the same rate is the governance infrastructure required to catch what goes wrong, before it reaches customers.

In AI-driven systems, defects are different in character from traditional software defects. They are often not visible at the point of release. They emerge over time, as the model encounters data conditions it was not trained on, as the production environment diverges from the test environment, as edge cases accumulate into a pattern of unreliable output.

EVIDENCE

A major European retail bank discovered a loan pricing defect that had been live in production for six weeks across 40,000 applications. The defect originated in a data transformation layer that passed automated testing but had not been validated against business logic. Remediation cost: over £12 million. The engineering fix, had it been caught pre-production: two days.

Pattern 2: Data Fragmentation Across Systems

Banking data does not exist in a governed, unified, real-time state. It exists across legacy core banking platforms running on batch cycles, CRM systems updated at varying frequencies, fraud and payments infrastructure with their own schemas, digital channel event streams, and third-party data providers with independent update cadences.

An AI model trained on this landscape is trained on a version of reality. When it is deployed into production, it encounters a different version, one that is slightly, or sometimes substantially, different from what the training data represented.

EVIDENCE

BCBS 239 risk data aggregation principles have been in place since 2013, more than a decade. As of 2024, fewer than 30% of Tier-1 banks report full compliance. Every model deployed in production is a new and demanding consumer of the same fragmented, inconsistently governed data estate that BCBS 239 was designed to correct.

Pattern 3: Model Opacity in Decisioning

In a deterministic system, every decision has an auditable logic path. In a probabilistic system, decisions emerge from patterns across millions of parameters – patterns that can be characterised, but not always traced to a specific, communicable rationale.

In banking, where credit decisions affect individuals’ financial lives, where fraud determinations have direct customer impact, and where regulatory frameworks carry explicit requirements for decision justification, this is a structural liability.

EVIDENCE

The US Consumer Financial Protection Bureau has stated explicitly that the complexity of an algorithm does not exempt a lender from the obligation to provide specific, accurate reasons for adverse credit actions. Enforcement actions have followed, not because the models produced incorrect outcomes, but because the institutions could not explain why the outcomes were correct.

Pattern 4: Disconnected Transformation Layers

AI transformation requires three capabilities to evolve together: engineering velocity, data reliability, and compliance assurance. In most institutions, they evolve separately – under different senior leadership, with different definitions of success, responding to different internal and external pressures, and operating at different speeds.

Engineering teams are measured on deployment frequency. Data teams on model accuracy. Compliance teams on risk avoidance. These objectives are not inherently conflicting, but when pursued in silos, they produce conflicting outcomes. A model that passes engineering and data gates can fail compliance review. And by the time that failure is discovered, the cost of resolution is a multiple of what early integration would have required.

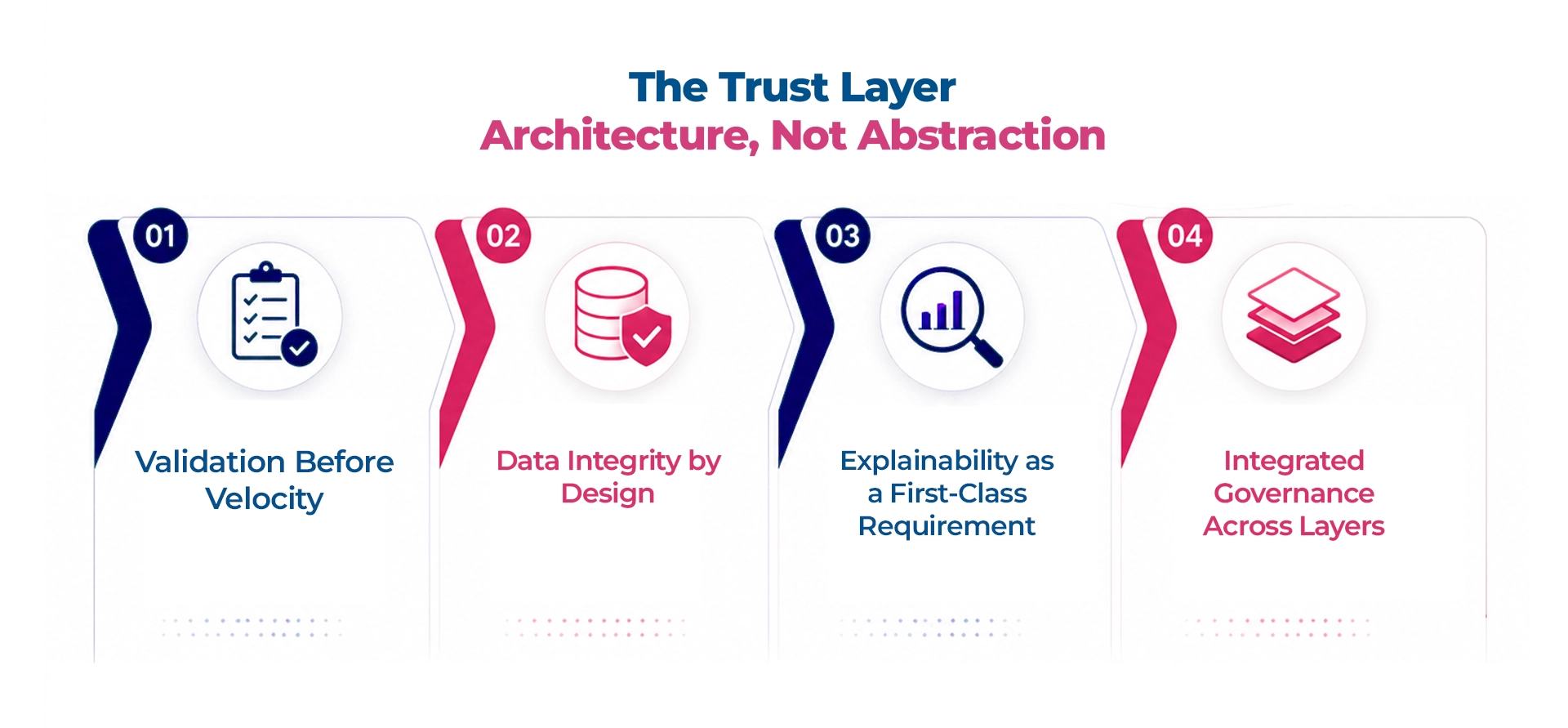

The Trust Layer: Architecture, Not Abstraction

Most frameworks that address this problem stay at the level of principle. The trust layer in AI-first banking is not a metaphor or a set of aspirations. It is a specific architectural requirement with a defined anatomy, clear ownership, and measurable outcomes. It comprises four integrated capabilities:

Capability 1: Validation Before Velocity

Continuous quality intelligence embedded directly into the CI/CD pipeline, not as a periodic gate, but as a persistent, always-on signal that validates model behaviour, detects data anomalies, and catches business logic failures before they reach production.

Owner: The CTO and Head of Engineering, with shared accountability from the Head of Quality Engineering. This is a software engineering discipline, not a compliance function and must be resourced and measured as one.

Capability 2: Data Integrity by Design

Data lineage enforcement, consistency monitoring, and real-time quality validation built into the data architecture from the point of design. The practical expression: the data contract – a defined, monitored, enforced specification of what every model in production expects from its data inputs. A model without a data contract is a model operating on assumptions. In production, assumptions degrade.

Owner: The Chief Data Officer, with joint accountability from the data engineering function and the model risk management team.

Capability 3: Explainability as a First-Class Requirement

Explainability is not a reporting feature added at the end of model development. It is an architectural decision made at the point of model design – determining which decisions require human-interpretable logic, which require post-hoc explanation infrastructure, and which require a full, reconstructable audit trail that can be produced on regulatory demand.

Owner: The Chief Risk Officer and the Head of Model Risk Management, in partnership with the data science teams that design the models.

Capability 4: Integrated Governance Across Layers

Engineering, data, and compliance operating within a shared execution model with common definitions of what ‘production-ready’ means, aligned risk thresholds that apply across all three functions, and cross-functional accountability at the level of individual models and releases.

Owner: The CIO, as the executive who sits at the intersection of the CTO’s delivery mandate, the CDO’s data mandate, and the CRO’s risk mandate.

What Changes When the Trust Layer Is Built

The objection that building this architecture will slow delivery is empirically wrong. Institutions that have embedded continuous quality validation into their AI delivery pipelines report 40 to 60 percent reductions in production incidents. More significantly, they report structural improvement in deployment confidence, the ability to release with genuine, evidence-based assurance rather than hopeful assumption.

Without a trust layer, complexity accumulates debt. Every model added to the production estate is a new source of potential failure. The system becomes progressively more fragile as it scales – and the weight of that fragility eventually becomes the ceiling on the institution’s transformation ambition.

With a trust layer, complexity compounds confidence. Each validated release builds the institutional evidence base for the next. Each clean data contract reduces the surface area of downstream risk.

The banks that win the next decade will not be those who adopted AI first. They will be those who made it trustworthy in production, under pressure, at scale.

Ready to go deeper on the trust layer architecture – who owns each pillar, what it requires technically, and what it looks like in practice? The companion deep-dive examines each capability in full implementation detail.

Deep Dive: Engineering Trust in AI-First Banking – The Architecture CIOs Actually Need

This article is part of the Engineering Trust in AI-First Banking series, examining the framework that separates institutions that scale AI from those that stall.

What to Read Next

PREVIOUS: The Real Shift: From AI Adoption to Trusted AI

FAQ

1. Why does deploying AI fast without trust infrastructure create risk in banking specifically?

In banking, AI-driven decisions carry the same regulatory, customer, and financial obligations as human decisions – but at a volume and velocity that makes retrospective correction structurally impossible. A fraud model generating false positives at scale is not just a technical problem: it is a customer harm event, a regulatory exposure, and an operational overhead simultaneously. Speed without the validation and governance infrastructure to sustain it amplifies risk at the speed of deployment.

2. What are the four execution failure patterns that cause AI transformation to break down?

The four patterns are: velocity without validation (deploying faster than monitoring infrastructure can cover); data dependency without data governance (assuming input quality that does not exist); explainability treated as a post-deployment problem rather than an architectural requirement; and governance designed for periodic review applied to systems that release continuously. Each pattern is individually addressable – but they typically appear together, compounding into systemic execution failure.

3. How does model drift silently undermine AI performance in production banking environments?

Model drift occurs when the real-world data a deployed model encounters begins to diverge from the data it was trained on – due to seasonal patterns, market conditions, customer behaviour shifts, or upstream system changes. Unlike a system outage, drift is invisible to standard monitoring: the model continues running and producing outputs, but accuracy degrades without triggering an alert. In credit decisioning or fraud detection, even modest drift translates directly into miscalibrated risk assessments.

4. Can banks achieve both speed and trust, or is there an inherent trade-off?

Speed and trust are not opposites – but they require different sequencing. Institutions that build trust infrastructure early (continuous validation, data contracts, governance embedded in the delivery pipeline) find that speed increases sustainably over time, because each release is made with evidence-based confidence rather than hopeful assumption. The apparent trade-off exists only when trust infrastructure is treated as a constraint on speed rather than the foundation that makes sustained speed possible.

5. What does a data contract mean in the context of AI-first banking, and why does it matter?

A data contract is a defined, monitored, and enforced specification of what a production AI model expects from its inputs – schema, quality thresholds, latency, completeness. In a banking environment where data lives across six or more systems with different standards and update cycles, data contracts are the mechanism that prevents input inconsistency from silently corrupting model outputs. Without them, data quality is assumed; with them, it is verified continuously at the point of model consumption.