The Mobile First Approach to Digital Transformation

Digital transformation has evolved into a strategically imperative business operation for all industries – with mobile phones playing a key technology-enabler. In a bid to ‘mobilise’ banking, financial institutions are recognizing the role of smartphones in digital transformation and its integration into core business strategies.

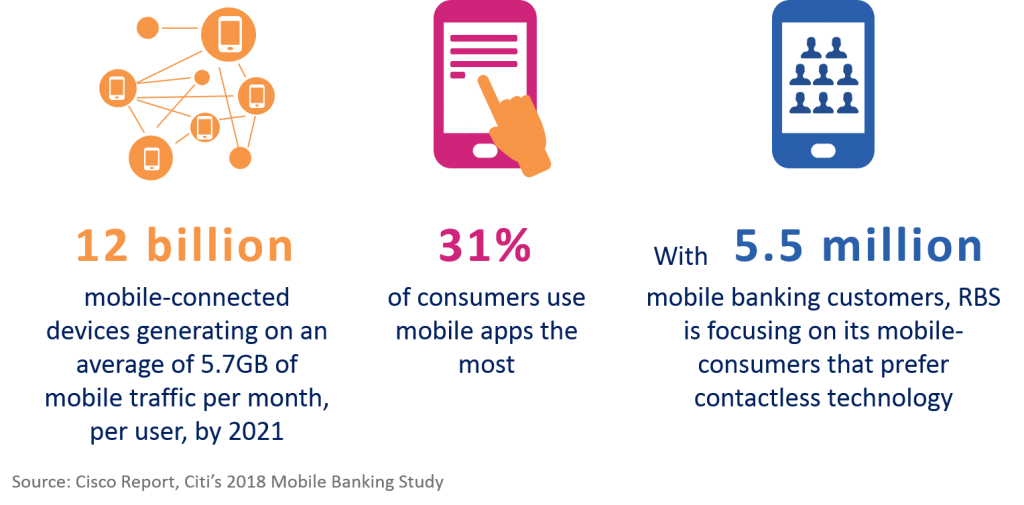

In a recent report by Cisco it was stated that by 2021, there will be nearly 12 billion mobile-connected devices generating on an average of 5.7GB of mobile traffic per month, per user. While mobile banking apps are not new to the finance industry with 31% of consumers using mobile apps the most, as per Citi’s 2018 Mobile Banking Study. From checking their balances to transferring funds, apps are taking care of all banking transactions. Rapid development in mobile banking technology has shifted user’s perception towards digital payments and also seen an increase in “digital branches” that replace traditional banks. The Royal Bank of Scotland (RBS) is working on plans to create a standalone digital bank and is soon to shut down over 259 branches across UK. With 5.5 million mobile banking customers, RBS is focusing on its mobile-consumers that prefer contactless technology.

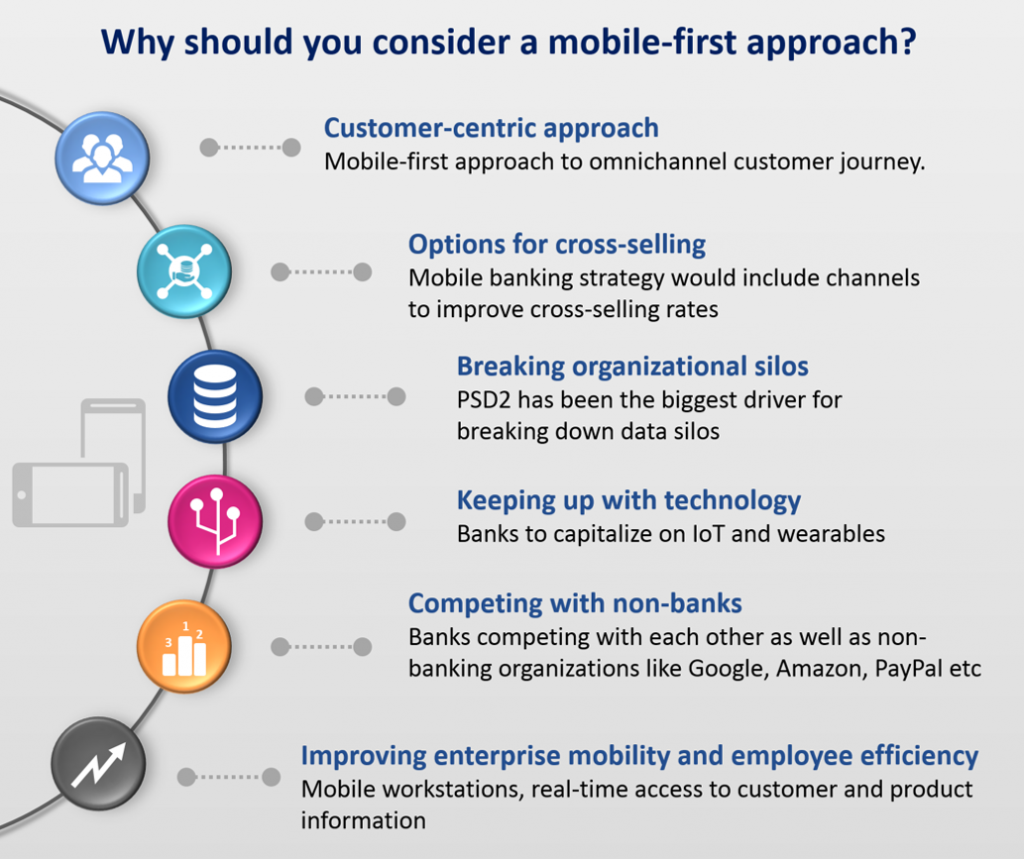

Why should you consider a mobile-first approach?

As per Deloitte’s 2018 Banking Outlook report, the emphasis is on building a mobile-centric platform that’s redefining their retail channel strategies, product portfolios, and delivery models. The report stresses on the importance of viewing mobiles, not as a one-way window for delivering products and services, but rather places it at the core of delivery strategies.

-

Customer-centric approach

Consumers are constantly looking for services that are convenient, available at all times and do not compromise on security/privacy. To meet the demands of a growing tech-savvy consumer base banks have to quickly adopt technological solutions. Smartphones have become essential to deliver a seamlessly connected omnichannel customer journey. With a heavy consumer-base, an interesting trend seen in banks is the move towards design and user experience.

Mobile banking creates new rules for a customer-centric banking process – smart visual interface, building a relationship with the customer through other channels, generate traffic to increase sales and, improve speed-to-market rates with innovative solutions.

-

Options for cross-selling

An effective mobile banking strategy would include channels to improve cross-selling rates. A decline in bank foot traffic is making banks develop selling strategies that rely heavily on technology. Machine learning techniques are empowering financial institutions with data insights (such as app usage, location, transaction history etc.) that banks can leverage to increase sales. Analytics is also being used to acquire new customers through digital channels.

-

Breaking organizational silos

As banks transform into digital organizations a change in organizational structure is evident. Legacy systems are quickly being replaced by a unified system that operates irrespective of the technology stack evolvement, improves efficiency and is easily scalable. PSD2 has been the biggest driver for breaking down data silos, wherein banks have to start sharing data with their party providers. The new directive opens up banking industry to new entrants and is creating a shared data network system, where information is easy to access and share across all touch points. Banks, like HSBC, are adopting technology to centralize their operations and expedite services such as loan processing.

-

Keeping up with technology

The increase in connected devices is an opportunity for banks to capitalize on IoT and wearables. “Wearable banking” is soon going to be the next big thing to impact banking-on-the-go. It is forecasted that the Internet of things in banking market is expected to register a CAGR of 18.49% by 2023. Banks that succeed in keeping up with technological trends will become trendsetters for creating numerous downstream opportunities.

-

Competing with non-banks

With the new PSD2 directive banks have to find innovative solutions to compete not only with each other but also with non-banking organizations like Google, Amazon, PayPal etc., to retain their consumer base. For example, Apple recently announced the launch of Apple Pay – a secure payments service for iOS. It also provides loans to small and medium-sized companies. While organizations like Apple are not looking to turn into a financial institute, it is working towards partnering with banks to grow its financial stance.

-

Improving enterprise mobility and employee efficiency

While external innovation is taking place with the presence of apps and wearable-tech, financial institutes also have to look into improving workforce productivity. The right mobile strategy enables the bank to adopt digital transformation as a multi-faceted tool for their employees. For the mobile workforce, organizations could look at improving collaboration and productivity through mobile workstations, real-time access to customer and product information, and foster innovation within the organization.