Payments modernization in banking is the strategic transition from outdated, batch-based legacy systems to an agile, real-time infrastructure capable of processing transactions instantly, 24/7. This transformation is driven by the need to meet customer expectations for immediate payments, improve operational efficiency, and enable new digital products. It is achieved by building a new payments hub using microservices and APIs, integrating it into a broader core banking transformation, and leveraging automation to manage high-volume, real-time transaction flows.

Core Deficiencies of Legacy Payment Platforms

The core deficiencies of legacy payment platforms are their reliance on slow batch processing, high operational costs, and an inability to integrate with modern technologies. These monolithic systems create significant technological debt that limits a bank’s competitiveness and exposes it to operational risk.

1) Inherent Delays:

Batch processing introduces delays, making these platforms incompatible with the instant settlement expectations of modern digital commerce.

2) High Operational Costs:

Complex maintenance cycles, specialized hardware, and manual interventions result in a high total cost of ownership.

3) Lack of Agility:

Monolithic codebases make it slow and expensive to launch new products, update features, or integrate with third-party fintech services.

4) Data Silos:

Siloed data architecture complicates compliance reporting, prevents a unified view of customer activity, and inhibits data-driven decision-making.

5) Security Vulnerabilities:

Outdated technology stacks are often more difficult to secure against sophisticated, modern cybersecurity threats.

Technological debt from legacy payment systems directly inhibits a bank’s ability to compete, innovate, and manage risk effectively in a digital-first economy.

Alignment of Payments Modernization with Core Banking Transformation

Payments modernization is an integral component of a comprehensive core banking transformation because payment systems are deeply interconnected with core functions like ledgers, fraud detection, and liquidity management. Treating payments modernization as a standalone project creates significant integration risk and fails to address foundational architectural limitations.

Key Considerations:

1) Interdependency:

Real-time payments directly impact core account ledgers, fraud screening engines, and liquidity management systems, requiring synchronized updates.

2) Phased Modernization:

A common strategy is to decouple payment services from the monolithic core into a flexible payments hub. This allows for a phased approach, reducing the risk of a “big bang” failure while delivering incremental value.

3) Data Consistency:

Integrating a modern payments hub with a legacy core requires a robust data strategy to ensure consistency and accuracy across all systems during the transition.

Attempting to modernize payments in isolation from the core banking system creates significant integration risk and fails to address foundational architectural limitations.

The Role of Banking Process Automation in Real-Time Payments

Banking process automation is essential in real-time payments to manage the high transaction volume, speed, and 24/7 operational demands that manual processes cannot support. Automation ensures the scalability and accuracy required for an instant, always-on payments environment.

1) What it is:

Automation in this context involves using technologies to handle repetitive, rule-based tasks and complex decision-making in the payment lifecycle.

2) Why it matters:

It reduces human error, ensures consistent application of compliance rules, and allows for 24/7 operations without a proportional increase in staffing.

3) How it is implemented:

Robotic process automation in banking (RPA) handles structured tasks like data entry and validation, while intelligent automation (AI/ML) manages complex fraud detection and exception handling.

In a real-time payments environment, automation is not an efficiency tool but a mandatory capability for operational viability and risk management.

Key Architectural Principles for Modern Payments Systems

The key architectural principles for modern payments engineering are adopting a microservices-based architecture, leveraging cloud-native technologies, and implementing an event-driven, data-centric design. These principles provide the foundation for building a system that is agile, resilient, and scalable.

1) Microservices Architecture:

Complex payment functions are broken down into small, independent, and deployable services (e.g., payment initiation, fraud scoring). This contrasts with a single monolithic application, allowing for faster updates and greater resilience.

2) API-First Communication:

Services communicate via Application Programming Interfaces (APIs), creating a flexible ecosystem that can easily integrate with internal systems and external partners.

3) Cloud-Native Technologies:

Using cloud infrastructure provides the elastic scalability needed to handle fluctuating transaction volumes efficiently and cost-effectively.

4) Event-Driven Design:

This approach ensures that payment data is processed, analyzed, and acted upon in real time, enabling immediate decision-making for fraud detection and liquidity monitoring.

A shift from monolithic to microservices architecture is the foundational principle of modern Engineering modernization banking , enabling agility, scalability, and resilience.

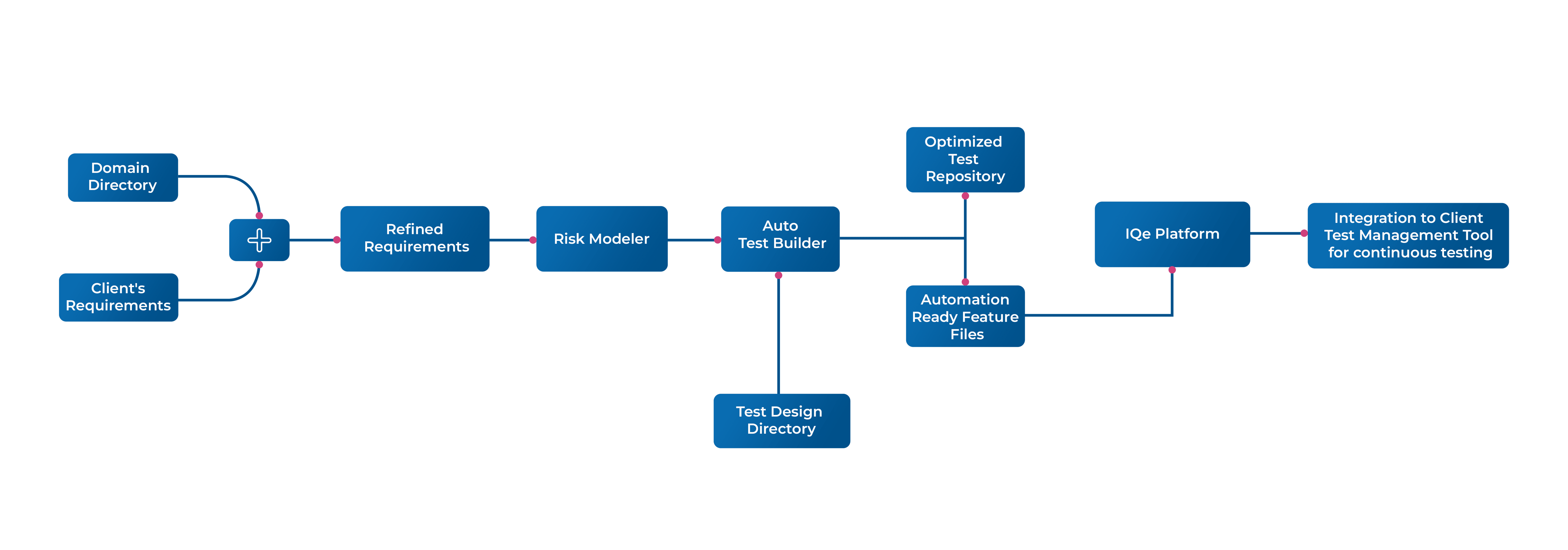

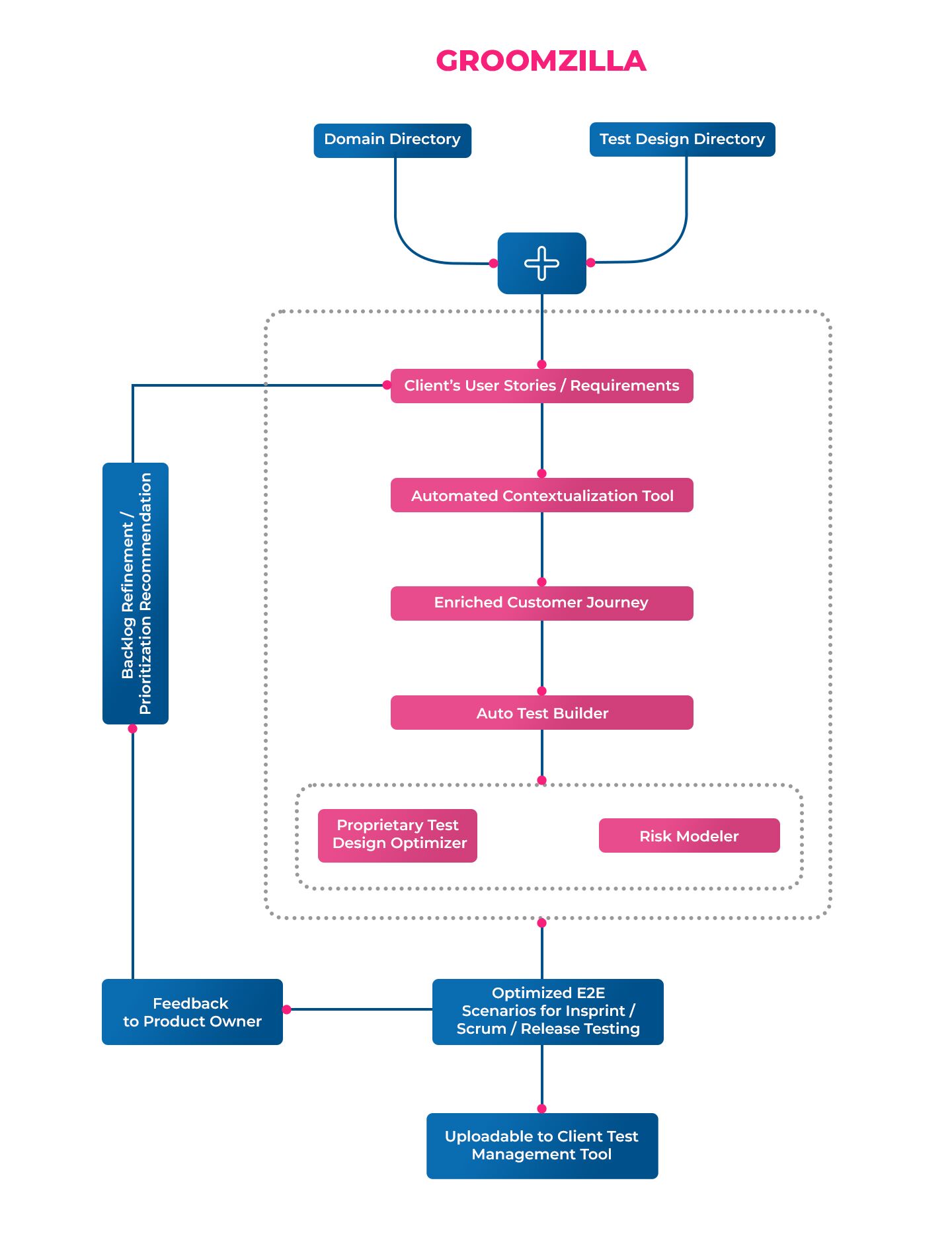

Approach to End-to-End Testing for Core Banking Modernization

Banks should approach end-to-end testing for core banking modernization with a comprehensive strategy that covers the entire transaction lifecycle, including performance, security, and integration testing. Due to the systemic importance of payment systems, a robust, automated, and continuous testing framework is non-negotiable to mitigate risk.

Types of Critical Testing:

1) Performance and Load Testing:

Validates that the system can handle peak transaction volumes and 24/7 operations without performance degradation.

2) Security Testing:

Includes penetration testing and vulnerability assessments to protect the system against sophisticated fraud and cyber threats.

3) Integration Testing:

Ensures seamless data flow and communication between the new payments hub, legacy core systems, third-party networks, and customer channels.

4) Regression Testing:

Automated tests that run continuously to ensure new code changes do not break existing functionality, which is critical in an agile development environment.

For critical payment systems, end-to-end testing must validate not just functional correctness but also resilience under peak load and security against sophisticated threats.

The Strategic Importance of Post-Implementation Application Support

Post-implementation application support is strategically important because it ensures the long-term stability, performance, and compliance of the new real-time payments platform. A real-time environment requires a proactive support model that can anticipate and resolve issues before they impact customers.

1) Shift to Proactive Monitoring:

Specialized banking ams services (Application Management Services) must actively monitor system health and transaction flows, rather than reacting to failures.

2) Continuous Compliance:

The support function is responsible for managing updates and ensuring the platform remains compliant with evolving payment regulations and network rules.

3) Performance Optimization:

Effective application support bfsi teams analyze performance data to optimize the system over time, improving efficiency and reducing operational costs.

4) Foundation for Innovation:

A stable, well-supported platform provides the reliable foundation needed to build and launch new payment-related products and services.

In a real-time payments ecosystem, application support must evolve from a reactive, break-fix function to a proactive service ensuring continuous system health and performance.

Frequently Asked Questions (FAQ)

Is a “rip and replace” approach necessary for payments modernization?

No, a complete “rip and replace” of the core system is high-risk and disruptive. Most financial institutions opt for a phased modernization strategy, such as building a parallel payments hub that gradually takes over transaction volume from legacy systems. This approach mitigates risk and ensures service continuity.

How do real-time payments impact fraud detection and compliance?

Real-time payments require real-time fraud detection and compliance screening. Because instant transactions are irrevocable, prevention is critical. This necessitates advanced AI and machine learning models to analyze transactions and identify anomalies before execution, replacing slower post-transaction batch analysis.

What is the typical timeline for a core banking transformation focused on payments?

A focused payments modernization project typically ranges from 18 to 36 months. The timeline depends on the complexity of the existing architecture, the chosen implementation strategy (e.g., phased vs. parallel), and the scope of integration with other banking systems.

Can robotic process automation in banking be an interim solution for legacy systems?

Yes, RPA can serve as a tactical, interim solution to bridge gaps between legacy systems and new platforms during a transition. It is effective for automating manual data transfers or reconciliation tasks that would otherwise require complex point-to-point integrations.

What are the implications of the ISO 20022 messaging standard for payments modernization?

Adopting the ISO 20022 global messaging standard is a core component of payments modernization. This standard provides richer, more structured data within payment instructions, which enhances transparency, improves automation, strengthens compliance screening, and enables the development of new data-driven financial services.