In the history of technological revolutions, few periods match the dot com bubble and bust of the late 1990s and early 2000s for scale and shock. From 1995 to 2000, the internet promised to transform global commerce and communication. This optimism propelled the NASDAQ Composite from under 1,000 to a peak of 5,048.62 on March 10, 2000. The crash that followed obliterated trillions in market value, forced thousands of startups into bankruptcy, and reshaped the trajectory of digital innovation.

In 2025, artificial intelligence and especially generative AI evoke familiar patterns. Companies with limited revenue command extraordinary valuations. Hyperscaler capital expenditure has reached unprecedented levels. The narrative around AI’s potential has grown far faster than adoption. Yet AI is not a replay of the year 2000. Lessons learned across enterprises, regulators, investors and technology providers have created conditions where a correction is more likely to be managed than catastrophic. Gartner now places generative AI deep in the Trough of Disillusionment, raising a critical question.

Will the strongest AI survivors, much like Amazon after 2002,

emerge to drive a multi trillion-dollar value creation wave by 2033

The Dot Com Bust: A Collision of Hype and Reality

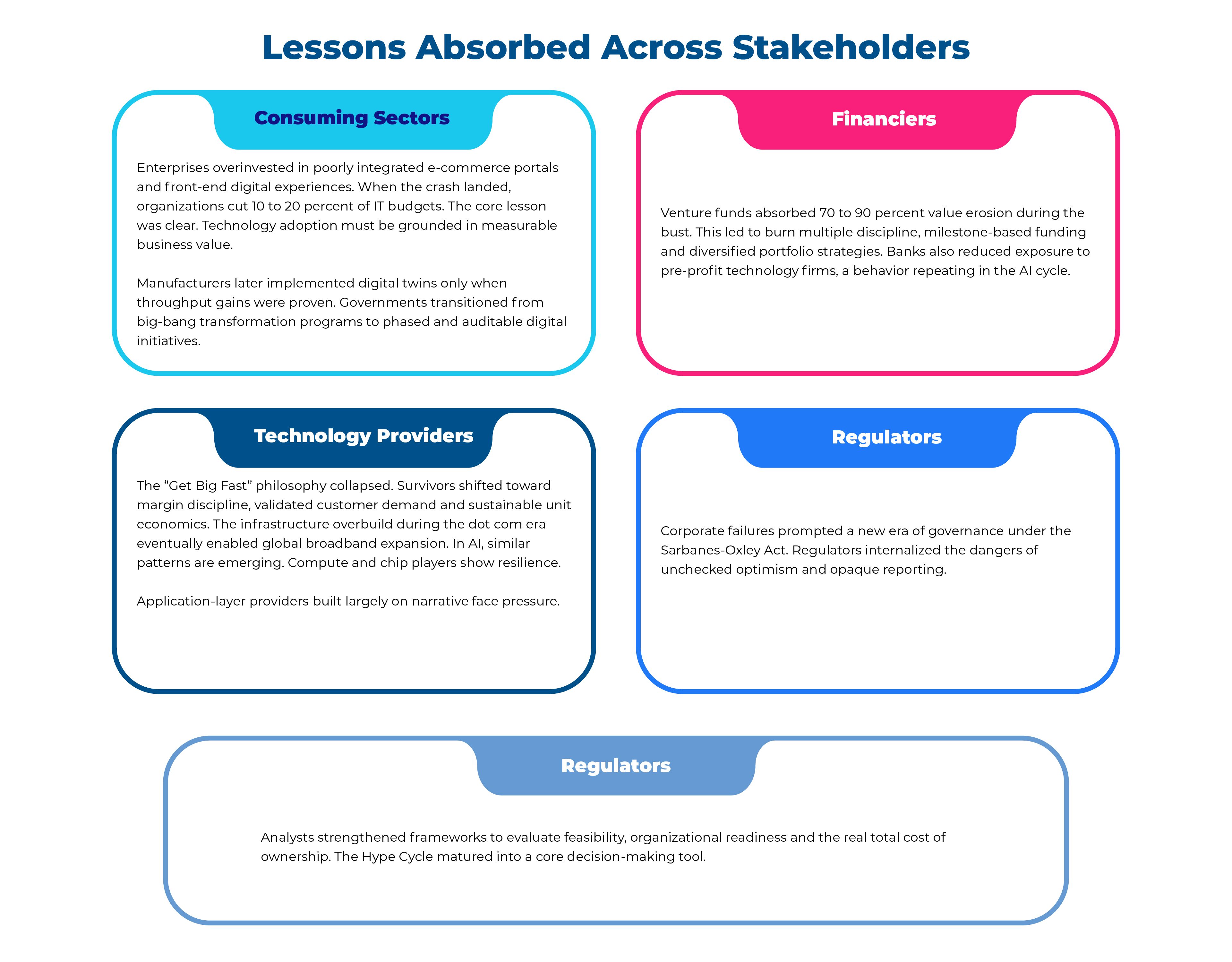

During the late 1990s, venture capital inflows grew from around $8B annually to more than $100B. Internet companies attracted nearly 40 percent of all venture funding. The year 1999 alone saw more than 900 technology IPOs. Pets.com became emblematic of the excess, launching with significant visibility despite minimal revenue.

The unraveling began in early 2000. Interest rate increases squeezed valuations. Y2K spending cycles ended overnight. Scandals, including WorldCom’s $11B accounting fraud, further weakened investor confidence. By October 2002, the NASDAQ had fallen more than 70 percent.

High-profile failures accelerated. Webvan collapsed after raising more than $800M. Boo.com burned through more than $100M in less than two years.

Yet research shows that nearly 50 percent of dot com ventures survived at least five years. Infrastructure companies like Cisco and Qualcomm rebounded strongly. Amazon recovered from a 90 percent share-price decline and eventually became a $1T company.

The deeper legacy lies in the lessons absorbed across stakeholder groups.

The AI Hype Cycle: Familiar Shadows and an Evolving Script

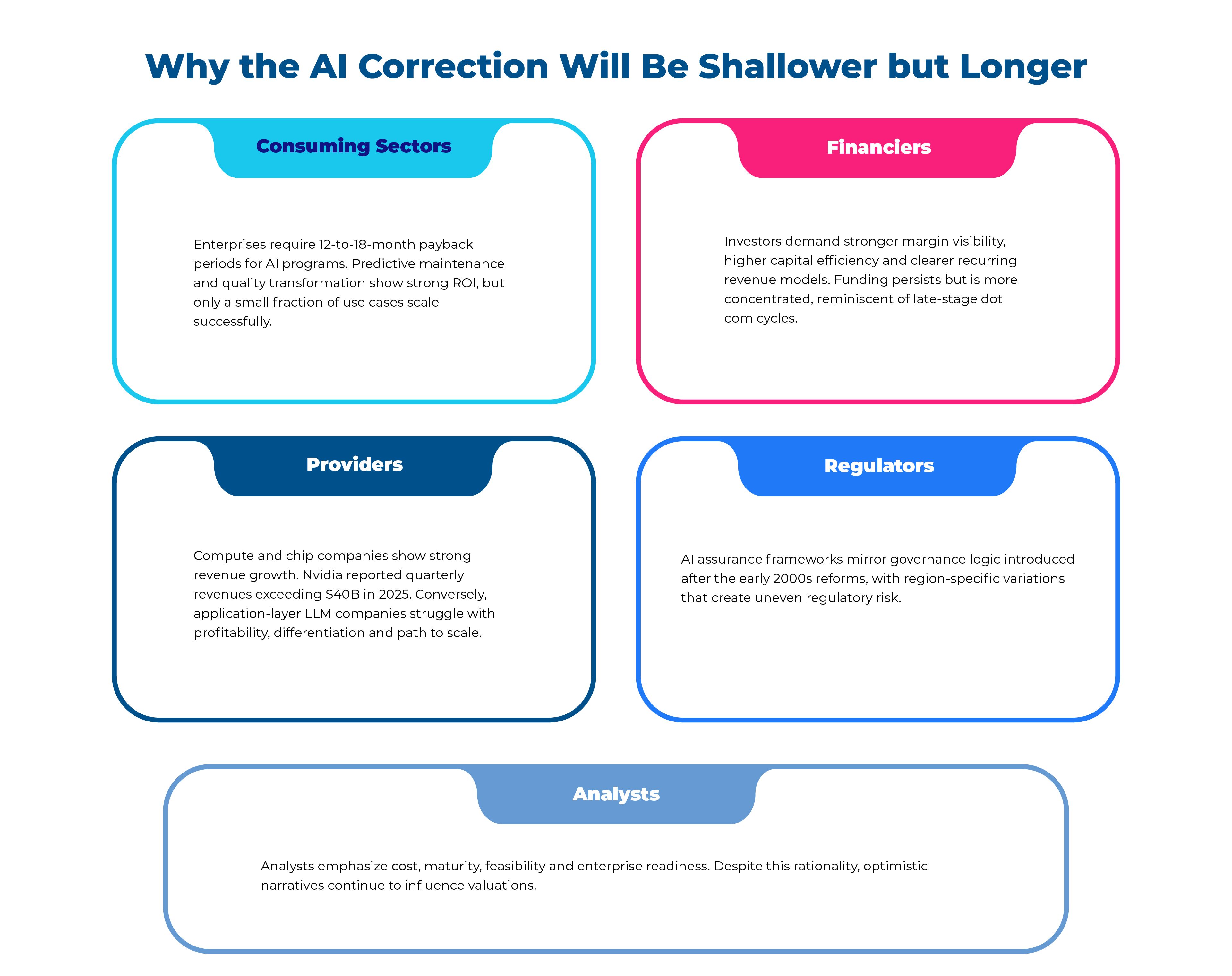

Since 2022, AI has followed a compressed version of the dot com trajectory. Generative AI breakthroughs triggered massive demand for compute. Hyperscaler capital expenditure exceeded $350B in 2025. Global AI startup funding reached nearly $90B. U.S. startup funding surpassed $200B.

By late 2025, subtle recalibration appeared among major technology firms. Not through dramatic warnings but via moderated investment ramps, refined forecasts and more cautious public positioning.

Three signals stand out.

- Circular monetization patterns where AI firms rely on hyperscalers whose revenue depends on AI adoption.

- A data center development pipeline that far exceeds near-term utilization.

- Equity markets increasingly dominated by AI-linked valuations with heightened sensitivity to sentiment shifts.

These shifts reinforce the central thesis. AI is deeply integrated into the global digital ecosystem. Any correction will likely be controlled rather than catastrophic.

The outcome is likely a 30 to 50% AI market correction.

Less severe than the dot com crash, but more prolonged due to its deep infrastructural integration

Hype in AI Categories: Survivors and Vulnerabilities

Lower Survival Categories

Frontier LLM companies face strong consolidation pressures. Autonomous code-generation tools still struggle with reliability. Pure-play AI cyber tools leak value due to heavy integration dependencies.

Higher Survival Categories

Chip manufacturers, compute platforms and data center operators show robust long-term demand. ROI-led enterprise AI applications align closely with business priorities. Scientific AI — especially in drug discovery and materials engineering — shows durable long-term potential.

Out of more than 10,000 AI startups founded since 2022, only 5 to 10 percent may reach scale by 2030.

Conclusion: Purging for Plateau

The dot com bust was not an end point. It became the foundation for the trillion-dollar digital economy that followed. AI is approaching a similar inflection. Projections estimate an $800B global AI economy by 2030 with potential GDP uplift of $15T to $20T.

A consolidation phase is inevitable. Compute providers, infrastructure players and scientifically oriented AI innovators resemble the early winners of the internet era. Pure-play LLM companies face significant risk unless they evolve quickly.

Strategic leaders should focus on measurable ROI, governance, transparency and phased scaling. The AI ecosystem will strengthen. The forest will endure, but only if the underbrush clears.

Authored by P Venkatesh – Co-Founder and Director

P Venkatesh (PV) leads the global thought leadership function aimed at shaping and promoting Maveric’s perspectives as well as expertise in the banking technology space. By building relationships with industry influencers, partners and BankTech ecosystem leaders, PV drives creation of impactful frameworks, methodologies and landscape reports that provide informed perspectives on new age technologies that shape the BankTech space.

FAQ

Is the current AI boom similar to the dot com bubble?

Yes, the AI boom shows similarities to the dot com era in terms of rapid valuations, strong investor enthusiasm, and infrastructure overbuild. However, unlike the late 1990s, enterprises, investors, and regulators today operate with greater discipline, governance maturity, and experience, reducing the likelihood of a sudden market collapse.

Will AI experience a market crash like the dot com bust?

A crash similar to the dot com bust is unlikely. Instead, the AI market is expected to undergo a controlled correction of approximately 30–50 percent, driven by capital discipline, enterprise ROI requirements, and regulatory oversight.

Why will the AI correction be less severe but more prolonged?

AI is deeply embedded in enterprise systems, cloud infrastructure, and digital ecosystems. This structural integration makes rapid unwinding difficult, resulting in a correction that unfolds gradually rather than abruptly.

Which AI sectors are most likely to survive long term?

Sectors with the strongest long-term resilience include:

- Compute platforms and chip manufacturers

- Data center operators

- ROI-led enterprise AI applications

- Scientific AI, particularly in drug discovery and materials engineering

These segments align closely with real business demand and infrastructure dependency.

Which AI segments face the highest consolidation risk?

Frontier large language model companies, autonomous code-generation tools, and pure-play AI cybersecurity platforms face consolidation pressure due to differentiation challenges, high integration dependencies, and unclear profitability paths.

What lessons from the dot com era apply most to AI today?

The most critical lesson is that technology adoption must be grounded in measurable business value. The dot com era demonstrated that narrative-driven growth without economic fundamentals ultimately fails, while disciplined, infrastructure-aligned innovation survives.